Last week during the National Crowdfunding and Fintech Association of Canada’s annual event, FFCON2018, there was a single presentation that provided a state of Fintech in Canada. Professor Michael King, from the Scotiabank Digital Banking Lab @ Ivey Business School, delivered an excellent synopsis of what’s working and what’s not.

Entitled “the Current State of Fintech in Canada: The Good, The Bad and The Ugly,” King’s deck bulleted out both the high and the low.

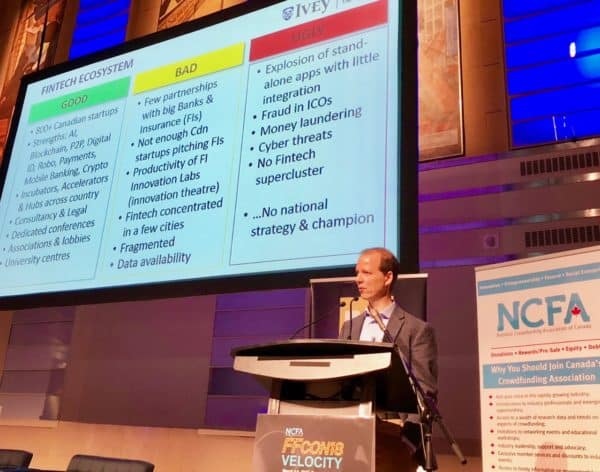

So what is working out well up North?

Canada is growing Fintech startups. There are more than 800 today which is pretty respectible for a smaller country.

Areas of prominence include Blockchain, AI, Payments, peer to peer and more.

There are an increasing number of incubators and accelerators to promote sector growth, plus recognition by universities and other support sectors that Fintech is of strategic importance.

What is not so good, or perhaps kind of bad?

Traditional financial institutions have been slow to adopt Fintech innovation or partner with emerging disruptive financial firms. King provided a painful, but probably not a unique example, where a traditional bank required 120+ signatures to partner with Fintech firm. Geez.

[clickToTweet tweet=”In Canada, traditional financial institutions have been slow to adopt #Fintech innovation or partner with emerging disruptive financial firms” quote=”In Canada, traditional financial institutions have been slow to adopt #Fintech innovation or partner with emerging disruptive financial firms”]

And what really sucks?

Beyond the routine shortfalls, King hits home: There is no national strategy. No Fintech champion. The Canadian government simply lacks direction.

Beyond the routine shortfalls, King hits home: There is no national strategy. No Fintech champion. The Canadian government simply lacks direction.

Canada is not alone in lacking in concrete federal goal. The fragmented regulatory environment dominated by the provinces does not help. While many countries have embraced a Fintech mission, such as the UK, Singapore, and Australia, Canada has not yet focused its policymaking energy towards this objective. In fact, Canada hovers at the bottom of the pack when it comes to global Fintech adoption (see in the deck).

Things can change, of course, and there are multiple Fintech success stories that are Canada based. But there could be more.

[clickToTweet tweet=”There is no national strategy. No #Fintech champion. The Canadian government simply lacks direction” quote=”There is no national strategy. No #Fintech champion. The Canadian government simply lacks direction”]

See the presentation below.