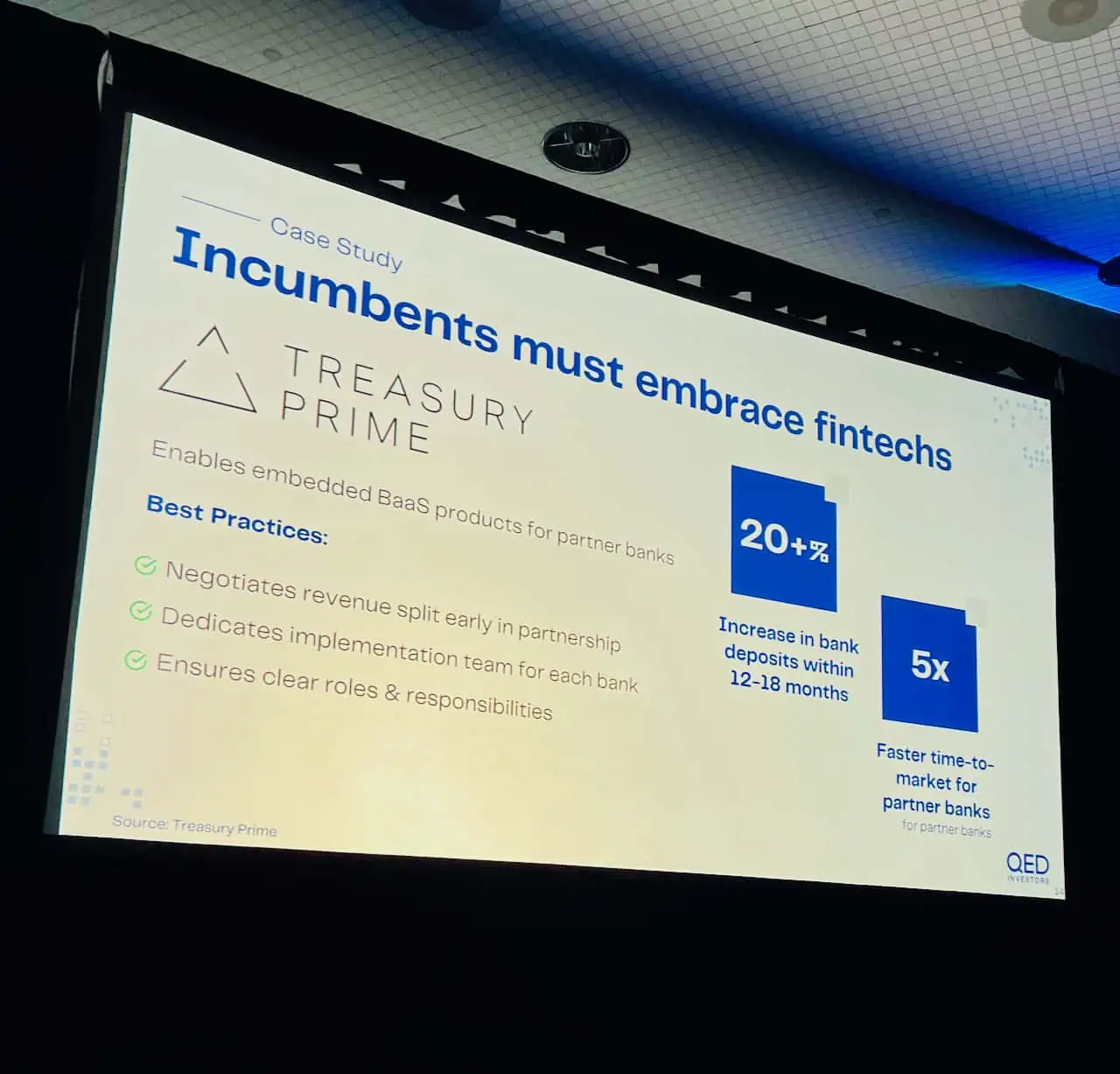

Treasury Prime, an embedded banking provider, is said to be laying off staff, according to a blog post. Today, the company has issued a statement outlining that it will shift its efforts to regulated banks.

Jason Mikula, posting on LinkedIn, claims that Treasury Prime has laid off about half its employees. He adds that the company has “struggled with high churn,” and some possible investors have hit pause due to the turmoil.

Treasury Prime says it is reorienting the company to focus on direct-to-bank partnerships. Mikula says they will “wind down” their services to Fintechs.

Chris Dean, CEO and co-founder of the Fintech, said the future of banking is embedded with regulated institutions and tech firms working to deliver financial services. This alludes to a shift from focusing on Fintechs or Neobanks to working with established banks as legacy firms transition to digital banking. Dean said the most successful Fintechs are working with banks.

“That is why Treasury Prime is doubling down on a “bank-direct” approach, and is launching a Bank-Direct product that makes it possible for any bank to build a safe and successful embedded banking business line,” said Dean.

Treasury Prime General Counsel and Chief Compliance Officer Sheetal Parikh stated that regulators want banks and other regulated financial services firms to oversee Fintech partners directly.

“We clearly see where embedded banking is headed and are following our customers that recognize that Treasury Prime’s bank-direct approach will ultimately create a safer and more sustainable ecosystem for all participants – banks, Fintechs, and partners alike,” Parikh explained

Going forward, Treasury Prime will:

- Focus its sales strategy on supporting banks as they close their own deals, including the development of automated screening tools to identify the Fintechs they want as partners and a new business development team to provide specialized advice.

- Enhance support for platform implementation and customer onboarding, including streamlining its contracts to make it clear to regulators that the bank directly oversees its Fintech customers.

- Provide more flexibility for banking institutions to tailor their partnerships with Fintech customers, deepen those relationships, and build their own Fintech brands.

- Optimize investments in personnel and infrastructure to drive bank-led, Fintech, and embedded banking partnerships.

Some policymakers have voiced their concerns about regulatory arbitrage utilized by neobanks and other Fintechs. Currently, there are only a handful of federally chartered pure digital banks.