Regulation Crowdfunding (Reg CF) was initially pigeonholed as a new exempt offering for smaller private firms to raise equity capital, so much so that many people described securities crowdfunding as “equity crowdfunding,” a term that is not really accurate.

Today, private firms pursue online capital formation across the realm of securities exemptions, including equity, convertibles, SAFEs, revenue shares/royalties, debt/term loans, and more. Equity or common shares (and SAFEs) tend to be riskier for investors. Most early-stage ventures fail; if you hold common shares, you are usually left with zero if a company collapses.

Debt, or business loans, are non-dilutive capital frequently used by more established firms to raise growth capital online. These securities tend to be less risky while potentially providing regular payments to investors. In a high-interest rate environment, debt issued from a crowdfunding platform can provide a higher rate of return than what you may expect from a savings account (currently around 5%).

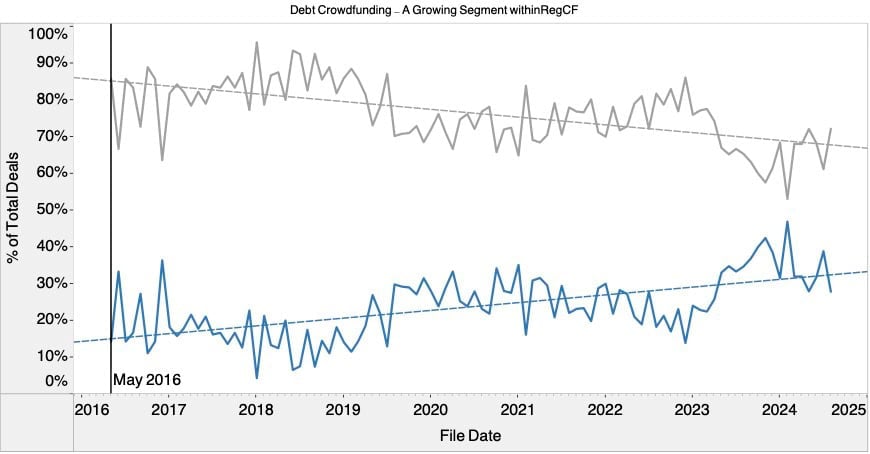

In the past several years, more private firms have leveraged online investment platforms to raise debt capital. According to Crowdfund Capital Advisors (CCA), debt offerings (plus Rev Share) comprised about 15% of all offerings when the Reg CF industry commenced. Debt has now gradually grown to encompass one out of every three offerings.

CCA outlines that this trend is increasing, with median interest rates of around 12.25% along with low default rates. These private securities offerings can be an interesting opportunity for investors and issuers – especially in a somewhat tight bank lending environment.

CCA co-founder and Principle, Sherwood Neiss, explains:

“The growth in debt offerings within Reg CF is a clear signal that both businesses and investors are recognizing the benefits of this financing option. For businesses, it’s about accessing capital efficiently while maintaining ownership. For investors, it’s about finding yield in a market where traditional options may not be as rewarding.”

In 2022, there were 330 debt offerings issued under the Reg CF exemption. So far in 2024, there have been 223 debt offerings and this sector of lending appears to be poised to top last year’s number.

Peer-to-Peer Lending 3.0

For firms in need of capital, an established business or an emerging one, can tap into the private markets to raise debt capital. As getting a bank loan can be an arduous task (and SBA loans demanding a lot of navigation), going to a Funding Portal or Broker Dealer that specializes in securities crowdfunding to get a loan – may make more sense than the traditional bank path. In fact, some crowdfunding platforms may be able to approve a loan in less than 24 hours.

At the same time, if a small business has a community presence, it may be able to tap into an existing customer base—individuals who appreciate the service or products and want to help keep the firm in business, to finance these loans.

Two examples of “bank replacement platforms” include Honeycomb Credit and SMBX. Both platforms can issue loans of up to $5 million.

This past March, CI spoke with Honeycomb Credit co-founder and CEO George Cook, who explained:

“It’s no secret that banks have moved dramatically upstream in the small business lending landscape. The average SBA loan in 2007 was $146,000, 15 years later in 2022 it was up to $543,000 – a 270% increase that makes SBA loans increasingly out of reach for most Main Street entrepreneurs. As competition grows more heated for larger commercial loans, fewer bank lenders are supporting younger and smaller businesses.”

Currently, loans issued on Honeycomb Credit typically range from around $25,000 to $250,000. In the past year, Honeycomb has emerged as one of the top issuers leveraging the Reg CF exemption.

SMBX is another bank replacement platform that issues “Small Business Bonds” financed by local residents, as well as, other investors. SMBX says it enables “small businesses to reduce borrowing costs and win customer loyalty.” SMBX touts its lower fees and fast approval process. The Small Business Bonds amortize over time with the business paying principal and interest to investors each month.

In a way, small business loans originated by Funding Portals or Broker-Dealers are the next iteration of peer-to-peer lending in the US; a sector of Fintech that rocketed into existence, transitioned to “marketplace lending,” which then diminished over time.

Platforms like SMBX, Honeycomb, and others are now stepping up to fill a void in finance pertaining to smaller firms accessing debt capital. Private debt markets (non-bank lending) are enormous and typically dominated by institutions and the wealthy. Private credit markets grew “exponentially, reaching $1.6 trillion globally in assets under management in 2023.” The report by Deloitte states that the “private credit market is expected to grow to $3.5 trillion globally by 2028” as banks lose market share.

These online investment platforms can provide a bank loan alternative for smaller firms. They may also offer smaller investors access to a growing sector of alternative finance that generates consistent returns at a lower risk level than an equity investment.