Mercator Advisory Group is out with brief write up on the status of the Office of the Comptroller of the Currency Fintech Charter and one sentence in the report pretty much sums it up:

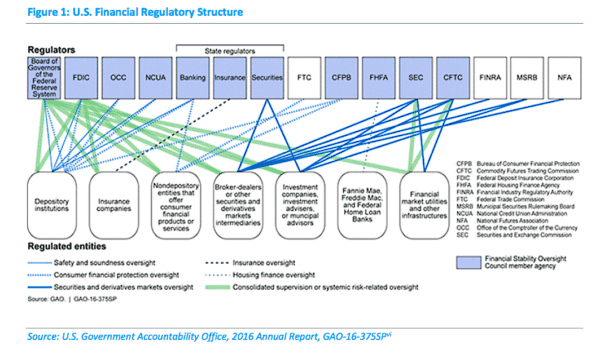

“The United States has the most fractured, decentralized, and complicated regulatory structure in the world, a structure that includes more than a dozen federal agencies and 50 separate state regulatory entities.”

So the issue has been identified, now what is the solution?

Having a fragmented and convoluted regulatory system that stymies innovation in the financial services is an implicit tax upon both consumers and business. Creating a streamlined regulatory environment for financial services encourages Fintech innovation which can then better challenge entrenched traditional financial firms. This is good for the economy and better for consumers so why don’t policymakers do something about it?

Well, each of these regulatory agencies and 50 states have fiefdom’s and budgets to protect. Once again, progress is hobbled by parochial politics and internecine posturing for power and control. Clearly it is time for a regulatory overhaul the consolidates federal agencies to single digits. As for the states, if they were truly looking out for their constituents they would be leading the charge.

Well, each of these regulatory agencies and 50 states have fiefdom’s and budgets to protect. Once again, progress is hobbled by parochial politics and internecine posturing for power and control. Clearly it is time for a regulatory overhaul the consolidates federal agencies to single digits. As for the states, if they were truly looking out for their constituents they would be leading the charge.

If we step back and look at the global environment, other regions have embraced innovation. As the authors of the report state:

“The U.S. financial services regulatory agencies, including the Federal Reserve and OCC, have been somewhat passive regarding the potential impact of Fintech companies and solutions on the banking industry. This is in contrast with the more proactive approach taken by the European Union through the European Commission (EC) and by certain sovereign nation regulators, such as in the United Kingdom.”

The OCC Fintech Charter could have been a viable vehicle to solve much of the problem Fintech faces in the US. Mercator ostensibly supports the initiative:

“This move is neither outside the scope of the OCC’s unilateral regulatory authority nor unprecedented. The OCC has the authority to grant charters for special purpose national banks (SPNBs) and federal savings associations under the National Bank Act and the Home Owners’ Loan Act (HOLA), respectively. Indeed, existing regulations define a special purpose national bank as a bank that conducts activities other than fiduciary activities and engages in at least one of three core banking functions: receiving deposits, paying checks, or lending money. A precedent was the creation of credit card banks. In effect, the OCC is simply reaffirming its own chartering authority.”

With several lawsuits filed challenging the OCC Fintech Charter the entire process is on hold. No Fintech firm will go through the process of filing for a Fintech Charter and who would blame them? Congress really needs act, but good luck with that.

The Mercator report concludes:

“U.S. regulators have been rather passive in the face of the rapidly evolving impact that Fintech is having on the financial services industry. The OCC is in the process of expanding its role in this sector by allowing special purpose national bank charters to be filed by Fintech companies. The principal reason is ostensibly to gain better control over the potential for instability in the financial services industry driven by lack of direct visibility into this explosive industry sector. Whether or not this continues to move forward depends on both the views of a yet-to-be- appointed replacement for Thomas Curry and the pending litigation introduced by the CSBS.”

The Mercator report is available for free download after you hand over some personal info.