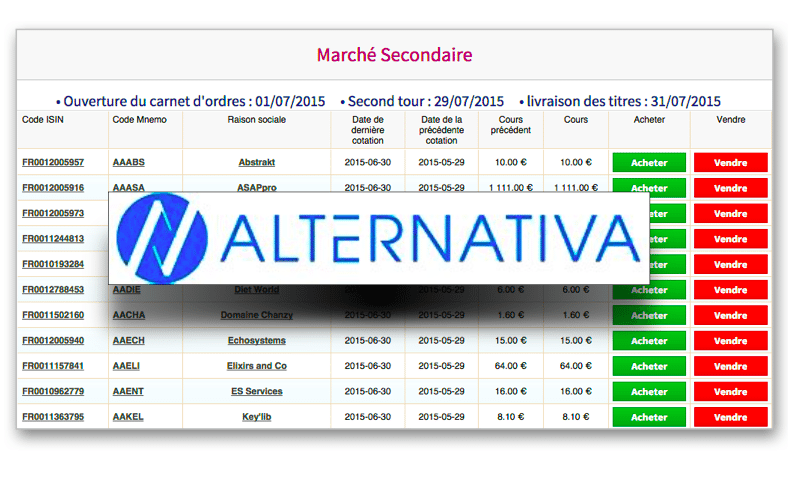

Alternativa.fr is an intriguing cross between an equity crowdfunding platform and an alternative exchange system which gives it something many crowdfunding platforms would like to have: a secondary market for trading SME’s private equity shares.

Creating liquidity for private shares is an ongoing discussion in most parts of the world that are enacting regulations to improve access to capital to SMEs. Alternativa has incorporated a model that provides an option to sell – or purchase – private SME shares.

I caught up with Philippe Dardier, President and CEO of Alternativa in Lisbon, at the European Crowdfunding Network (ECN)’s Crowdcamp, one day after he was appointed to the board of ECN.

Therese: Bonjour Philippe. Alternativa.fr is both an equity crowdfunding platform and an alternative trading system, can you explain?

Therese: Bonjour Philippe. Alternativa.fr is both an equity crowdfunding platform and an alternative trading system, can you explain?

Philippe: Alternativa is an independent privately-owned digital marketplace for listing and trading SME securities, a sort of junior exchange. It fills a gap between, on the one hand, regulated public exchanges, such as Alternext, which finance midsize companies rather than SMEs, and, on the other hand, equity crowdfunding platforms which raise private equity for startups and SMEs, albeit with non tradable securities, no secondary market.

The original model of Alternativa was the Swedish alternative trading platform Alternativa.se. Alternativa.fr tried to import the concept of a secondary market for SMEs’ private equity into France. The company started in 2008 and opened for business in 2009, in the wake of the financial crisis. The timing was bad and the concept did not catch on.

In the meantime, around 2011, I left my banking job. As a business angel and private investor, I was invested in an international portfolio of 20 companies, including Alternativa, Vistaprint, Attenda, Ficofi… I experimented firsthand what it means to look for an exit! Out of my 20 investments, two made it to an IPO, of which one was a NASDAQ IPO, thus did pretty well, 5 were OK, and the rest went bust.

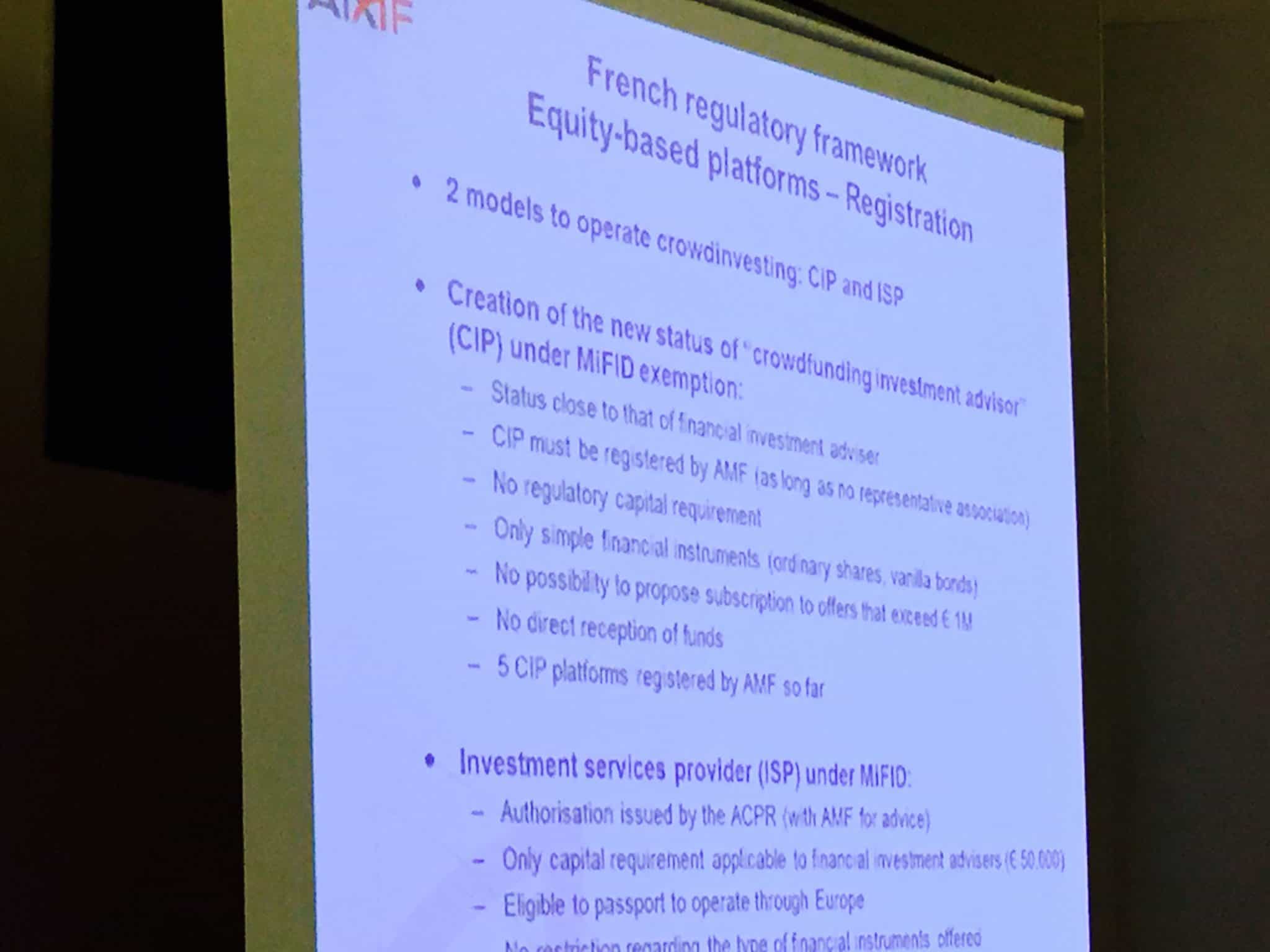

I took over Alternativa.fr in 2012. At the time, the company was getting more and more requests from SMEs looking for primary funding through the platform. We were also under pressure from the regulator to become more mainstream and to adopt a regulatory status within the framework of the European Markets in Financial Instruments Directive (MIFID). To comply, I split the company into two businesses:

- AM France: an Investment Services Provider (Prestataire de Services d’Investissement, PSI in French) which enables SMEs to raise equity quite like an equity crowdfunding platform regulated as such [Author’s note: the difference is explained in detail below].

- Alternativa.fr: a Multilateral Trading Facility (MTF in English, Système Multilatéral de Négociation, SMN in French)) which enables investors to trade shares on a secondary market.

Therese: How is Alternativa doing so far? Who are the companies funded, who are the investors?

Philippe: So far, Alternativa has listed and funded 41 companies, raising €36.8 million in pure SME equity – no real estate, no lending, (so far) no bonds –and direct shareholding. This makes us France’s largest equity crowdfunding platform. Last year we did €6 million. By mid-year 2015 we reached around €4 million. One of our most visible funding rounds was with Domaine Chanzy, a burgundy vineyard, for which we raised over €2.6 million in 2015. The company was also independently co-funded on Seedrs and is now preparing an LSE – AIM listing.

Philippe: So far, Alternativa has listed and funded 41 companies, raising €36.8 million in pure SME equity – no real estate, no lending, (so far) no bonds –and direct shareholding. This makes us France’s largest equity crowdfunding platform. Last year we did €6 million. By mid-year 2015 we reached around €4 million. One of our most visible funding rounds was with Domaine Chanzy, a burgundy vineyard, for which we raised over €2.6 million in 2015. The company was also independently co-funded on Seedrs and is now preparing an LSE – AIM listing.

In addition to the Alternativa.fr platform, we run two regional platforms: The new Lyon regional private stock exchange called Place d’échange, and Normandy’s equity crowdfunding & trading platform Kiosktoinvest.

The average funding raised on Alternativa is around €500,000 to €600,000. The average investment is €12,000. We take between 7% and 12% commission on funds raised. We only work with SMEs, not startups. If we list tech or like biotech companies, we need them to show they have robust technology. We list only full limited companies (Société par Actions, SA in French), not the simplified version (Société par Actions Simplifiée, SAS).Companies that raise equity through us are automatically listed on the MTF, the trading platform, to enable secondary market transactions. This wouldn’t be possible with an SAS. An SAS is a flexible structure that facilitates growth of companies, but in the mid long term it’s hindering their growth.

Once a company is listed, the shareholder agreement is replaced by the platform’s Rulebook which determines fair and transparent rules for trading shares. We don’t charge for holding shares.

Once a company is listed, the shareholder agreement is replaced by the platform’s Rulebook which determines fair and transparent rules for trading shares. We don’t charge for holding shares.

The secondary market is taking off, even though it is slowed down by French taxation rules that grant tax reliefs to investors under the condition that they hold their share for 5 years or more. This year, 3 companies have traded 5 % of their market cap and 8 have traded sporadically. Among the other companies, some do not have liquidity because the amount of listed shares is too low, less than 10% of their total equity.

We have about 2,300 regular repeat investors. By and large, these investors are high net worth individuals, independent financial advisors, small private banks, and the occasional family office. They are self-directed investors. They get exposure to us online, via the press and all forms of media.

Therese: Why did you chose to be regulated outside of the French crowdfunding framework of October 2014?

Therese: Why did you chose to be regulated outside of the French crowdfunding framework of October 2014?

Philippe: Indeed, we are not regulated as Conseil en investissement participatif, CIP (Crowdfunding Investment advisor) which is the regular status of equity crowdfunding platforms in the French crowdfunding regulation. We don’t need and don’t want a CIP status because it is part of a local French regulation, i.e. not passportable. The current statuses of our two entities as PSI (Investment Services Provider) and MTF are recognized Europe-wide. This gives us a European passport that enables us to operate with professional investors and companies throughout the European Union and the European Economic Area (excluding Switzerland – all in all 32 countries) and is approved for retail distribution in the UK, Belgium, and, obviously, France.

Equity markets are international. We don’t want to be restricted to the French market. For this same reason, we are part of the European Crowdfunding Network (ECN) rather than of the French local chapter and organizations.

Therese: What are the main differences between Alternativa and crowdfunding platforms regulated as CIPs in France?

Philippe: I already mentioned several differences. But to make a list:

We list only limited companies registered as SA. These companies are formally audited and evaluated by independent certified analysts who are registered with the French regulatory authority, the Autorité des Marchés Financiers (AMF).

We list only limited companies registered as SA. These companies are formally audited and evaluated by independent certified analysts who are registered with the French regulatory authority, the Autorité des Marchés Financiers (AMF).- We automatically list companies for which we raise funds on the MTF, the secondary market.

- We are allowed to raise up to €5 million –against €1 million for equity crowdfunding platforms regulated as CIP.

- Investors are qualified investors rather than small retail investors and their average investment is significantly higher.

- Legal entities such as investment funds can be and are investors on the platform.

- Investors are direct shareholders –whereas crowdfunding platforms regulated as CPI often collect crowdfunding shares into a special vehicle,

- Our status gives us a European passport – whereas most crowdfunding platforms are locally regulated.

In summary, one could say that we are focused on order execution rather than investment advisory.

Therese: How do you see the market evolving?

Philippe: Focusing on the French market, there is a huge need for more sources of SME financing. Therefore, there is room for different crowdfunding models, especially for models like ours, with a secondary market offering an additional exit opportunity. But it is also important to educate SMEs in what is expected of them in terms of reporting and communication.

A few innovations would also greatly help the market develop: the introduction of a unique European company identification code (ISIN), as well as a standardization of the simplified prospectus which, for example, should list risk factors to help investors make conscious decisions.

A few innovations would also greatly help the market develop: the introduction of a unique European company identification code (ISIN), as well as a standardization of the simplified prospectus which, for example, should list risk factors to help investors make conscious decisions.

French income tax is a major hindrance to the growth of retail investment in France. There are tax reliefs, some with the above mentioned negative side effects, but retail investors have already deserted the stock market: They represent less than 5% of the stock market against 25% twenty years ago, in 1995. The new crowdfunding models can bring retail investors back to financing the French/European economy if they are efficient and transparent and timely in their corporate communication.

Thank you, Philippe!

Therese Torris is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique and curates crowdfunding news on Scoop.It.

Therese Torris is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique and curates crowdfunding news on Scoop.It.