While NVIDIA (NASDAQ:NVDA) reported relatively strong results, shares dipped in after hours trading in advance of the earnings call. NVIDIA topped expectations on both the top and bottom line but fell slightly short in data center revenue.

Expectations for the next quarter were solid – especially when you take into consideration that NVIDIA is not including any revenue from possible sales in China.

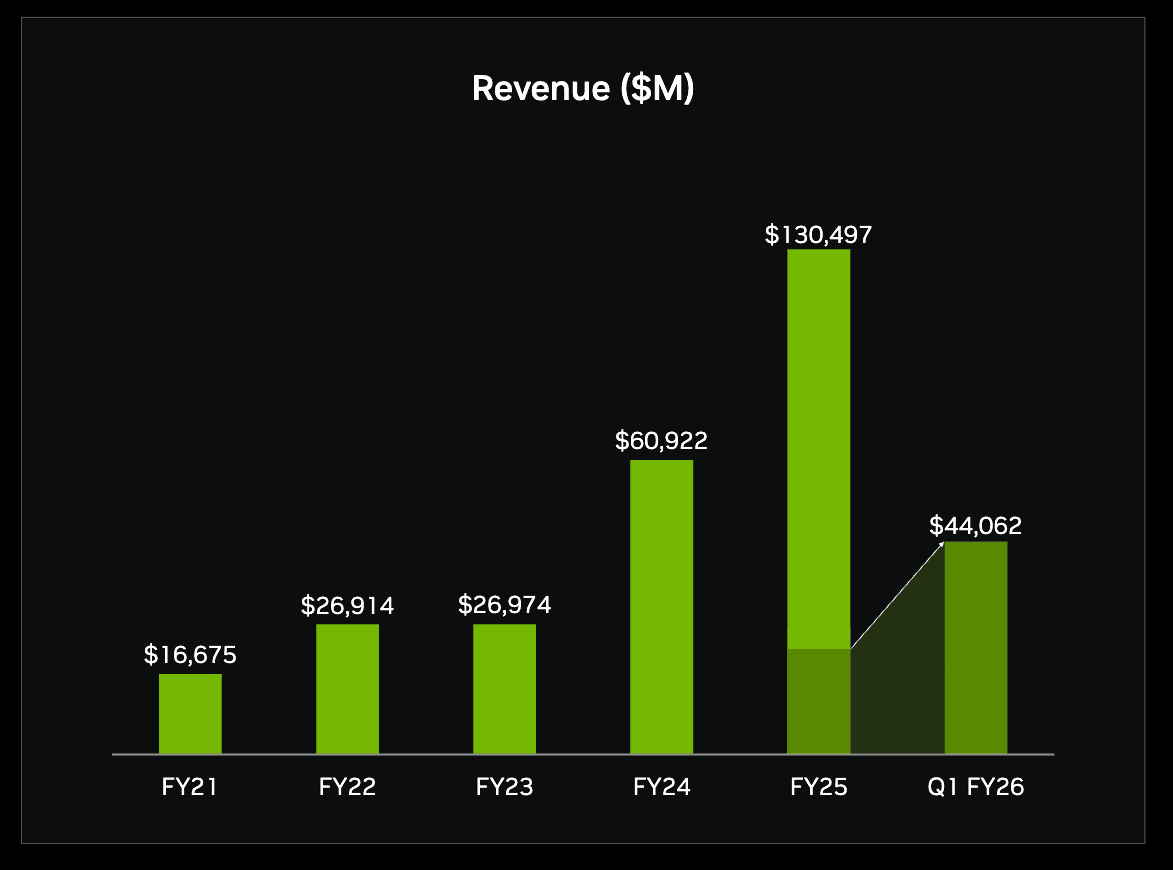

Revenue during Q2 was $46.7 billion, up 6% from Q1 and up 56% from a year ago.

Data Center revenue increased by 5% compared to Q1 to $41.1 billion and up 56% from a year ago.

Business with China has hovered over the company for much of the year due to trade restrictions with the country. NVIDIA said there were no H20 sales to China-based customers during the quarter. NVIDIA stated that it benefited from a $180 million release of previously reserved H20 inventory, resulting in approximately $650 million in H20 sales to a customer outside of China.

For the quarter, GAAP and non-GAAP gross margins were 72.4% and 72.7%, respectively.

Jensen Huang, founder and CEO of NVIDIA, issued a statement on Blackwell Ultra stating demand is “extraordinary” and production is ramping at full speed.

“NVIDIA NVLink rack-scale computing is revolutionary, arriving just in time as reasoning AI models drive orders-of-magnitude increases in training and inference performance. The AI race is on, and Blackwell is the platform at its center.”

Shares initally jumped higher on the results but then traders tempered their enthusiasm. Currently, shares are done by around 3.4% but this could change following remarks during the conference call.

The investor presentation is quite bullish, highlighting that the future opportunity for AI is incredibly enormous, with NVIDIA serving a fraction of various markets. In fiscal 2025, 88% of the company’s revenue came from data centers, followed by gaming at 9%. Other services, including financial services, are ramping now with exceptionally bullish predictions for the future of AI.