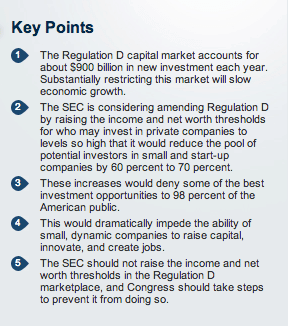

The Securities and Exchange Commission (SEC) is considering substantial increases in the Regulation D thresholds for “accredited investor” income and net worth, which would reduce the pool of potential investors in small businesses and start-up companies by 60 percent to 70 percent. This will impede these firms’ access to capital and, therefore, slow economic growth.

The Securities and Exchange Commission (SEC) is considering substantial increases in the Regulation D thresholds for “accredited investor” income and net worth, which would reduce the pool of potential investors in small businesses and start-up companies by 60 percent to 70 percent. This will impede these firms’ access to capital and, therefore, slow economic growth.

Among others, this policy will harm:

- Entrepreneurs seeking to launch new companies or grow existing ones;

- Investors who could invest under the current thresholds but not under the proposed thresholds;

- Millions of American workers who will not secure good, well-paying jobs because the firms that create those jobs will not exist;

- Millions of other American workers whose real wages will stagnate because the economy will remain mired in its current slow growth condition; and

- The federal government because anemic economic growth will reduce tax revenues and increase expenditures on federal programs.

The SEC should not raise the accredited investor thresholds, and Congress should prevent the commission from doing so.

Securities Law and Regulations

Securities regulation dates back many centuries. Modern securities regulation began in Kansas with the adoption of a comprehensive state regulatory regime in 1911. Many states soon followed Kansas’s example. Federal securities regulation began with the Securities Act of 1933 and the creation of the Securities and Exchange Commission by the Securities Exchange Act of 1934.

The Securities Act of 1933. The Securities Act of 1933 generally prohibits selling securities unless they are registered with the Securities and Exchange Commission. The act exempts various securities and transactions from this requirement. Making a registered offering (often called going public) is expensive and well beyond the means of most small and start-up companies.

Private Placements. Section 4(a)(2) of the Securities Act exempts “transactions by an issuer not involving any public offering.” Neither the statute nor securities regulations define what is a “public offering” or what is not a public offering. A non-public offering is generally called a private placement, and Section 4(a)(2) is usually called the private placement exemption.

Primarily because of this provision, three friends, for example, could join together to form a business without running afoul of federal securities laws. Nevertheless, they would need to be careful. If they are a little too public in seeking investors, they could run afoul of federal or state securities laws. For example, telling a local reporter about their plans when they run into him at a local high school football game or standing up at the local Kiwanis or Rotary Club seeking investors would probably be deemed a public offering (unless they have a “substantial pre-existing relationship” with everyone in the room).

Regulation D. The SEC adopted Regulation D in 1982. An issuer who complies with the requirements of Regulation D will be treated as exempt from the registration requirements of the Securities Act. Regulation D achieves this by creating three exemptions under Rule 504, Rule 505, and Rule 506. Rule 506 accounts for about 94 percent of Regulation D offerings and over 99 percent of the capital raised via Regulation D.

Under Rule 506, a company may raise an unlimited amount of money and sell securities to an unlimited number of “accredited investors” (and up to 35 non-accredited, but sophisticated investors). Critically, Rule 506 offerings are not subject to most aspects of state securities regulation because the National Securities Markets Improvement Act of 1996 (NSMIA) preempts most state regulation of Rule 506 offerings. Thus, although Rule 506 imposes a greater federal regulatory burden than Rule 504 or Rule 505, small issuers making small offerings usually use Rule 506 to avoid the costs, delay, and regulatory risk involved in complying with multiple state securities laws (usually called “blue sky laws”). Rule 504 and Rule 505 offerings involve about 0.1 percent of the Regulation D capital raised.

Accredited Investors. An issuer using Rule 506 may sell to an unlimited number of accredited investors. Under Regulation D, an accredited investor is generally either a financial institution or a person with an income of more than $200,000 ($300,000 joint) or a residence exclusive net worth of $1 million or more.

Accredited Investors. An issuer using Rule 506 may sell to an unlimited number of accredited investors. Under Regulation D, an accredited investor is generally either a financial institution or a person with an income of more than $200,000 ($300,000 joint) or a residence exclusive net worth of $1 million or more.

The idea underlying the exemption for accredited investors is that they are either sophisticated themselves or affluent enough to acquire advice from sophisticated advisors. They can therefore “fend for themselves” and do not require protection of the Securities Act. This analysis largely follows the leading Supreme Court case of Ralston Purina in interpreting what is and is not a public offering under the Securities Act.

Regulation D Is Economically Important

In 2012, more than three times as much capital was raised under Regulation D as through public sales of equity (i.e., ownership shares). Total private placements ($1.7 trillion) exceeded public (i.e., SEC-registered) securities sales ($1.2 trillion), and Regulation D offerings ($903 billion) accounted for over half of all private offerings. Two-thirds of Regulation D offerings were equity. More than 234,000 investors participated in Regulation D offerings, of which more than 90,000 participated in offerings by nonfinancial issuers.

Although the amount of capital raised through Regulation D offerings is large, the average offering size is only $30 million, and the median offering size is just $1.5 million. Regulation D is the primary means by which new companies and young growing companies raise equity capital. As two SEC analysts put it, “Consistent with the original intent of Regulation D to target the capital formation needs of small business, there have been more than 40,000 issuances by non-financial issuers since 2009 with a median offer size of less than $2 million.”

One goal of Regulation D was “a substantial reduction in costs and paperwork to reduce the burdens of raising investment capital (particularly by small business).” It is imperfect, but compared to previous regulations governing private placements, Regulation D has achieved that goal, particularly since NSMIA was enacted.

Recent Developments and Cause for Concern

Section 413(a) of the Dodd–Frank Wall Street Reform and Consumer Protection Act[21] required the SEC to modify the net worth qualification for an accredited investor to exclude the equity in a person’s residence when calculating that person’s net worth. In addition, Section 413(b) invites the commission to analyze whether the $1 million net worth standard “should be adjusted or modified for the protection of investors, in the public interest, and in light of the economy.” The SEC may undertake this review as early as July 21, 2014, but no later than 2018. Continued quadrennial reviews are required.

Section 415 of Dodd–Frank required the Government Accountability Office (GAO) to conduct a study of the accredited investor thresholds. In July 2013, the GAO released this study: “Alternative Criteria for Qualifying as an Accredited Investor Should Be Considered.”

On July 24, 2013, the SEC proposed a series of revisions to Regulation D that would substantially increase the burden on Regulation D issuers. Tucked in the discussion of these proposed rules is a request for comments regarding the definition of an accredited investor.

The commission is specifically seeking comment on the following points:

Are the net worth test and the income test currently provided in Regulation D the appropriate tests for determining whether a natural person is an accredited investor? Do such tests indicate whether an investor has such knowledge and experience in financial and business matters that he or she is capable of evaluating the merits and risks of a prospective investment? If not, what other criteria should be considered as an appropriate test for investment sophistication?

Are the current financial thresholds in the net worth test and the income test still the appropriate thresholds for determining whether a natural person is an accredited investor? Should any revised thresholds be indexed for inflation?

Currently, the financial thresholds in the income test and net worth test are based on fixed dollar amounts (such as having an individual income in excess of $200,000 for a natural person to qualify as an accredited investor). Should the net worth test and the income test be changed to use thresholds that are not tied to fixed dollar amounts (for example, thresholds based on a certain formula or percentage)?

The Flawed Arguments for Raising the Thresholds

A wide variety of pro-regulation organizations have taken this opportunity to indicate to the SEC their support for increasing the accredited investor thresholds and a variety of other provisions that would make Regulation D more complex.

![]()

![]() For example, the North American Securities Administrators Association, which represents state and provincial securities regulators, supports more than doubling the net worth threshold to a residence exclusive net worth of $2.4 million and increasing the income thresholds from $200,000 to nearly $500,000 to account for inflation since Regulation D was adopted in 1982.[26] Americans for Financial Reform, a coalition of 250 pro-regulation groups, believes that updating the definition for inflation since 1982 “is the single most important step the Commission can take to ensure that unregistered securities sold under Rule 506 are sold only to those investors who are financially sophisticated enough to understand the risks and wealthy enough to absorb potential losses.” AARP supports dramatic increases, seemingly to at least $2.5 million in investments and $400,000 in income. The Consumer Federation of America (CFA) supports not only increasing the thresholds dramatically, but additional changes that would substantially narrow the definition of accredited investor. The CFA’s Director of Investor Protection Barbara Roper opines:

For example, the North American Securities Administrators Association, which represents state and provincial securities regulators, supports more than doubling the net worth threshold to a residence exclusive net worth of $2.4 million and increasing the income thresholds from $200,000 to nearly $500,000 to account for inflation since Regulation D was adopted in 1982.[26] Americans for Financial Reform, a coalition of 250 pro-regulation groups, believes that updating the definition for inflation since 1982 “is the single most important step the Commission can take to ensure that unregistered securities sold under Rule 506 are sold only to those investors who are financially sophisticated enough to understand the risks and wealthy enough to absorb potential losses.” AARP supports dramatic increases, seemingly to at least $2.5 million in investments and $400,000 in income. The Consumer Federation of America (CFA) supports not only increasing the thresholds dramatically, but additional changes that would substantially narrow the definition of accredited investor. The CFA’s Director of Investor Protection Barbara Roper opines:

But the burden of proof should be on those groups resisting change to demonstrate that the existing threshold satisfies the Supreme Court test of identifying a group of investors with the financial sophistication to understand the risks of investing in private offerings and the financial wherewithal to withstand potential losses. We have little doubt that, to the degree that it ever did, the current definition has long ceased to identify a population of investors who are capable of “fending for themselves” without the added protections afforded in the public markets.

The primary argument for raising the thresholds is simply that they have not been raised since they were adopted in1982 and that inflation has effectively reduced the original thresholds in real, inflation-adjusted terms. Table 2 shows what the accredited investor thresholds would be if they had been indexed for inflation during the past three decades.

Logically, the inflation adjustment argument rests on the idea that the number picked by the SEC in 1982 was correct. A review of the discussion in the proposed and final rule shows that the number was not based on any sophisticated economic analysis. It was, in effect, the best guess of people involved with the markets at the time. In the proposed rule, the SEC chose a net worth test of $750,000 and an income test of individual adjusted gross income of $100,000 or more in the most recent year. Based on comments to the SEC, these were increased in the final rule to $1,000,000 in net worth for the investor and his or her spouse and $200,000 of income in the past two years combined with a reasonable expectation of this level of income in the current year. The use of the tax concept of adjusted gross income was dropped.

The proper way to examine the question of whether the accredited investor definition should be changed to account for inflation is not blind adherence to a largely arbitrary threshold chosen in 1982. The correct approach is to determine whether evidence indicates that the current thresholds are problematic, and the answer to that is no. Proponents of increasing the threshold offer no evidence demonstrating the alleged problem.

Regulation D works and has become an integral part of the U.S. capital market. Of course, there is some fraud in the Regulation D market, just as in the public market or any other market. Such fraud is unlawful, and vigorous enforcement of the laws against securities fraud is entirely warranted. However, no evidence suggests that fraud is more commonplace in Regulation D offerings than in other offerings. Moreover, there is little reason to believe that increasing the accredited investor thresholds would materially affect the level of fraud in any event.

Prior to the 2012 Jumpstart Our Business Startups (JOBS) Act, it was illegal for an inventor or entrepreneur to place an advertisement in a newspaper or on the Internet seeking rich people to invest in the idea unless he or she went public. Going public is prohibitively expensive for most start-ups. Now, Title II of the JOBS Act permits general solicitation or advertising seeking accredited investors for Rule 506 offerings. Opponents of the JOBS Act argue that it “increases the risk of fraud and misleading practices in the vast and increasingly important Regulation D market.” They propose increased accredited investor thresholds as the solution to this alleged problem.

The argument that the general solicitation provisions of the JOBS Act require increased accredited investor thresholds is simply mistaken. First, over the objection of the CFA, AARP, state regulators, and many others, Congress decided by huge bipartisan majorities to permit general solicitation in Rule 506 offerings. The SEC should not seek to thwart congressional purposes by increasing the regulatory burden on Rule 506 offerings to such an extent that they are no more attractive (or potentially less so) than there were before the JOBS Act became law. The opponents of the JOBS Act are trying to accomplish through SEC rule-making what they could not accomplish in Congress. Moreover, Congress should not allow the SEC to do so.

Second, the JOBS Act contains provisions ensuring that only accredited investors may invest in Rule 506 offerings involving general solicitation. The SEC recently adopted rules—a year after the congressionally imposed deadline—governing general solicitation in Rule 506 offerings. These rules impose strict requirements on Rule 506 issuers engaging in general solicitation. They must use tax returns or other information to verify that investors have income or net worth sufficient to qualify as accredited investors.

Raising the Thresholds Is Bad Economic Policy

Raising the accredited investor thresholds would devastate the ability of entrepreneurs to launch new enterprises and impede the capacity of small firms to grow, innovate, and create jobs. This dramatic negative effect on the economy substantially outweighs the highly speculative improvement in investor protection that proponents of higher thresholds are claiming.

The GAO estimates that the proposed increase in the net worth thresholds for accredited investors would reduce the number of potential small business investors from 8.5 million to 3.4 million, a reduction of 60 percent. Adjusting the income thresholds would reduce the pool of small business investors from 6.1 million to 1.7 million, a reduction of 72 percent. (See Table 3.)

Per the GAO:

According to SEC [sic], when the standard was first created, 1.87 percent of households qualified as accredited investors. SEC staff estimate that 9.04 percent of households would have qualified as accredited investors under the net worth standard in 2007; we estimate that removing the primary residence from households’ net worth, as required in the Dodd-Frank Act, dropped the percentage to 7.2 percent (based on 2010 data).

The wealthiest 7 percent of the public are not poor, uneducated people incapable of securing investment advice or making informed decisions themselves. Nor are they incapable of bearing financial risk. Increasing the thresholds to the 1982 levels in inflation-adjusted terms would reduce the pool to about the top 2 percent of households.

The wealthiest 7 percent of the public are not poor, uneducated people incapable of securing investment advice or making informed decisions themselves. Nor are they incapable of bearing financial risk. Increasing the thresholds to the 1982 levels in inflation-adjusted terms would reduce the pool to about the top 2 percent of households.

Economic research has increasingly demonstrated that most job creation comes from young, dynamic companies, which some call “gazelles.” These companies need equity investment to launch and grow. A recent survey of the economics literature on the subject reached the conclusion that gazelles “create all or a large share of net new jobs.”

Adopting policies that impede these dynamic firms’ access to capital will exacerbate unemployment and hold down improvements in real wages. They will harm millions of Americans who will not be able to secure good, well-paying jobs because the firms that create those jobs will not exist. Given the size of the Regulation D capital market and the critical role of gazelles in job creation and economic growth, these effects will be macroeconomically important.

Fairness Considerations

Most proponents of increasing the accredited investor thresholds believe that they are protecting investors from themselves—from making unwarranted investments. They do not believe that the wealthiest 7 percent of the population have the sophistication or the financial wherewithal to make investments beyond the public marketplace. They believe that they are too unsophisticated to seek and pay for sophisticated advice.

Yet is it fair, in the name of federal paternalism, to limit some of the best investment opportunities to those who are already wealthy with a net worth exceeding 98 percent of their fellow citizens? Certainly such a policy will thwart upward mobility. Preventing all but the very richest Americans from investing in the most promising companies in America is inappropriate and unfair as well as economically destructive.

Policy Recommendations

Congress and the SEC should not limit investing to only the very richest. Specifically:

- The SEC should refrain from increasing the accredited investor thresholds and from adopting other restrictions that would limit which investors can invest in Rule 506 offerings.

- Congress should repeal Section 413(b) of Dodd–Frank, which requires continuing review of the accredited investor thresholds.

- Moreover, Congress should amend the statutory definition of accredited investor to ensure that the thresholds are not increased by the SEC.

Conclusion

Although imperfect, Regulation D works. It funds most of the dynamic companies that account for the bulk of U.S. economic growth. The solution to the potential problem of higher accredited investor thresholds is straightforward. The SEC should leave well enough alone.

(Editors Note: This article was previously published on The Heritage Foundation. The article was reproduced with the approval of the author)

_______________________________________

David R. Burton focuses on tax matters, securities law, entitlements and regulatory and administrative law issues as The Heritage Foundation’s senior fellow in economic policy. Burton was general counsel at the National Small Business Association for two years before joining Heritage’s Roe Institute for Economic Policy Studies in 2013. He previously was chief financial officer and general counsel of the start-up Alliance for Retirement Prosperity, a conservative alternative to AARP. For 15 years, Burton was a partner in the Argus Group, a Virginia-based law, public policy and government relations firm. Burton received a Juris Doctor degree from the University of Maryland School of Law. He also holds a bachelor of arts degree in economics from the University of Chicago.

David R. Burton focuses on tax matters, securities law, entitlements and regulatory and administrative law issues as The Heritage Foundation’s senior fellow in economic policy. Burton was general counsel at the National Small Business Association for two years before joining Heritage’s Roe Institute for Economic Policy Studies in 2013. He previously was chief financial officer and general counsel of the start-up Alliance for Retirement Prosperity, a conservative alternative to AARP. For 15 years, Burton was a partner in the Argus Group, a Virginia-based law, public policy and government relations firm. Burton received a Juris Doctor degree from the University of Maryland School of Law. He also holds a bachelor of arts degree in economics from the University of Chicago.