Mezu is a mobile payment app that allows sending and receiving money free, instantaneously, and privately. The app is available for download in both the App Store and Google Play.

On the privacy side, Mezu says it uses encrypted transaction codes to execute private person-to-person payments. Mezu users do not have to share their names, phone numbers, email addresses, or any other personal information to pay or get paid, according to the company. The company also offers a virtual debit card in partnership with Mastercard.

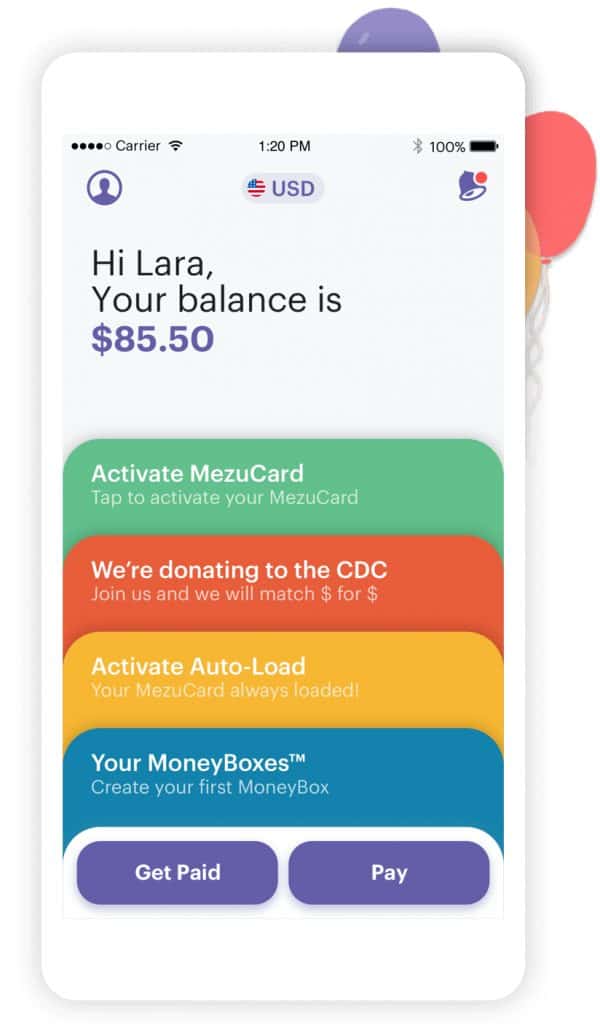

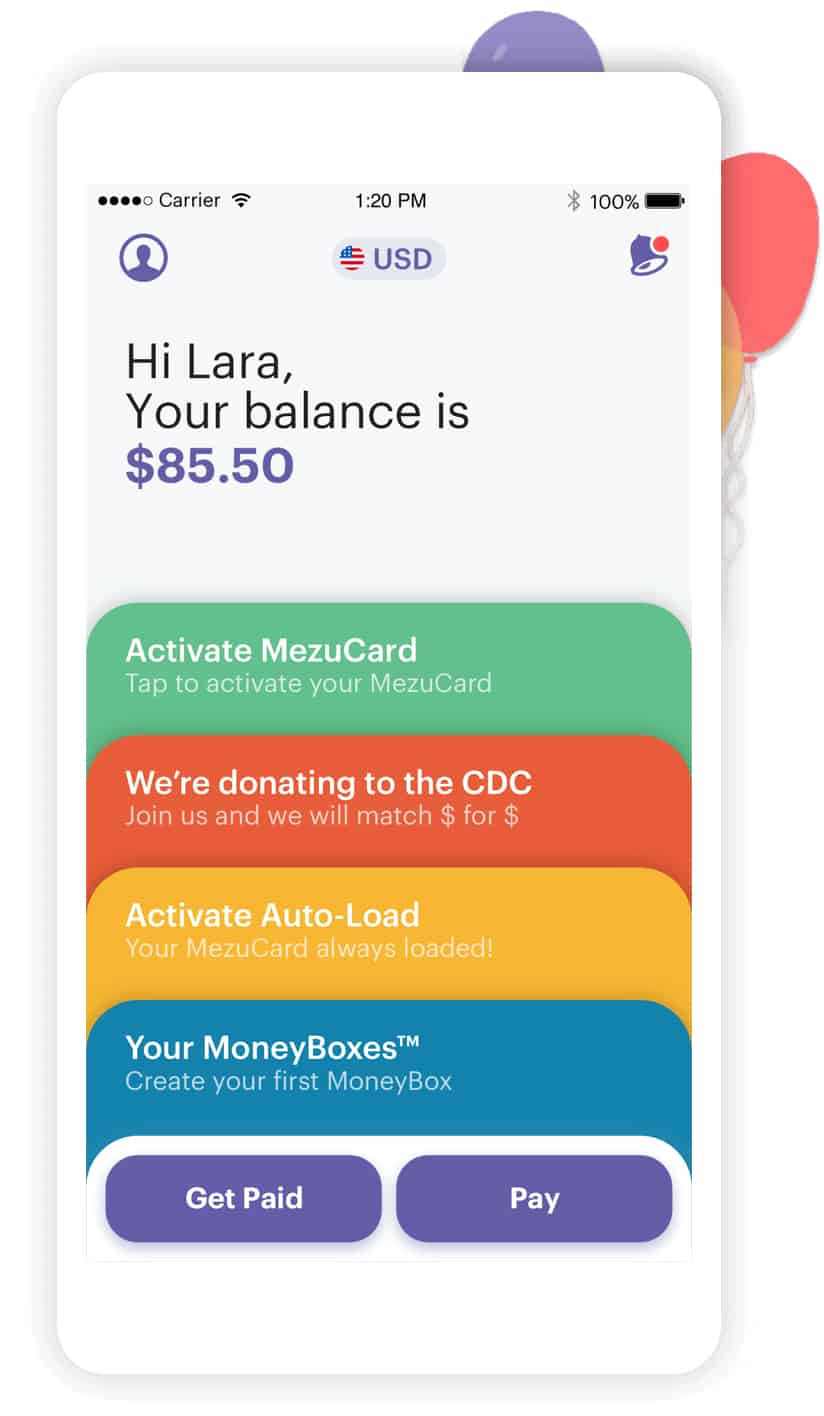

Earlier this week, Mezu announced the “Global Mezu MoneyBox” a method to send and receive money globally for Mezu customers. The company says the MoneyBox is a numbered public address for digital cash deposits where Mezu users can send money to users in a private and protected way from anywhere in the world. Mezu explains that it built the MoneyBox feature for the purpose of pooling cash, or donating anonymously to a charity, paying a service provider, an individual, a local business, with virtual cash, while protecting the identity of the payer from the payee.

So what about KYC/AML rules? Why is this better than PayPal/Venmo/Zelle etc.? We had to find out.

Crowdfund Insider connected with Mezu creator Yuval Brisker, an immigrant from Israel now based in Cleveland. Brisker co-founded TOA Technologies in 2003. After growing significantly, it was purchased by Oracle in 2013 for an undisclosed amount. TOA provided cloud-computing services that coordinated with customer service and repair people in the field. Reportedly, it was a global leader in the sector at the time of the acquisition. In 2012, TOA was said to be generating top-line revenue of over $40 million. In 2019, Brisker was recognized as one of the most interesting people in Cleveland.

Our discussion is shared below.

Why is Mezu different from all of the other payment apps already out in the market?

Yuval Brisker: The Mezu App is unique among peer to peer payment apps (such as Venmo and Cash App) in that it allows people to pay each other and get paid without having to reveal their identity or share any personal information like name, email address or phone number etc..

Along with traditional P2P payment methods (sending money to people you know via their email or phone number), Mezu provides users with additional ways to send and receive money: the CashCode, the MezuBox and the MezuCard.

The Mezu CashCode allows users to pay in person just like cash by generating a one-time, encrypted and, location-based four-digit transaction code. The payer shows to the recipient of the transaction the CashCode, which the recipient enters into their Mezu app and instantly receives the money. If not redeemed within 2 minutes, the code automatically expires.

The Mezu CashCode allows users to pay in person just like cash by generating a one-time, encrypted and, location-based four-digit transaction code. The payer shows to the recipient of the transaction the CashCode, which the recipient enters into their Mezu app and instantly receives the money. If not redeemed within 2 minutes, the code automatically expires.

Launching officially on May 5th is the Mezu MoneyBox, which is a new way to send and receive money globally* for Mezu customers (*available only for download within the U.S.). The MoneyBox is a numbered public address for digital cash deposits where Mezu users can send money to Mezu users in a private and protected way from anywhere in the world.

The MoneyBox is the ideal solution for those looking to give and collect money easily, conveniently and with zero fees. Mezu built the MoneyBox feature expressly for the purpose of pooling cash, or donating anonymously to a charity, paying a service provider, an individual, a local business, with virtual cash, while protecting the identity of the payer from the payee. The MoneyBox is simple, safe and free to use.

Last summer, Mezu launched the MezuCard, a virtual debit card, in partnership with Mastercard, which works instantly with Apple Pay and Gpay. The key differentiators of the MezuCard are that it’s a virtual-only debit card that can be activated and used instantly, and not like other US-based app debit cards it’s available for use internationally everywhere Mastercard is accepted. All of Mezu’s US competitors deliver Debit Cards as physical cards, so consumers must wait, sometimes for weeks, to receive a card.

Do all other payment apps sell your info? What about KYC/AML requirements?

Yuval Brisker: While apps like Venmo, Paypal, and Cash App are free to download, many users don’t realize their information is being shared with a host of other companies – with no option to opt-out.

A recent review on behalf of USA TODAY found that two of the most popular apps, Cash and Venmo, routinely pass on personal information to third-party data firms.

Mezu provides 100% privacy to its customers, not sharing, selling, nor giving access to any customer information, personal or transactional.

Like most P2P payment apps affiliated with the banking system, Mezu performs KYC and follows AML compliance procedures.

Who are your main competitors? Venmo? Apple Pay/Apple Cash?

Yuval Brisker: Venmo, Cash App, PayPal, Zelle.

How does Mezu generate revenue?

Yuval Brisker: Mezu is currently completely fee-free for its consumer customers.

When Mezu customers use the MezuCard Debit Card to purchase goods and services Mastercard charges those merchants interchange fees that are shared with Mezu.

For a limited time, Mezu is waiving other types of fees – however, Mezu plans to introduce various premium services in the future, which customers will be able to purchase on a subscription basis.

What about Bitcoin or other crypto transfers?

Yuval Brisker: While Mezu is built to support the use of any currency including cryptocurrencies, Mezu has not currently enabled cryptocurrencies.

We believe that Mezu’s patent-pending encrypted identity and transaction protecting technology lets Mezu provide all of the benefits of crypto – privacy, discretion, protection of identity and speed, without the disadvantages of crypto – i.e. volatility and liquidity.

Mezu is focused on making fiat transactions, both domestic and cross-border, as easy and non-invasive as possible.

Mezu is currently available in North America. What about Europe-Asia-Other regions?

Yuval Brisker: Mezu is poised to launch our financial services across the Americas and beyond. In the coming year, Mezu will launch in specific international markets, establishing us as the first truly global US-based mobile payment app.

What kind of transaction volume are you currently generating?

What kind of transaction volume are you currently generating?

Yuval Brisker: Mezu is set to reach 1 million downloads this quarter and grew 325% in 2019, with a record number of transactions in April 2020.

Mezu has seen a 60% increase in downloads since the start of March (during the beginning of social distancing.)

Will Mezu just focus on payments/transfers? Or do you intend on adding more features like digital banking features like Curve (UK)?

Yuval Brisker: Mezu already provides all the basic services of an FDIC-insured bank, as an integral part of its partnership with CFSB [Community Federal Savings Bank]. In addition, Mezu already provides a globally-enabled Mastercard debit card that can be used anywhere in the world that Mastercard is accepted.

In the coming months, Mezu will provide cross-border Foreign Exchange capabilities which will enable customers to send to and receive money from abroad instantly with a tap.

In the future, Mezu will also provide investment and trading services, as well as credit.