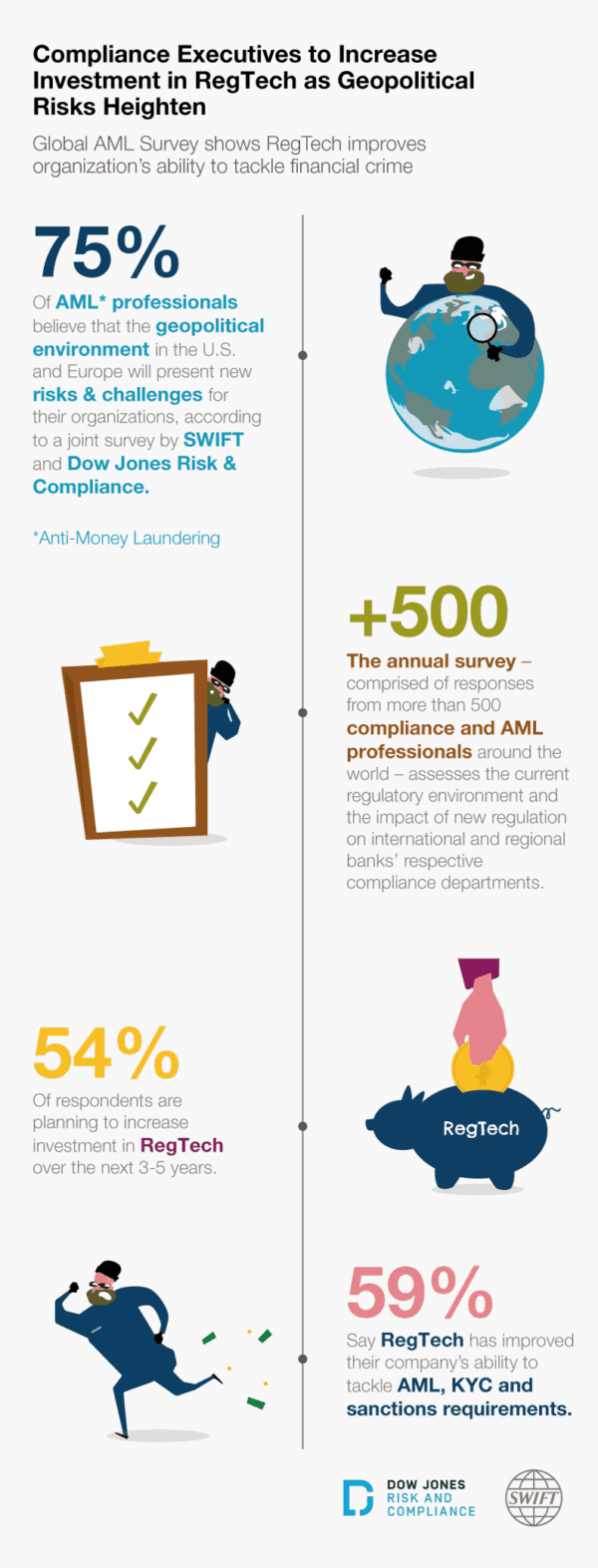

A large majority (75%) of anti-money laundering (AML) professionals believe the current geopolitical landscape presents new risks and challenges for preventing financial crime at their organisations, according to a joint survey by SWIFT and Dow Jones Risk & Compliance. To address these risks, more than half (54%) of respondents are planning to increase their investment in RegTech in the next three to five years, as the majority (59%) say technology has improved their company’s ability to tackle AML, KYC and sanctions requirements.

“The shifting geopolitical environment has created an additional layer of complexity for tackling financial crime around the world,” indicated Dow Jones Risk & Compliance Managing Director Joel Lange. “As the political and economic landscape continues to impact international trade, data protection, and tax cooperation, the need for greater transparency and more effective information sharing across borders is more important than ever.”

“The shifting geopolitical environment has created an additional layer of complexity for tackling financial crime around the world,” indicated Dow Jones Risk & Compliance Managing Director Joel Lange. “As the political and economic landscape continues to impact international trade, data protection, and tax cooperation, the need for greater transparency and more effective information sharing across borders is more important than ever.”

The annual survey – comprised of responses from more than 500 compliance and anti-money laundering professionals around the world – assesses the current regulatory environment and the impact of new regulation on international and regional banks’ compliance departments. As financial crime risks continue to evolve, increased regulatory expectations represent the greatest challenge (69%) for respondents, followed by concerns surrounding increased enforcement of current regulations (50%), and the need to understand regulation outside of their home jurisdiction (42%).

“Technology can play a key role in providing new and enhanced capabilities that strike a balance between preventing criminal activity, meeting regulatory requirements and containing costs,” stated SWIFT Director of Compliance Services Paul Taylor. “The most sophisticated financial crime compliance solutions help mitigate risks and boost efficiency in several ways, from managing workloads to automating payments monitoring and reducing false positives, enabling compliance teams to focus on more strategic risk policy and financial crime prevention work.”

“Technology can play a key role in providing new and enhanced capabilities that strike a balance between preventing criminal activity, meeting regulatory requirements and containing costs,” stated SWIFT Director of Compliance Services Paul Taylor. “The most sophisticated financial crime compliance solutions help mitigate risks and boost efficiency in several ways, from managing workloads to automating payments monitoring and reducing false positives, enabling compliance teams to focus on more strategic risk policy and financial crime prevention work.”

Specific regulations, such as the OFAC and EU 50% Rules as well as the FinCEN CDD Rule (both new in 2017 survey), are cited by over 70% of respondents as contributing to increased workloads for compliance departments. More than half of respondents say FATC3 and the Fourth EU Money Laundering Directive are regulations that add to existing workloads.

The survey also found that the greatest AML-related challenge currently facing organisations is having enough trained staff (57%), followed by the reliance on outdated technology (48%). Historically, most institutions manage their anti-fraud and AML activities separately; however the data shows an increase (66%) from last year (59%) of AML departments handling fraud detection and prevention. When it comes to managing fraud, risk data (90%) continues to be the most relevant source of information, followed by crime typologies (75%) and news (70%). For more information and to view the full results of the survey, please click here.