Despite the record success of many initial coin offerings (ICOs), raising capital for ICOs is a difficult process. It is tempting to accept help anywhere one can get it, and there is no shortage of persons and companies clamoring to “find” or refer investors in exchange for a little commission in the form of fiat currency or tokens. Depending upon how they introduce the potential investors, these persons and companies may be required to register as “broker-dealers” under various federal and state laws before they may make such referrals. An ICO that is a securities offering which uses unregistered broker-dealers may find itself with significant securities law headaches. To avoid those headaches, this article explains the differences between broker-dealers and finders, and provides some useful guidance on how to properly use them. To help simplify things, this article will only address ICOs which are securities offerings and not comment on non-securities offerings of utility tokens.

Broker-Dealer Regulation

Broker-dealers are primarily regulated under the Securities Exchange Act of 1934 (the “Exchange Act”). In addition, many states also regulate broker-dealers through their securities laws, commonly referred to as “blue sky laws.” For example, California law provides a right of rescission (the right to get out of a contract), recovery of additional monetary damages, and an extended statute of limitations for investors against an unlicensed broker-dealer. This article focuses on federal laws as opposed to state securities laws (which are for the most part similar with each other and with federal law, although differing in particulars). Most “brokers” and “dealers” must register with the Securities Exchange Commission (“SEC”) using Form BD and join a self-regulatory organization (“SRO”), and, in most cases, the Securities Investor Protection Corporation. Overseeing nearly 3,800 brokerage firms and approximately 634,000 registered brokers, the Financial Industry Regulatory Authority (“FINRA”) is the largest independent regulator for all securities firms doing business in the United States.

Broker-dealers are primarily regulated under the Securities Exchange Act of 1934 (the “Exchange Act”). In addition, many states also regulate broker-dealers through their securities laws, commonly referred to as “blue sky laws.” For example, California law provides a right of rescission (the right to get out of a contract), recovery of additional monetary damages, and an extended statute of limitations for investors against an unlicensed broker-dealer. This article focuses on federal laws as opposed to state securities laws (which are for the most part similar with each other and with federal law, although differing in particulars). Most “brokers” and “dealers” must register with the Securities Exchange Commission (“SEC”) using Form BD and join a self-regulatory organization (“SRO”), and, in most cases, the Securities Investor Protection Corporation. Overseeing nearly 3,800 brokerage firms and approximately 634,000 registered brokers, the Financial Industry Regulatory Authority (“FINRA”) is the largest independent regulator for all securities firms doing business in the United States.

Registration

The Exchange Act makes it unlawful for any broker or dealer to “effect any transactions in, or to induce or attempt to induce the purchase or sale of, any security” unless that broker or dealer is registered with the SEC. Speaking generally, ICOs raising capital, and the persons or companies helping ICOs raise such capital, usually do not need to worry about registration issues affecting dealers. There are some situations which could certainly involve dealers, but more often, the concern is whether persons or companies helping raise capital on behalf of the ICO must register as brokers. One who refers a potential investor to an ICO and receives in return either a commission based on the transaction or a success fee is likely a broker within the definition of the Exchange Act. If so, the failure to register as such could result in serious adverse consequences to the person deemed an unregistered broker-dealer, including injunctive or disciplinary action against the person or company, the prohibition of such person or company from registering as a broker-dealer in the future, and exposure to investor suits, fines, and penalties, and even criminal prosecution. The consequences against an ICO utilizing the unregistered broker-dealer are similarly grave, and could include investor suits and possibly criminal prosecution in addition to a number of other undesirable effects, such as increased scrutiny of the ICO and its securities offerings.

The Exchange Act makes it unlawful for any broker or dealer to “effect any transactions in, or to induce or attempt to induce the purchase or sale of, any security” unless that broker or dealer is registered with the SEC. Speaking generally, ICOs raising capital, and the persons or companies helping ICOs raise such capital, usually do not need to worry about registration issues affecting dealers. There are some situations which could certainly involve dealers, but more often, the concern is whether persons or companies helping raise capital on behalf of the ICO must register as brokers. One who refers a potential investor to an ICO and receives in return either a commission based on the transaction or a success fee is likely a broker within the definition of the Exchange Act. If so, the failure to register as such could result in serious adverse consequences to the person deemed an unregistered broker-dealer, including injunctive or disciplinary action against the person or company, the prohibition of such person or company from registering as a broker-dealer in the future, and exposure to investor suits, fines, and penalties, and even criminal prosecution. The consequences against an ICO utilizing the unregistered broker-dealer are similarly grave, and could include investor suits and possibly criminal prosecution in addition to a number of other undesirable effects, such as increased scrutiny of the ICO and its securities offerings.

Broker-Dealers Generally

The Exchange Act defines a “broker” as “any person engaged in the business of effecting transactions in securities for the account of others,” and a “dealer” as “any person engaged in the business of buying and selling securities for his own account, through a broker or otherwise”. In short, a broker sells securities for clients, while a dealer sells securities for itself. In determining whether a person or a company is a broker or a dealer, the SEC looks at the activities in which the person or business actually engages. Note that the SEC looks at “activities,” and not just one “activity”. While one particular activity may not require registration as a broker or dealer, other activities may require it. ICO promoters should become sufficiently educated to at least analyze on a broad basis how various activities have been considered in the decisions of federal courts and the SEC’s no-action and interpretive letters.

Questions to Consider

The SEC provides the following questions as general guidance as to whether a person or company is a broker or dealer. Answering “yes” to any of the questions may indicate the need to register as a broker or dealer:

Broker

- Do you participate in important parts of a securities transaction, including solicitation, negotiation, or execution of the transaction?

- Does your compensation for participation in the transaction depend upon, or is it related to, the outcome or size of the transaction or deal? Do you receive trailing commissions, such as 12b-1 fees? Do you receive any other transaction-related compensation?

- Are you otherwise engaged in the business of effecting or facilitating securities transactions?

- Do you handle the securities or funds of others in connection with securities transactions?

Dealer

- Do you advertise or otherwise let others know that you are in the business of buying and selling securities?

- Do you do business with the public (either retail or institutional)?

- Do you make a market in, or quote prices for both purchases and sales of, one or more securities?

- Do you participate in a “selling group” or otherwise underwrite securities?

- Do you provide services to investors, such as handling money and securities, extending credit, or giving investment advice?

- Do you write derivatives contracts that are securities?

What About Finders?

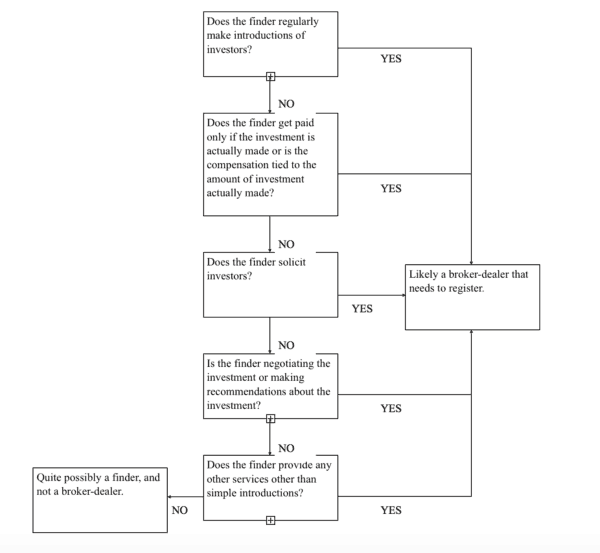

It is commonly believed that a person can avoid classification as a broker by claiming to be merely a “finder”. Technically, it is true that one may generally conduct the activities of a finder without registration under the Exchange Act. Hence, ICOs may freely use, and compensate, finders. However, labeling oneself a finder is not dispositive; if one is engaged in the activities in which a broker-dealer engages, registration generally is still required. In most cases, people or companies that claim to be finders actually are brokers and must register under the Exchange Act.

A true finder merely introduces a potential investor to the ICO in exchange for a fee that is paid regardless of whether that investor ultimately invests or not. In addition, the true finder does not (1) solicit investors, (2) negotiate, recommend, provide advice or information, or assist in any way with respect to the securities or the securities offering, or (3) regularly introduce investors to issuers of securities.

Using Finders

ICOs using finders must take care to ensure that the claimed finder is indeed a legitimate, true finder. ICO promoters should conduct due diligence into the finder’s past activities and proposed future activities sufficient to discern whether the finder has conducted unregistered broker-dealer services previously, and whether that finder is or is not likely to engage in broker-dealer activities before or during the ICO. In an engagement letter with a finder, ICO promoters should consider including indemnification clauses for any liability incurred by the ICO as a result of the finder’s failure to register as a broker-dealer, if registration turns out to be required by law. Additionally, ICO promoters may consider obtaining representations and warranties from the finder that it is not a broker-dealer and is therefore not required to register as a broker-dealer. Providing covenants that clearly spell out prohibited activities may be helpful both in educating unsophisticated finders about the broker-dealer laws, as well as affording the ICO with a breach of contract claim against the finder for any such violations.

Verifying Registration

In analyzing whether a party is a registered broker, the first step should be to verify registration by using the FINRA BrokerCheck tool located at: http://finra.org/brokercheck. Next, ICO promoters should carefully investigate the broker-dealer’s qualifications to ensure that the broker-dealer is capable of providing the all of the services you require from it and ultimately raise the capital it claims to be able to. After retaining a broker-dealer, the ICO should work closely with the broker-dealer to ensure that it conducts the offering in the manner necessary to utilize the securities exemptions that the ICO needs to rely upon.

In analyzing whether a party is a registered broker, the first step should be to verify registration by using the FINRA BrokerCheck tool located at: http://finra.org/brokercheck. Next, ICO promoters should carefully investigate the broker-dealer’s qualifications to ensure that the broker-dealer is capable of providing the all of the services you require from it and ultimately raise the capital it claims to be able to. After retaining a broker-dealer, the ICO should work closely with the broker-dealer to ensure that it conducts the offering in the manner necessary to utilize the securities exemptions that the ICO needs to rely upon.

Conclusion

All broker-dealers are finders, but not all finders are broker-dealers. Typically, finders do not need to be registered under federal and state laws, but broker-dealers do. In most cases, if a person or company does anything other than only provide an introduction of a potential investor to an ICO, or takes compensation that is dependent on the whether the investment or how much investment is made, then that person or company is a broker-dealer and must be registered with the appropriate authorities. ICOs that choose to leverage the services of finders or broker-dealers should take steps to minimize their legal exposure to liability from claims related to the use of unregistered broker-dealers or illegal finders in order to ensure a successful and legal ICO.

Jor Law is a co-founder of VerifyInvestor.com, a widely used resource for accredited investor verifications in the crowdfunding and cryptocurrency initial coin offering (ICO) space. These verifications are required by federal laws for generally solicited Regulation D, Rule 506(c) capital raises. Jor Law is also a co-founder of Homeier Law PC, where he practices corporate and securities law, including helping companies take advantage of alternative forms of capital raising such as venture capital, EB-5 finance, Regulation D, Rule 506(c) offerings, Reg A+ offerings, crowdfunding, and of course, ICOs.

Jor Law is a co-founder of VerifyInvestor.com, a widely used resource for accredited investor verifications in the crowdfunding and cryptocurrency initial coin offering (ICO) space. These verifications are required by federal laws for generally solicited Regulation D, Rule 506(c) capital raises. Jor Law is also a co-founder of Homeier Law PC, where he practices corporate and securities law, including helping companies take advantage of alternative forms of capital raising such as venture capital, EB-5 finance, Regulation D, Rule 506(c) offerings, Reg A+ offerings, crowdfunding, and of course, ICOs.