Financial Innovation Now (FIN) represents some of the biggest names in tech when it comes to Fintech. These firms include Apple, Amazon, Google, PayPal, Square, and Intuit. Each of these big tech firms have a strong foothold in providing financial services and many observers expect the services provided to expand in the coming years.

FIN has published a report highlighting the importance of payment apps as more and more consumers shift to non-cash payments or non-plastic transactions. According to FIN, payment apps are a vital part of everyday life for millions of Americans.

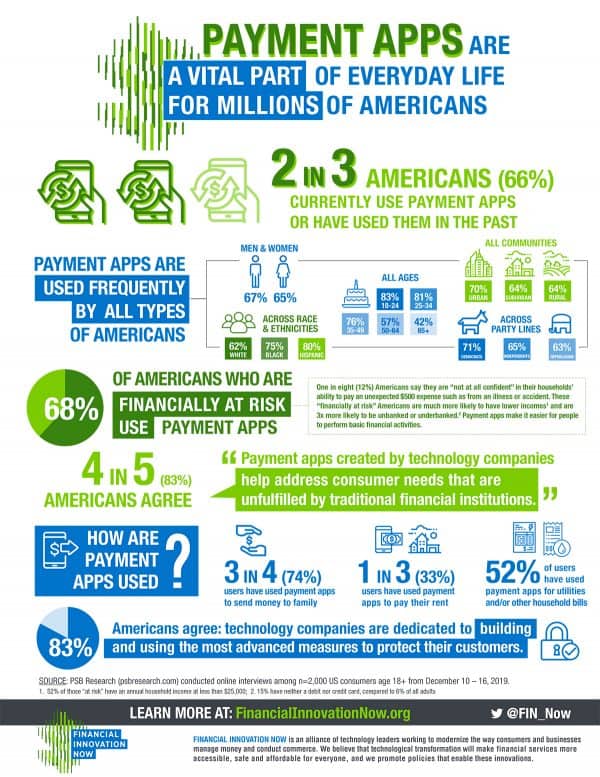

According to FIN’s survey, 2/3 or 66% of US citizens currently use, or have used, payment apps.

Four in five or 83% agree that “payment apps created by technology companies help address consumer needs that are unfulfilled by traditional financial institutions.”

Brian Peters, Executive Director of FIN, says technology companies are leading the way when it comes to payments – especially in the underserved markets.

“Millions of Americans rely on fast and innovative payment apps to make their life better and easier every day, and consumers trust technology companies to build and deploy the most advanced measures to protect their customers.”

The survey data, produced by PBS, is as follows:

- Fast and innovative payment apps are ubiquitous and have become a vital part of everyday life for millions of Americans

- Two in three Americans (66%) “currently” use payment apps or have used them “in the past”

- Payment app usage spans many key demographics – not only gender, age, race, but also geography, and political affiliation

- Payment app usage is common among men (67%) as well as women (65%)

- Though younger Americans are more likely to use payment apps (for example, 83% of those and 18-24 and 81% of those age 25-34), usage is pervasive among older Americans as well. 76% of Americans ages 35-49, and 57% of those ages 50-64 have used payment apps, and 42% of those age of 65 or older have used payment apps

- As it relates to race and ethnicity, payment apps have been used by 62% of Whites / Caucasians and usage even more commonly within minority communities such as Blacks / African Americans (75%) and Hispanics / Latinos (80%)

- Payment app usage spans the nation, evident by strong usage from those who live in the suburbs (64%) and in urban settings (70%), as well as those in rural communities (64%)

- Politics today often draws Americans apart – but not when it comes to using payments apps. 71% of Democrats, 63% of Republicans, and 65% of Independents use payment apps.

- Americans rely on fast & innovative payment apps to make their life better and easier: not simply bill sharing but also essential transactions such as paying rent and utilities

- 73% of Americans say payment apps are “a vital tool that people use to manage their finances,” including 30% who “strongly agree”

- 3 in 4 users (74%) have used payment apps to send money to family members

- 1 in 3 users – and half of users under age 35 – have used payment apps to pay their rent (33% and 49%, respectively); in addition, over half (52%) have used one to pay their utilities and/or other household bills

- Payment apps are embedded in people’s lives and 74% of Americans say that “restricting payment apps [would] disrupt people’s lives and make it more difficult for people to perform basic financial activities that they have become accustomed to and rely on” (Cont.) 2 © 2020

- PSB Payment apps are especially important to millions of Americans financially at risk

- Payment app usage is noticeably strong (68%) among Americans who are financially at risk, such as the one in eight Americans (12%) who say they are “not at all confident” in their households’ ability to pay an unexpected $500 expense such as from an illness or accident

- In fact, among these financially at-risk Americans, 79% agree payment apps are “a vital tool people use to manage their finances” and 77% say restricting payment apps would “disrupt people’s lives and make it more difficult […] to perform basic financial activities”

- Those who are financially at-risk are much more likely to have lower incomes (52% have an annual household income at less than $25,000) and are 3x more likely to be unbanked or underbanked (15% have neither a debit nor credit card, compared to 6% of all adults)

- Americans perceive innovative tech companies as playing a key role in fulfilling unmet needs not currently addressed by traditional financial institutions

- Four in five Americans (83%) agree that “payment apps created by technology companies help address consumer needs that are unfulfilled by traditional financial institutions

- Americans are 6x more likely to associate innovation with technology companies rather than financial institutions (“innovative”: 73% vs. 12%)

- Speed is also a major perceived strength of technology companies: 58% of Americans associate “fast” with technology companies over financial institutions (23%)

- Innovation and speed are key elements of security, and 83% of Americans agree “technology companies are dedicated to building and using the most advanced measures to protect their customers”

- Americans support fast and innovative payments apps and want more integration and cooperation between technology companies and the financial sector

- 9 in 10 Americans (89%) agree that “consumers benefit when technology companies and financial institutions work together”, including 43% who “strongly agree”

- 90% of Americans agree that “Innovations that benefit consumers should be encouraged – not restricted – and technology companies and financial institutions should work together more often.”