JPMorgan Chase (NYSE:JPM) is out with its annual report today and opening up the document is a letter from JPM CEO Jamie Dimon. The annual missive has emerged as the most widely read “dear shareholder” letter in the financial services sector as Dimon is broadly viewed as the best bank CEO in the world. As he typically has in past letters, Dimon addresses a plethora of issues and ideas pertaining both to JPM as well as society in general.

In regards to the growing competition attacking traditional banks, Dimon states, “Banks are playing an increasingly smaller role in the financial system.” While noting that he is in favor of competition, Dimon says that “U.S. banks (and European banks) have become much smaller in size relative to multiple measures, ranging from shadow banks to Fintech competitors and to markets in general.”

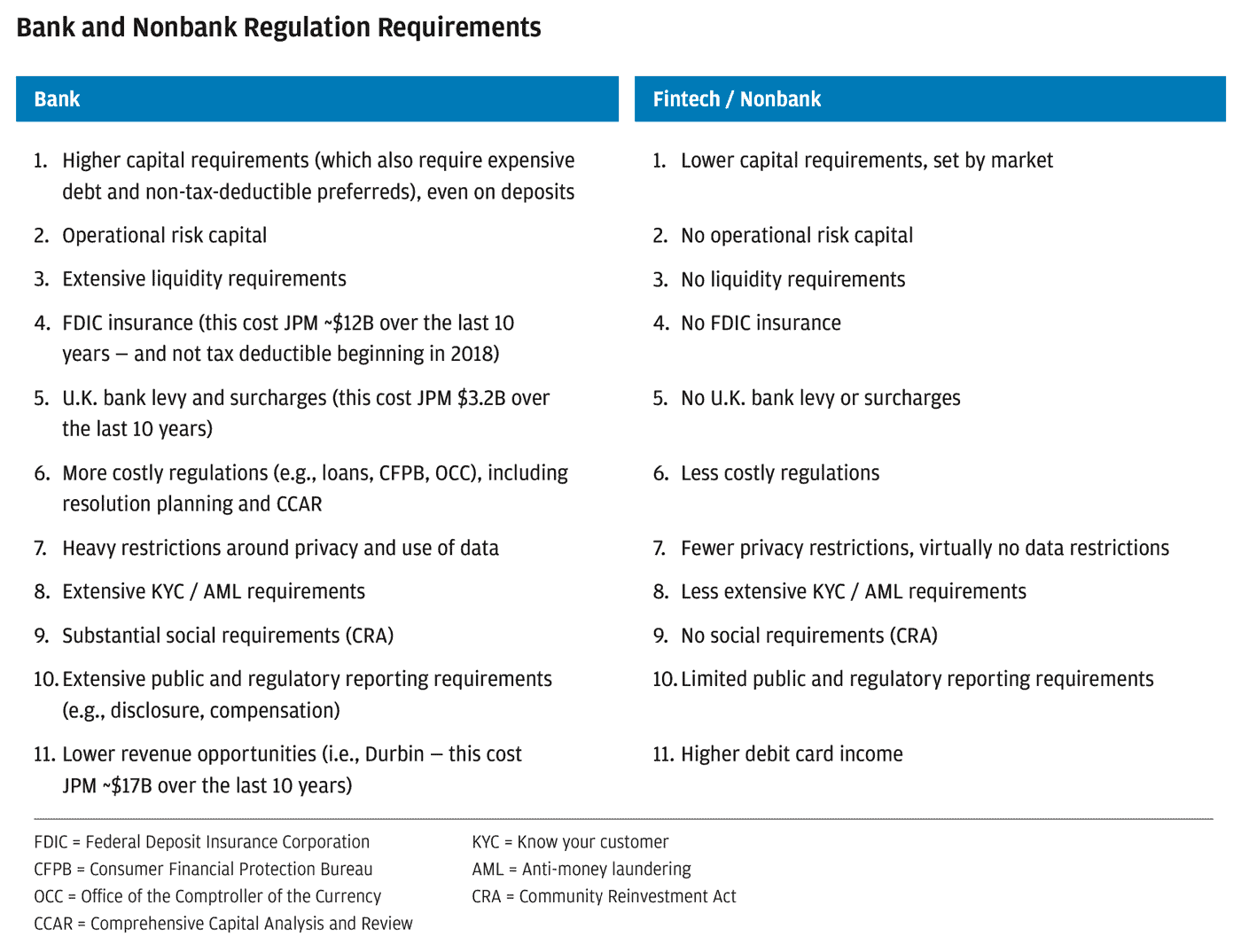

As Fintechs, big tech and other non-traditional firms offer financial services Dimon defends old finance stating that while some regulators may say that risk has moved out of the banking system – making banks safer – he defends his industry claiming that banks are reliable, less costly and consistent credit providers during goods times as well as bad.

“…transactions made by well-controlled, well-supervised and well-capitalized banks may be less risky to the system than those transactions that are pushed into the shadows.”

In Dimon’s opinion, banks are better regulated, in general, than Fintechs.

“We believe that many of these new competitors have done a terrific job in easing customers’ pain points and making digital platforms extremely simple to use. But growth in shadow banking has also partially been made possible because rules and regulations imposed upon banks are not necessarily imposed upon these nonbanks. While some of this may have been deliberate, sometimes the rules were accidentally calibrated to move risk in an unintended way. We should remember that the quantum of risk this unprecedented pandemic may not have changed – it just got moved to a less-regulated environment. And new risks get created. While it is not clear that the rise in nonbanks and shadow banking has reached the point of systemic risk, this trend is accelerating and needs to be assiduously monitored, which we do regularly as part of our own business.”

While criticizing the regulatory environment for Fintechs, a frequent refrain by incumbents, Dimon says that from loans to payments to investing, Fintechs have “done a great job.” The ability to approach financial services differently, merging social media and leveraging data, will “help these companies win significant market share.”

Admitting that Big Tech is morphing into financial services firms, Dimon admits their strengths are substantial but Big Tech is not without its issues:

“Their regulatory environment, globally, is heating up, and they will have to confront major issues in the future (banks have faced similar scrutiny). Issues include data privacy and use, how taxes are paid on digital products, and antitrust and anticompetitive issues – such as favoring their own products and services over others on their platform and how they price products and access to their platforms. In addition, Big Tech will have very strong competition – not just from JPMorgan Chase in banking but also from each other. And that competition is far bigger than just banking – Big Tech companies now compete with each other in advertising, commerce, search and social.”

While competition from agile Fintechs may be increasing, Dimon is confident that JPMorgan Chase will remain a robust challenger as financial services go through a rapid period of digital transformation.

“We have an extraordinary number of products and services, a large, existing client base, huge economies of scale, a fortress balance sheet and a great, trusted brand. We also have an extraordinary amount of data, and we need to adopt AI and cloud as fast as possible so we can make better use of it to better serve our customers. We need to make our extraordinary number of products and services a huge plus by improving ease of use and reducing complexity. We need to move faster and bolder in how we attack new markets while protecting our existing ones. Sometimes new markets look too small or appear not to be critical to our customer base – until they are. We intend to be a little more aggressive here.”

Calling for more regulatory scrutiny on Fintechs to “level the playing field” Dimon says he does not expect much to change and they will adjust their strategies appropriately. Dimon states that strategies going forward include acquisitions – in payments, asset management, data, and other services. And that is how JPM will go forward and hopefully survive and thrive.