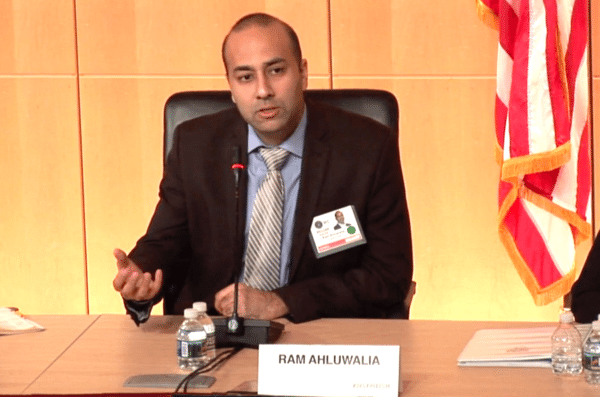

In the online lending world, there are a handful of people that know everything that is going on. From the good to the not so good, their vantage point is unique. Ram Ahluwalia, CEO and co-founder of PeerIQ, is one of these individuals.

Ahluwalia launched PeerIQ in 2014 as a provider of institutional credit risk analytics for the peer to peer lending sector. As online lending has morphed from a novelty to the future of debt, PeerIQ has been there chronicling the growth with its deep dive analysis of securitization and portfolio monitoring. PeerIQ provides institutional investors with tools for accessing and managing risk in the marketplace lending market.  PeerIQ’s analytics platform aggregates industry data from leading online lending platforms and generates sophisticated credit analytics and independent benchmarks. If you are in the online lending sector, you are reading PeerIQ’s marketplace lending securitization tracker.

PeerIQ’s analytics platform aggregates industry data from leading online lending platforms and generates sophisticated credit analytics and independent benchmarks. If you are in the online lending sector, you are reading PeerIQ’s marketplace lending securitization tracker.

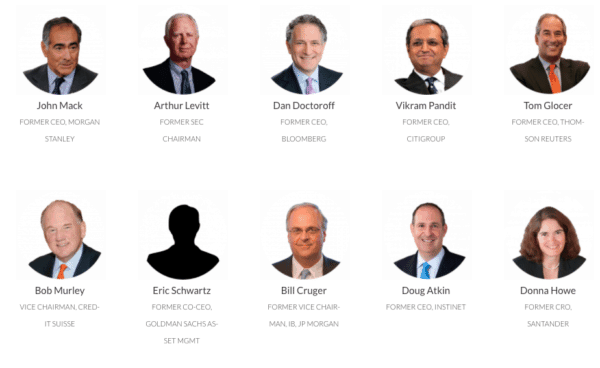

Ahluwalia has put together what may be the most prominent list of investors in the Fintech space. PeerIQ investors include finance rock stars like John Mack, Vikram Pandit, Tom Glocer, Arthur Levit, Doug Atkin and many more.

Ahluwalia recently shared with Crowdfund Insider his insight and perspective into the online lending industry. Our discussion is below.

Crowdfund Insider: 2016 was a challenging year for online lending. Any parting thoughts or comments?

Ram Ahluwalia: Last year highlighted that securing access to a diverse mix of low-cost capital is necessary to compete and win. Lenders that could tap many channels saw little to no slowdown in origination growth and maintained a healthy differentiation in funding cost and access to capital from their peers.

We also see evidence that institutional capital rather than retail capital will be the primary source of funding going forward. In particular, term capital from ABS programs, new ’40 Act funds, and bank partnerships are the core pillars of an institutional funding strategy.

Accordingly, we have seen platforms elevate the role of the capital markets function and invest in infrastructures such as data and analytics to improve investor confidence and execution. The effects we’ve seen has been tremendous. ABS issuances grew 60% in 2016 versus prior year, and virtually every major platform has established a securitization program and a bank partnership.

Crowdfund Insider: You have a unique perspective into online lending platforms. Many have experienced declines in lending during the past year. Which sector or platforms have experienced the largest declines?

Ram Ahluwalia: The decline in originations is overstated and misunderstood. The third quarter saw some origination decline, particularly for a couple of originators who encountered funding crunches, but year over year originations are still up across the industry.

And early indications from the fourth quarter suggests a quick rebound. Notably, the slowdown in growth is not due to borrower demand—it was entirely due to the funding constraints platforms experienced.

Crowdfund Insider: On the flip side, securitization has grown. Why is that?

Ram Ahluwalia: As we expected it too. Our business was founded on the premise that a substantial portion of these loans would find their way into bonds and bank balance sheets. As the queue for whole loan buyers tightened, platforms emphasized new funding channels including rated securitizations.

By transforming illiquid credit into marketable securities, lenders can access a much broader base of eligible yield-hungry investors in the debt capital markets, and access larger pools of capital at a lower cost of capital

Securitization has several other advantages too. Securitization provides permanent capital for platforms, whereas credit facilities are subject to roll-risk. Also, securitization programs can create a regular path to liquidity and financing for whole loan investors.

Crowdfund Insider: Do you expect securitization to continue to experience solid growth throughout 2017? What are the most significant catalysts necessary for this to occur?

Crowdfund Insider: Do you expect securitization to continue to experience solid growth throughout 2017? What are the most significant catalysts necessary for this to occur?

Ram Ahluwalia: Yes. We project securitization to continue to be a favored funding channel, with total ABS issuance volumes growing 50% in 2017. The same drivers observed in 2017 will persist—the need to for lenders to access large, diverse, funding sources.

Further, as consumer credit trends remain positive, there is a lot of demand for this ABS paper; the majority of deals remain oversubscribed.

Crowdfund Insider: Is peer to peer lending dead? Is it all hybrid lending?

Ram Ahluwalia: Peer-to-peer funding channels (or retail) is not dead.

Diversity of capital sourcing is critical, and those lenders who have built retail funding channels today will continue to retain them as part of their funding mix.

That said, we’re likely to see the form by which retail investors access consumer credit continue to evolve. Funds and ETFs—offered via RIAs as wealth management products—are more efficient avenues than directly marketing whole loans to individuals.

Further, we’re working with some platforms to craft financial products with different risk profiles that may appeal more to retail investors. Ultimately, though, institutional capital will remain by far the largest source of funding for the sector, as is the case in all fixed income asset classes.

Crowdfund Insider: What are your biggest regulatory concerns?

Crowdfund Insider: What are your biggest regulatory concerns?

Ram Ahluwalia: Lack of legal clarity around federal preemption and true lender issues continues to cast a shadow over ABS and other funding channels. We ultimately see such questions being resolved favorably for the industry, but policymaking via the courts is unfortunately not a fast-paced game.

Also, we’ve seen a wholesale preference for privately placed (Rule 144A) ABS transactions, due to the higher costs of public issuances and transparency concerns. We’ll start to see some public securitizations in 2017, led by leading online platforms, which will be a welcome development and further evidence of maturation of the online lending sector.

Crowdfund Insider: Do you believe the OCC Fintech Charter will become an opportunity for online lenders or just another costly regulatory mandate?

Ram Ahluwalia: The OCC Charter presents an optional path for Fintech lenders burdened by varied, state-by-state licenses rules. That said, the OCC Charter has not specified the capital and liquidity rules, and those requirements may be onerous for capital-light Fintech firms.

More generally, the OCC is trading-off an interest in promoting the safety and soundness of chartered banks and an interest in promoting financial inclusion and innovation. We believe the Charter will be awarded sparingly to large non-bank lenders or payments companies that exhibit bank-level compliance, strong management teams, data & analytics, and robust internal controls.

The OCC Charter is not a panacea. It does not address other financing and liquidity challenges for the industry. As a result, we believe partner funding banks such as WebBank and Cross River Bank will continue to have an important role to play.

Crowdfund Insider: How do you see traditional finance managing the digital lending ecosystem? Are we going to see more [Goldman Sachs] Marcus like platforms?

Ram Ahluwalia: Scaling up origination operations that can compete with online lenders (who have established brands now) requires significant investment in marketing, technology, servicing, and risk management.

It requires a top-level strategic push with high execution risk, brand, management, and regulatory implications, so it is not an undertaking for the timid.

While there is a large opportunity here for traditional financiers (with their noted cost of capital advantages), on balance, we predict most banks will try to partner with nimble lending platforms, acquiring benefits from the partnerships, while minimizing risks associated with such a major strategic push.

There will, of course, be exceptions. Goldman Sachs is a unique bank that has a strong risk management culture, and robust data and technology infrastructure. American Express already has a strong mass affluent brand and credit risk management capabilities. Large regional and money-center banks such as Wells Fargo or Bank of America similarly have existing origination, underwriting, and servicing capabilities.

Crowdfund Insider: What are your predictions for the online lending industry during 2017 in the US? What about Globally?

Ram Ahluwalia: We’re going to continue to see strong ABS growth and the formation of material platform/banking partnerships.

We’re also going to see the acceleration of lender consolidation; winners will be those with lower funding costs and sustained capital access or close focus on credit performance. Investors will increasingly focus on verification, monitoring loan modifications, monitoring underwriting standards, and ensuring they can perfect their interests and title to their loans.

Finally, to address some of the problems uncovered in 2016, there will be wholesale investment in funding infrastructure: improving data standardization, verification, validation, hot back-up servicing, and other transparency tools that are required to smooth the functioning of the online lending and ABS markets.

Finally, to address some of the problems uncovered in 2016, there will be wholesale investment in funding infrastructure: improving data standardization, verification, validation, hot back-up servicing, and other transparency tools that are required to smooth the functioning of the online lending and ABS markets.

Enabling the infrastructure is PeerIQ’s focus. We are excited to roll-out a number of offerings, several in partnership with TransUnion, to address the challenges for the category. We’re quite bullish on 2017.