Last week Robo.cash surpassed a €4M investment milestone and briefly commented on new studies conducted by its analytical center. Today the Latvian P2P lending platform Robo.cash tweeted a detailed infographic and Founder and CEO Sergey Sedov explained the findings on TechBullion: the younger generation of investors who consider P2P lending as an advantageous and comfortable financial tool will contribute to the dynamics greatly.

According to Sedov, key takeaways from the research include:

1. The younger generation is speeding up

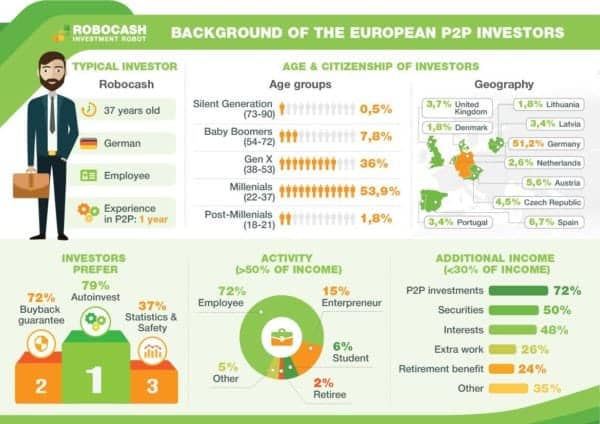

“With an account of stagnating interest rates on deposits in developed countries, as well as the cautious lending policies held by banks after the global economic crisis, alternative lending is attracting more and more investors and borrowers. Its volumes have grown drastically and the global scale is predictedto come close to $1 trillion by 2025. The increased volume of investments made by investors, who are already experienced in P2P lending, and a grown number of new investors help to maintain such a high momentum on the market,” Sedov explained. “Our own statistics of the P2P platform Robo.cash working in the European market since February 2017 shows that 22-37-year-old Millennials are steadily catching up with an elder generation of investors. This promises to create a favorable environment for the further growth of alternative lending globally. Six months ago, an average age of investors of the platform was equal to 38 years and age groups were distributed as follows: Silent Generation (73-90) — 0.8%; Baby Boomers (54-72) — 9.5%; Gen X (38-53) — 38.6%; Millennials (22-37) — 50.3% and Post-Millennials (18-21) — 0.8%. Today, the typical investor has grown younger to 37 years due to the increased share of investors under 37 years old: Millennials — 53.9% and Post-Millennials — 1.8%.”

“With an account of stagnating interest rates on deposits in developed countries, as well as the cautious lending policies held by banks after the global economic crisis, alternative lending is attracting more and more investors and borrowers. Its volumes have grown drastically and the global scale is predictedto come close to $1 trillion by 2025. The increased volume of investments made by investors, who are already experienced in P2P lending, and a grown number of new investors help to maintain such a high momentum on the market,” Sedov explained. “Our own statistics of the P2P platform Robo.cash working in the European market since February 2017 shows that 22-37-year-old Millennials are steadily catching up with an elder generation of investors. This promises to create a favorable environment for the further growth of alternative lending globally. Six months ago, an average age of investors of the platform was equal to 38 years and age groups were distributed as follows: Silent Generation (73-90) — 0.8%; Baby Boomers (54-72) — 9.5%; Gen X (38-53) — 38.6%; Millennials (22-37) — 50.3% and Post-Millennials (18-21) — 0.8%. Today, the typical investor has grown younger to 37 years due to the increased share of investors under 37 years old: Millennials — 53.9% and Post-Millennials — 1.8%.”

[clickToTweet tweet=”.@Robocash1 data proves that investors’ behaviour can be classified by several basic models but all of them pursue the only purpose to maximize profits. #fintech” quote=”.@Robocash1 data proves that investors’ behaviour can be classified by several basic models but all of them pursue the only purpose to maximize profits. #fintech”]

2. Income and activity of investors

“Following the results of a survey of investors from 15 European countries, half of the respondents (52%) have less than a year experience in P2P lending, one third (34%) have been investing from one to three years already. At the same time, a vast majority (72%) of investors are employees with a monthly income not exceeding €5,000 and only 2% of respondents estimated their monthly income to be more than €10,000. These findings greatly confirm the conclusion about accessibility of modern P2P lending. Other sources of income (extra work, retirement benefit, securities, etc.) are mainly additional for investors,” added Sedov. “However, if to consider sources of additional income only, then investments in P2P are standing out. In this context, they overtake securities, bank deposits and some other options of passive income. 54% of the respondents mentioned their income from P2P lending to have up to 10% within total income structure, and 17% indicated the range from 10% to 30%.”

“Following the results of a survey of investors from 15 European countries, half of the respondents (52%) have less than a year experience in P2P lending, one third (34%) have been investing from one to three years already. At the same time, a vast majority (72%) of investors are employees with a monthly income not exceeding €5,000 and only 2% of respondents estimated their monthly income to be more than €10,000. These findings greatly confirm the conclusion about accessibility of modern P2P lending. Other sources of income (extra work, retirement benefit, securities, etc.) are mainly additional for investors,” added Sedov. “However, if to consider sources of additional income only, then investments in P2P are standing out. In this context, they overtake securities, bank deposits and some other options of passive income. 54% of the respondents mentioned their income from P2P lending to have up to 10% within total income structure, and 17% indicated the range from 10% to 30%.”

3. Preferences determine the choice

“In search of comfortable and profitable ways to improve financial welfare, today’s investors prefer automated investments (79%) combined with a buyback guarantee (74%) both of which simplify portfolio management and provide a higher turnover. This is a characteristic of the European P2P platforms of a “new wave”, rather than traditional,” noted Sedov. “Another important feature typical for platforms particularly in Baltic which appeared on the market in the last years is in higher interest rates (over 12%) supplied together with a greater financial guarantee and accessibility for the EU residents.”

“In search of comfortable and profitable ways to improve financial welfare, today’s investors prefer automated investments (79%) combined with a buyback guarantee (74%) both of which simplify portfolio management and provide a higher turnover. This is a characteristic of the European P2P platforms of a “new wave”, rather than traditional,” noted Sedov. “Another important feature typical for platforms particularly in Baltic which appeared on the market in the last years is in higher interest rates (over 12%) supplied together with a greater financial guarantee and accessibility for the EU residents.”

4. Geography of investors

“According to the own figures of Robo.cash, Germany takes a leading place on the number of investors. According to the Cambridge Center for Alternative Finance (who released a new survey today,) its volume of the domestic market in 2016 was ranked third in Europe, after the United Kingdom and France. Considering a cross-border activity, Germany can be considered an unofficial European leader thanks to high incomes and the number of its population, and the national legislative restrictions on domestic investments,” observed Sedov. “At the same time, the majority of investors come from countries which are already familiar with alternative lending and have the necessary experience. This is usually supported by the developed special legislation (the UK, Spain, Austria, the Netherlands) or its active formation (Czech Republic, Latvia, Lithuania, Portugal, Denmark).”

“According to the own figures of Robo.cash, Germany takes a leading place on the number of investors. According to the Cambridge Center for Alternative Finance (who released a new survey today,) its volume of the domestic market in 2016 was ranked third in Europe, after the United Kingdom and France. Considering a cross-border activity, Germany can be considered an unofficial European leader thanks to high incomes and the number of its population, and the national legislative restrictions on domestic investments,” observed Sedov. “At the same time, the majority of investors come from countries which are already familiar with alternative lending and have the necessary experience. This is usually supported by the developed special legislation (the UK, Spain, Austria, the Netherlands) or its active formation (Czech Republic, Latvia, Lithuania, Portugal, Denmark).”

5. Tactics investors follow

“Results of the survey pointed that most investors diversify their investments usually working with several (81.2%) platforms, mainly four or more (50%). Each portfolio size is adjusted with regard to the effectiveness of funds. As a rule, money is invested gradually rather than at once. At the same time, the older the investor is, the more frequent withdrawals are, that is pointing an increased pragmatism of mature audience,” recapped Sedov. “Robo.cash data proves that investors’ behaviour can be classified by several basic models but all of them pursue the only purpose to maximize profits. For example, just starting investors prefer to invest “free” money in P2P lending, usually not more than €1,000 that appear from time to time. In contrary, experienced investors usually plan their budget, and they are ready both to make solid inputs at once and continue increasing portfolio by making frequent additional investments. The average portfolio size characteristic for various age groups confirms this: 18-24 years — €755, 25-34 years — €1,415, 35-44 years — €2,473, over 45 years — €2,958.”

“Results of the survey pointed that most investors diversify their investments usually working with several (81.2%) platforms, mainly four or more (50%). Each portfolio size is adjusted with regard to the effectiveness of funds. As a rule, money is invested gradually rather than at once. At the same time, the older the investor is, the more frequent withdrawals are, that is pointing an increased pragmatism of mature audience,” recapped Sedov. “Robo.cash data proves that investors’ behaviour can be classified by several basic models but all of them pursue the only purpose to maximize profits. For example, just starting investors prefer to invest “free” money in P2P lending, usually not more than €1,000 that appear from time to time. In contrary, experienced investors usually plan their budget, and they are ready both to make solid inputs at once and continue increasing portfolio by making frequent additional investments. The average portfolio size characteristic for various age groups confirms this: 18-24 years — €755, 25-34 years — €1,415, 35-44 years — €2,473, over 45 years — €2,958.”

6. Conclusion

Sedov concludes that 82% of respondents positively estimated their investment experience in P2P lending, while investors are planning definitely (37%) or most likely (46%) to increase investments at P2P platforms in the next two years.

“Such demand on investments proves the potential for the development of alternative lending. This is supported by a positive experience with existing P2P marketplaces and the growing interest of investors, young particularly, in a simple and reliable source of additional income with no significant restriction to an income level,” surmised Sedov. “Our own figures at Robo.cash confirm the idea: the platform attracted over €3 million and the number of investors exceeded 2,000 just in a first year of its work on the market.”

“Such demand on investments proves the potential for the development of alternative lending. This is supported by a positive experience with existing P2P marketplaces and the growing interest of investors, young particularly, in a simple and reliable source of additional income with no significant restriction to an income level,” surmised Sedov. “Our own figures at Robo.cash confirm the idea: the platform attracted over €3 million and the number of investors exceeded 2,000 just in a first year of its work on the market.”