To my Fintech friends, this is my 4th annual “Top Ten” Fintech prediction. I started this tradition at Crowdfund Insider back in January 2017.

As we are saying goodbye to an incredible Fintech year of 2019, I see another seismic change in 2020 for our industry. One which could spell the end to Fintech as we know it.

Before we get there, let’s take a look at how I did last year. Here’s the link to my 2019 predictions and let’s review them one by one:

10. Consumer Lending Market Correction (Welp). I was wrong about this one. President Trump’s aggressive stands against the Federal Reserve paid off. The interest rates are still at an all-time low and employment numbers are strong. Despite trade wards with the rest of the world, the U.S. consumer market remains strong. People are still borrowing at an incredible speed. According to the Feds, total consumer revolving credit is over a trillion dollars, growing at a 5%+ annual rate.

9. The Rise of Debt Relief Companies (Welp). It’s just a matter of time when that trillion dollars will come home and roost. During a downturn, bankruptcy and foreclosures are typically the solutions for people that couldn’t get out of debt. There aren’t too many Fintechs thinking about this because most of them (and their founders) haven’t seen an economic cycle played out yet. Helping people get out of debt might be a thing in the near future, but we haven’t seen a lot of development this year on the Fintech front to get people ready for the next economic cycle.

8. Subprime Lenders Rejoice (True). We’ve seen a lot of activity happening between prime and subprime lending in 2019. Just today, someone told me about SeedFi.com another subprime lender that’s backed by Evolve Bank that aims to help the 100 million Americans living paycheck to paycheck. Companies such as Dave, Earnin, PayActiv all aim to unlock your earned salary but the actual APR may vary.

7. It’s Credit Union’s Turn (Welp). I was wrong about this. Credit Unions are still trying to stay relevant in today’s Fintech filled world. Whether it’s their management or their membership mandate, I still haven’t seen any innovation from Community Banks or Credit Unions. CULytics and their conferences are getting the word out there bridging Fintech and Credit Unions. You should check them out. Interestingly enough, I became a member of a “tech-driven” credit union and the experience has been nothing but horrific.

6. Student Lending Rising (True). This one is interesting, last year, I mentioned SixUp from San Francisco being one of the new players in the market. However, something new came onto the market via Income Share Agreements that’s catching a lot of attention in the media. Firms like meratas.com, StudentFinance.com, vemo.com are changing the way tuitions are financed. Income Share Agreements essentially defer the entire tuition and the student only pays when he/she is gainfully employed. Check them out.

5. Vertical Financing Will Dominate (True). Point of Sale financing is all the rage now. Unsecured personal loans are inherently risky because the money goes directly to the consumer. These point of sale financing models put money into the hands of doctors, merchants, installers and their credit risk profiles look much better. Patient Financing, Solar Energy Financing, and aforementioned student tuition financing Fintech are popping up everywhere to compete with traditional offerings. We will see many affirm.com look-alikes that target specific industries.

4. Biometrics are coming (again) (True). Facial recognition and social credit scoring are making waves all over the world. However, having your face analyzed by Macy’s security cameras might be decades away, we are sort of okay with have a device such as Alexa (Amazon) and HomePod (Apple) or worse, your phones sitting inches away from your bed, constantly listening to your every word…

3. Breakthroughs in Cost to Acquire (True). Amazon, Uber, Facebook are just some of the examples this year that came into Fintech. This week, bank executives are now saying that Big Tech is their true competition and not Fintech. Why? Cost of Acquisition. Facebook has 2.45 billion users and Chase might have 20-30 million customers.

2. A.I. Everywhere (True). This is scarily true. Elon Musk said AI is humanity’s biggest existential threat. We are now seeing A.I. used in health care, our criminal justice system and more. The inherent biases in these trained models will become a deathward spiral in the near future. The United Nations’s next AI For Good conferences is taking place in Geneva, Switzerland on May 4-8 2020. We can only hope that there will be standards to be followed.

1. The Birth of Micro-Fintechs (Welp). Other than Affirm and some of the newly minted Point of Sale Financing platforms, we haven’t seen a large adoption in Micro-Fintechs. Mostly, I believe Fintech infrastructures are not at the point of maturity that allows any merchants to set up their own financing options to avoid fees and charges from existing solutions such as credit cards. Directionally speaking, I think this has to happen. It should be as easy as signing up for Gmail for merchants to set up and launch a financing portal of their own.

Six out of ten is not too bad for 2019. Big Techs such as Facebook and Uber getting into Fintech in a major way really stole the large Fintech headlines.

Without further ado, here are my top ten Fintech predictions of 2020.

10. Death of Fintech. Fintech, as a buzzword will be dead. However, the Fintech ideals, infrastructure, data, and software will become ubiquitous and most of the consumers won’t be aware (or should they care) that they are using Fintech to get through their day to day goals. Big Tech is the new Fintech. FAANGs (Facebook, Amazing, Apple, Netflix and Google (Alphabet)) are all getting into Fintech including Uber. My number 3 prediction in 2018 is finally coming true.

9. Biometrics. Your retina, voice, and face will become your new payment method. Most of us use Apple and Samsung’s Face ID to unlock our devices. It’s just a matter of time (one step removed) from using your face to make payments. Try this with your iPhone when you have a chance. “Hey Siri, Can I make a payment?” And see what happens. Recently, I attended the LendIt Latin America Fintech conference in Miami, and there’s a startup called Facenote that is using your face as a payment method. Check them out at https://facenote.me/

8. Subscriptions everywhere. I predict that we will soon have to subscribe to credit or certain payment methods. We are already susceptible to all sorts of subscriptions from Netflix to PreCheck at the airport, paying a monthly fee to have guaranteed access to credit is not far fetched. A select few pays for an annual credit card fee, mass adoption is soon to come.

7. Everything is financed. Everything that’s of any value, whether it’s a product or a service should be financed into installment payments. Whether it’s an elective surgery or a six months coding school, there will be a financing option available for anything that’s consumable. There will be infrastructure companies that will put together underwriting, payments and loan servicing in one place and making it available at no or low cost to all merchants, everywhere.

6. Monoliths. There will be one company that will finance everything you do. The banks does a horrible job on conquering your wallet share, although that’s been their mantra for the past 30 years. Banks simply don’t know when you need credit or when you are shopping for goods and services. Paypal’s recent acquisition of Honey is forward-thinking and they might become your one-stop-shop but I won’t count out Google, Amazon or Apple for that matter.

6. Monoliths. There will be one company that will finance everything you do. The banks does a horrible job on conquering your wallet share, although that’s been their mantra for the past 30 years. Banks simply don’t know when you need credit or when you are shopping for goods and services. Paypal’s recent acquisition of Honey is forward-thinking and they might become your one-stop-shop but I won’t count out Google, Amazon or Apple for that matter.

5. United Nations of Credit. There will be one credit bureau that rules them all. The fragmentation of credit files across multiple bureaus and specifically negative bureau only countries are limiting the world’s economy. As human migration becoming more prevalent, people’s financial health records don’t necessarily come along for the ride. After working through privacy and political issues, a worldwide credit bureau is absolutely necessary to measure one’s creditworthiness. It’s scary but it needs to happen. China has been at the forefront of collecting every bit of information from their citizens, if you don’t score well, you are banned from something as simple as using public transportation. There are certainly a ton of moral and ethic issues that need to be discussed here but lack of information is certainly a big contribution of lack of access to credit.

4. New Rails. Visa, Mastercard, Discover, Amex, and ACH/Wire clearing houses have been dominating the payment scene for decades. With Libra from Facebook, a new form of currency riding on a more sophisticated rail such as blockchain will win us over. When we make a payment today, we don’t think about who owns the payment rails or layers of fees that merchants and consumers need to pay. These new rails will be everywhere and a whole new slew of functions and benefits will become the new standards of exchanging stored value.

3. Regulations. As Fintech enters its golden age, a phrase coined by Ron Suber, regulation is about to catch up. From crowdfunding regulations to how an accredited investors are being defined, regulatory bodies around the world are busy catching up with innovations happening around us. Regulation, by definition, is a one size fits all set of rules which by definition inhibits innovation. When we look at Fintech regulations happening in Latin America, in most cases, the initial ideas were for innovation, however, when regulators put ink to paper, the laws become another derivative of banking regulations which forbids any competition and innovation. Sweeping regulation is coming for payments and lending. It will reset us to another decade and leave us further behind other nations.

2. The rise of Fintech in Middle East and Africa. The often forgotten regions of the world denominated by conflicts and heavy reliance on energy as the center piece of their economy is waking up to Fintech. We will see developments similar to the Fintech Bay Initiative led by the nation of Bahrain to headline new Fintech developments in that region of the world. In 2020, we will see a lot more collaboration between Fintech and Big Tech companies in those parts of the world along with their local governments to develop new ways to provide access to banking, credit and payments for their citizens.

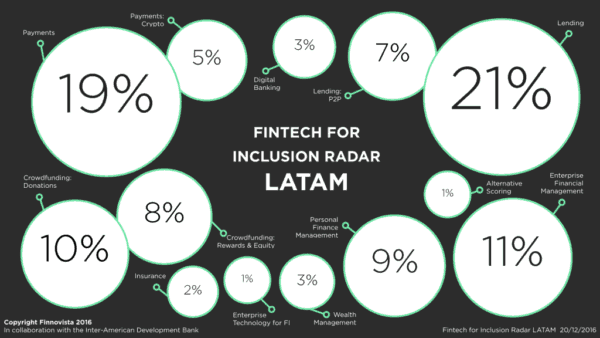

1. Brazil and LatAm. If you haven’t had the chance to read my series on Latin America Fintech development. Please take a look at them here and here. Brazil’s population will reach 220 million people in the next 10 years and it’s an economy roaring to dominate the international scene. BRICS (Brazil, Russia, Indian, China, and South Africa) are the major emerging national economies. These five countries consist of 40% of the world’s population, 20% of the world’s GDP as well as 27% of the world’s land surface. The Brazilian and LatAm Fintech scene is red hot with Softbank investing heavily in these countries’ infrastructure. I predict that 2020 will be a break out year for Brazil as the innovation center of Fintech and the word on the streets is that some of these LatAm Fintech companies are now eyeing Texas and Florida as their new battlegrounds for our Fintech future.

1. Brazil and LatAm. If you haven’t had the chance to read my series on Latin America Fintech development. Please take a look at them here and here. Brazil’s population will reach 220 million people in the next 10 years and it’s an economy roaring to dominate the international scene. BRICS (Brazil, Russia, Indian, China, and South Africa) are the major emerging national economies. These five countries consist of 40% of the world’s population, 20% of the world’s GDP as well as 27% of the world’s land surface. The Brazilian and LatAm Fintech scene is red hot with Softbank investing heavily in these countries’ infrastructure. I predict that 2020 will be a break out year for Brazil as the innovation center of Fintech and the word on the streets is that some of these LatAm Fintech companies are now eyeing Texas and Florida as their new battlegrounds for our Fintech future.

Until next time, see you in 2021.

Tim

Timothy Li is a Senior Contributor for Crowdfund Insider. Li is the Founder of Kuber, MaxDecisions, an Alchemy. Li has over 15 years of Fintech industry experience. He’s passionate about changing the finance and banking landscape. Kuber launched Fluid, a credit building product designed for college students to borrow up to $500 interest-free. Kuber’s 2nd product Mobilend is a true debt consolidation product, aiming to lower debt for all Americans. MaxDecisions provides financial institutions with the latest A.I. and Machine Learning algorithms and Alchemy is a state of the art end-to-end white-labeled lending platform powering some of the best Fintech companies in the world. Li also teaches at the University of Southern California School of Engineering.