The Regulation CF market is only a few months old but data on successful crowdfunding campaigns is starting to percolate to the surface. Reg CF, created by Title III of the JOBS Act, allows small and emerging companies the ability to raise up to $1 million online. Retail equity crowdfunding has  already seen many successful funding campaigns and a handful of those offers have hit the million dollar cap.

already seen many successful funding campaigns and a handful of those offers have hit the million dollar cap.

Earlier this week, Crowdfund Insider was invited to sit in on presentation by Crowdfund Capital Advisors (CCA) on Reg CF progress to date.

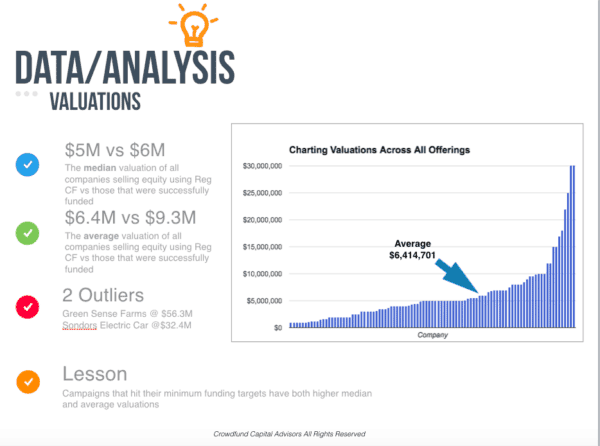

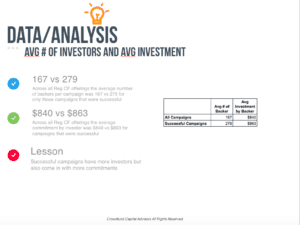

CCA is the creation of Jason Best and Sherwood “Woodie” Neiss – two individuals who were instrumental in getting the JOBS Act signed into law in 2012. The presentation covered the 49 companies have been successfully funded. According to CCA, the average valuation of these funded companies hovers around $6.4 million. Succesfully funded offers averaged 279 individual investors with an average commitmentof $863.

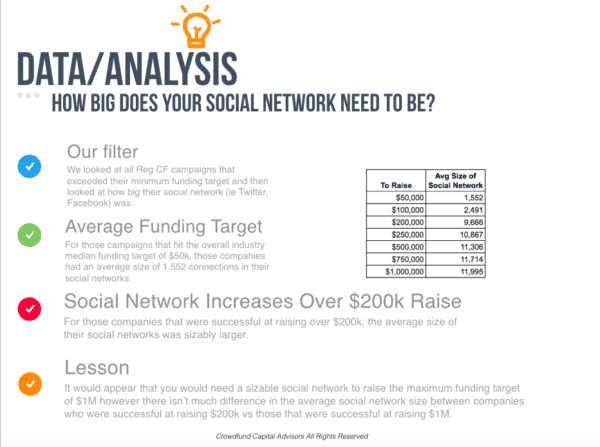

One of the biggest takeaways from the presentation was the importance of building your crowd first. CCA showed a strong correlation between having a well established network and the size of the raise.

Asked about this phenomena, Neiss said;

“You cannot crowdfund without a crowd. Having a great idea, great team and great business plan is a given as a starting point for Regulation Crowdfunding. However, you won’t be successful if you don’t have the crowd. Take the time to build your crowd, become an expert in your business online and learn how to communicate with your social network. The data shows that those entrepreneurs who have a strong crowd where they are engaged with them pre, during and post campaign are the ones who raise the most money.”

While there are challenges to any emerging sector, in general, response has been very positive regarding initial traction and the quality of issuers. Many of the fears expressed by some policy makers – have simply not materialized. Neiss said that both platforms and companies using the new exemption were taking a practical approach;

“The data shows that everyone (entrepreneurs, investors and platforms) seems to be approaching the market with logic. There is no hype from investors pouring money into deals they know are long-term and higher risk. The quality of the deal flow (particularly those that get funded) has been higher — those that lack quality barely get any commitments. The flow of capital is steady and increasing. And the data shows how all the variables of a crowdfunding campaign (not just including disclosures and video but size of the social network and type of security) are important to successful outcomes.”

One Reg CF platform was mentioned as not measuring up to rest. uFunding, a FINRA approved portal was questioned as to its approach. Recently there have been a flury of Reg CF filings for issuers using uFunding but little if no money invested in the offers. Neiss said all the deals, at last check, had been pulled from the site;

One Reg CF platform was mentioned as not measuring up to rest. uFunding, a FINRA approved portal was questioned as to its approach. Recently there have been a flury of Reg CF filings for issuers using uFunding but little if no money invested in the offers. Neiss said all the deals, at last check, had been pulled from the site;

“The other portals have videos, communication channels, social network connectivity, etc. All of these are critically important to the transparency of online finance and Regulation Crowdfunding in particular. These were lacking on uFunding portal.”

Of course the caveat being that none of these offers have been funded.

Asked about how the Reg CF market could be improved. Neiss commented on recent the legislative initiative taking place in the House and the Senate. Congressman Patrick McHenry crafted a bill called the Fix Crowdfunding Act. While stripped of some of the more important improvements before it crossed over the Senate, some believe wisdom will prevail and they will be added back. Neiss echoed what needed to be accomplished;

“First, Increase the cap from $1M to $5M. With higher caps on what entrepreneurs can raise, the industry can scale faster and those aspiring companies that don’t reside in Silicon Valley can access more capital. Second, get rid of the portal liability. Portals are technology players and don’t understand the detailed nuances of an issuer’s business or technology. To hold them accountable for material misstatements by an issuer is unfair and a deterrent to platforms wishing to enter the space. And third, allow the use of SPVs and funds. These will help issuers manage their cap tables, benefit investors that want to invest but are not sure where to put their capital and allow the industry to scale as well because those “friction bottlenecks” have been removed.”

CCA intends on doing quarterly webinar disecting market data. While it may be too early to call a trend they remain hopeful that Reg CF can become a powerful catalyst for providing access to capital to young, promising firms.