In late 2013, seed accelerator YCombinator introduced the SAFE (simple agreement for future equity) – a convertible instrument designed to make seed stage investing quicker and less expensive.

The SAFEs quickly became a popular structure for seed investing. Early this fall, YCombinator introduced several changes to the SAFE, most significant among them is a change in the basis for conversion from a “pre-money” to “post-money” valuation.

In addition, YCombinator announced that it was increasing its investment amount from $120,000 to $150,000 (still in return for 7% of the venture’s equity). For context, in 2007 the standard investment by YCombinator was $20,000.

YCombinator’s shift reflects two trends in the venture industry. As The Wall Street Journal recently reported, there has been a big increase in the size of early-stage investments and valuation (“More Venture-Capital Money Is Going Into Fewer Startup Deals”, November 11, 2018). Citing data from Pitchbook, the article indicated that the median size of seed investments in 2018 was $2 million, nearly 4 times the 2013 average. Meanwhile, the median seed stage valuation rose by about 50% during the same time period.

In addition to deal size, seed fundraising has increasingly become a “phase” rather than a fixed point in time, with many ventures undertaking multiple raises during their seed phase.

A large portion of this financing is raised using convertible instruments such as convertible promissory notes and SAFEs. As a result, the first “qualified financing,” usually associated with Series A (although sometimes occurring when Series Seed equity is issued), triggers a “wave” of conversions (the “Qualified Financing”). The presence of multiple convertible instruments, often sold in individual financing events rather than as part of a round and potentially having different conversion caps, made it difficult for SAFE holders to accurately assess the value of their holdings. Switching to a post-money valuation provides significant clarity. A similar dynamic is leading to increasing use of post-money valuations in priced equity rounds as well.

Historically, these conversions were made based on the pre-money valuation of the venture at the time of the financing and the cap was applied on a pre-money basis. The new SAFE provides that all SAFE funding is counted in determining valuation for purposes of calculating the conversion of the SAFE.

Under the old form SAFEs and convertible notes were excluded from the conversion calculation. However, the conversion calculation is performed before factoring in the new money funding the Qualified Financing. As a result, if a SAFE holder invests $100,000 with a post-money valuation cap of $5,000,000, the SAFE holder will own 2% of the company immediately prior to the Qualified Financing regardless of whether the company has issued other SAFEs or convertible notes prior to the financing.

Under the old form SAFEs and convertible notes were excluded from the conversion calculation. However, the conversion calculation is performed before factoring in the new money funding the Qualified Financing. As a result, if a SAFE holder invests $100,000 with a post-money valuation cap of $5,000,000, the SAFE holder will own 2% of the company immediately prior to the Qualified Financing regardless of whether the company has issued other SAFEs or convertible notes prior to the financing.

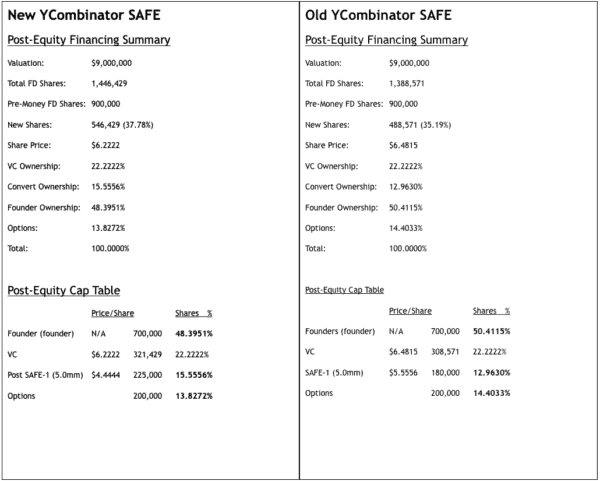

Here is an example that illustrates the difference. Calculations were done using a very helpful calculator on the angelcalc.com website. In each case, the founders own 700,000 shares, there is $1,000,000 in issued SAFEs with a $5 million cap and 200,000 issued options. The VC is investing $2 million at a $7 million post-money valuation (as a result the VC ends up with the same equity position under the old and New SAFEs).

Other than the choice of SAFE form, the financial terms of both financings are identical. As a result, what is noteworthy about comparing the two cap tables is that the introduction of the new SAFE form resulted in a significant shift in equity from the founders and employees to the SAFE holder.

This shift in equity allocation would become more pronounced if the company issues additional SAFEs/convertible notes or options. Conversion on a post-money basis essentially provides the SAFE holder with anti-dilution protection. The SAFE holder will own the same percentage of the company going into the Qualified Financing regardless of other financing activity by the company.

Other Highlights:

While the shift to a post-money basis is arguably the most significant change in the new SAFE, the new form includes several additional substantive changes:

- Exclusion of the Option Pool Expansion – Any expansion of the option pool which is included in the Qualified Financing, is not included in the SAFE conversion calculation.

- Pro-rata Investment Rights – The old SAFE form included a pro-rata right which became effective after conversion. The new SAFE eliminates this clause, but YCombinator has provided an optional side letter. The benefits of this approach are: (i) it allows founders to grant pro-rata rights on a case-by-case basis; and (ii) the side letter grants recipients the pro-rata rights in the conversion financing.

- No Modifications Representation – In an effort to promote simplicity, the new SAFE contains a representation that other than “filling in the blanks,” no other changes have been made to the form. While this may have utility for YCombinator deals, law firms frequently tweak the SAFE form, so this representation may be absent in many transactions.

- Liquidation Preference in an Exit or Dissolution – The new SAFE clarifies the preference status of SAFE holders, making it clear that they are junior to debt and convertible promissory notes, on par with preferred stock and other SAFEs, and senior to common stock.

- Tax-Related Provisions – The new SAFE includes a provision with respect to the tax treatment of the SAFEs. This language is designed to support the position that the SAFE should be treated as common stock, including for qualified small business stock purposes. In addition, the positioning, if embraced by the IRS, would avoid phantom income concerns such as the original issue discount on some forms of debt.

- Proceeds from a Liquidity Event – Under the new SAFE form, subject to certain tax concerns, if shareholders are provided a choice as to the form and amount of proceeds to be received in a Liquidity Event, SAFE holders are to receive the same choice.

- Amendment Process – Under the old SAFE form, amending a SAFE required the agreement of the individual SAFE holder. This reflected the fact that SAFE investments were often “one-off” events rather than rounds. The new SAFE form essentially creates artificial rounds by allowing amendments if approved by a majority-in-interest of SAFE holders whose SAFE’s have a common “Post-Money Valuation Cap” and “Discount Rate.” The provision also requires that each impacted SAFE holder be solicited, even if their consent is not obtained.

What Does It All Mean?

When SAFEs were first introduced, they were widely perceived as founder-friendly alternatives to convertible promissory notes. The revised form is somewhat more investor-friendly.

The biggest change is that the SAFE holders are immune from the dilutive impact of funds raised prior to the Qualified Financing through the use of convertible instruments and options granted prior to the Qualified Financing. The Founders and option holders bear this dilution.

Dror Futter is a partner in the Rimon, PC law firm. Dror’s practice focuses on representing startup companies in their financing and merger and acquisition transactions and their intellectual property, IT and internet agreements. He also advises companies with respect to Initial Coin Offerings and other blockchain legal issues. Dror was the co-founding chair of the PLI VC Law program and hosted their first blockchain legal program. He is a frequent speaker and writer on blockchain legal topics. He is a member of the model forms drafting group of the National Venture Capital Association, the legal advisory board of the Angel Capital Association and the legal working groups of the Wall Street Blockchain Alliance and the Digital Chamber of Commerce. Dror can be reached at dror.futter@rimonlaw.com