The SEC Finally Convenes on Crowdfunding Rules – Let the Sun Shine!

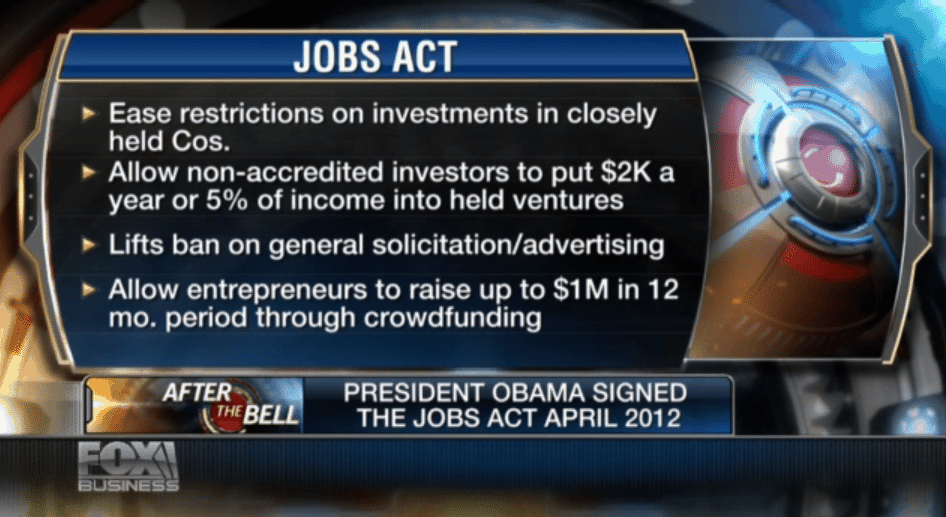

It had been more than 18 months since President Obama signed into law the multi-faceted potpourri entitled the Jumpstart Our Business Startups Act (the JOBS Act). One of the more controversial provisions of the JOBS ACT, Title III, entitled “Capital Raising Online While Deterring Fraud and Unethical Non-Disclosure Act of 2012” (“CROWDFUND”), outlined the parameters of a new and revolutionary vehicle intended to facilitate capital formation for startups and small businesses – Equity Crowdfunding – – harnessing the power of the Internet to attract capital from large numbers of investors seeking to invest small amounts of money in private companies in exchange for a piece of the action. Though the concept of raising large amounts of money from small, unaccredited investors was not a novel one, allowing companies to solicit investments from large numbers of unaccredited investors without the protections of an SEC registration and review process is something that has been largely prohibited under federal law since 1933.

It had been more than 18 months since President Obama signed into law the multi-faceted potpourri entitled the Jumpstart Our Business Startups Act (the JOBS Act). One of the more controversial provisions of the JOBS ACT, Title III, entitled “Capital Raising Online While Deterring Fraud and Unethical Non-Disclosure Act of 2012” (“CROWDFUND”), outlined the parameters of a new and revolutionary vehicle intended to facilitate capital formation for startups and small businesses – Equity Crowdfunding – – harnessing the power of the Internet to attract capital from large numbers of investors seeking to invest small amounts of money in private companies in exchange for a piece of the action. Though the concept of raising large amounts of money from small, unaccredited investors was not a novel one, allowing companies to solicit investments from large numbers of unaccredited investors without the protections of an SEC registration and review process is something that has been largely prohibited under federal law since 1933.

Adding to the controversy surrounding the JOBS Act were Title III provisions prohibiting states from regulating crowdfunded offerings – states could not engage in so- called “merit review” of crowdfunding investments. Generally, state merit review would be an absolute bar for startups and risky early stage companies seeking to raise money from unaccredited investors.

Though the JOBS Act provided a nine page blueprint for crowdfunding, it left the heavy lifting to SEC rulemaking – with a statutory directive that no later than 270 days following the enactment of the JOBS Act the SEC issue rules implementing the historic crowdfunding legislation.

The 270 day rulemaking period came and went – sans rules. Despite crowds of lobbyists and would-be service providers in and around the Washington Beltway; various directives and ultimatums from angry members of Congress; and letters from an impatient public; it seemed that for 18 months the only thing that Title III generated was controversy and speculation – when would the proposed rules be issued, what they would contain, and would crowdfunding prove to be a viable concept as an investment vehicle?

And Then There Was a Ray of Sunshine

As is often the case in Washingtonian business as usual, breaking “news” is often heralded by selective leaks to the press by Washington insiders. By this yardstick, it appears that it was business as usual last week in Washington, despite the best efforts of Congress to shut the government down.

Seems that Dave Michaels, a reporter with a reputation for covering breaking news at the SEC, was the first to scoop this story – reporting on October 17 and 18 on Bloomberg.com that the long awaited crowdfunding rules were targeted for a Commission vote on October 23.

Seems that Dave Michaels, a reporter with a reputation for covering breaking news at the SEC, was the first to scoop this story – reporting on October 17 and 18 on Bloomberg.com that the long awaited crowdfunding rules were targeted for a Commission vote on October 23.

Though overtaken with excitement at the prospect of crowdfunding finally getting off the ground, the lawyer in me was skeptical. Why would the SEC would be scheduling an open Commission meeting on less than seven days notice, as is normally required under the federal Sunshine Act? Normally the Sunshine Act requires not less than seven days advance notice of a Commission meeting unless agency business requires that the meeting be called on shorter notice. And it was hard to fathom what exigent circumstances might move the Commission to call a meeting on short notice for rules which were 18 months in the making, and were more than nine months overdue.

My skepticism gave way to disbelief on October 21, when the SEC published a “Sunshine Act Meeting Notice” announcing an Open Meeting of the SEC on October 23, 2013, to consider whether to propose rules and forms implementing Title III crowdfunding rules.

And alas, the October 21 Notice advised: “The duty officer has determined that no earlier notice was possible.” [Emphasis added]

Far be it from me to understand how apparently someone at the Commission, wittingly or unwittingly, had the time to inform the media of the upcoming Commission Meeting on October 17, but the Commission was unable to provide the statutory Sunshine Act Notice until two days before the Meeting. After all, the Commission had no difficulty complying with the seven day Sunshine Act notice period for all of the other prior JOBS Act rulemaking.

Was the shortened notice a conscious measure to implement “crowd control” at the SEC’s Open Meeting by cutting down the number of attendees?

The more troubling issue is that it appears by all accounts that outside parties may have had “special” access to the Commission in the JOBS Act rulemaking process – with advance knowledge of the exact meeting date – and if it turns out that Bloomberg Reporter Michaels is correct in his October 17 prognostication – specific terms of proposed crowdfunding rules regarding verification of investor eligibility.

For now, we can only go by what Bloomberg has told us as to its sources – “. . . two people with direct knowledge of the matter who asked not to be named because the proposal hasn’t been made public.”

It’s Washington Business as Usual? So What’s the Big Deal?

Some may say this apparent “leak” is simply business as usual in Washington. So what’s the big deal? I guess that depends on who you ask, especially in the context of a new financial market regulated by the SEC and FINRA – that has transparency and a level playing field as its core components, and is premised on the democratization of investing:

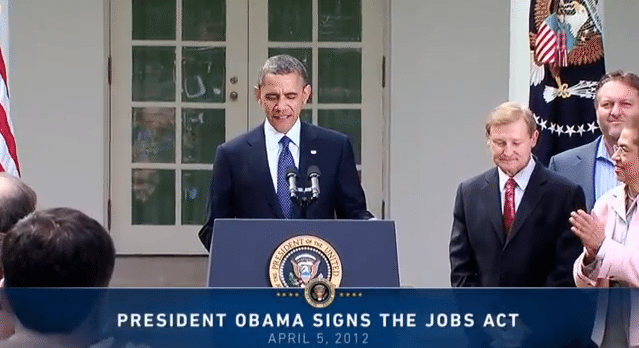

President Obama – He is the gentleman that signed the JOBS Act into law in the White House Rose Garden in April 2012 – a crowdfunding supporter who proudly stated:

President Obama – He is the gentleman that signed the JOBS Act into law in the White House Rose Garden in April 2012 – a crowdfunding supporter who proudly stated:

“For the first time, ordinary Americans will be able to go online and invest in entrepreneurs that they believe in.” But with the following caveat:

“Of course, to make sure Americans don’t get taken advantage of, the websites where folks will go to fund all these start-ups and small businesses will be subject to rigorous oversight. The SEC is going to play an important role in implementing this bill. And I’ve directed my administration to keep a close eye as this law goes into effect and to provide me with regular updates.” [Emphasis added]

Former Commissioner Elise Walter – And then there were the words of former Commissioner Walter at the last SEC JOBS Act Open Meeting on July 10, 2013:

Former Commissioner Elise Walter – And then there were the words of former Commissioner Walter at the last SEC JOBS Act Open Meeting on July 10, 2013:

“It is imperative that investors have confidence that the private offering marketplace has not turned into the Wild West. And it is important that investors know and understand that we are monitoring the marketplace and stand ready to implement any further appropriate protections. If investors lose confidence, then the market cannot succeed.” [Emphasis added]

Roosevelt Institute Fellow Georgia Levenson Keohane – This one time Fulbright Scholar recently made the following observations as to the importance of crowdfunding in her Policy Note published by noted New York think tank Roosevelt Institute on September 5, 2013:

“The emergence of crowdfunding represents a series of important new frontiers in the capital markets: social, commercial, and civic. The growth of the field, and of the opportunities for investors seeking financial, social or political returns with their individual and aggregated funds, will also require nuanced public policies that can nurture transparency, trust and safeguards necessary for them to flourish.” [Emphasis added]

The Sunshine Act – And then there are those pesky provisions in the federal Sunshine Act which prohibit ex parte (non-public) communications with interested outside parties, either to or from agency employees reasonably expected to be involved in the decisional process.

And This is Not the First Time That There is the Appearance of Special Access in the SEC Rulemaking Process.

It was less than a month ago, on September 23, 2013, that the rulemaking period closed on Title II JOBS Act proposed rules – only to be re-opened on September 27 for an additional 30 days. Yet consistent with my observations on Crowdfund Insider on September 27, it seemed that either the National Venture Capital Association was either “clued in” to the upcoming extension, or was clueless of the original September 23 expiration date, when it submitted its Comment Letter to the SEC on September 25, 2013. And then on September 27, 2013, the North American Securities Administrators Association (NASAA) belatedly filed its formal comment letter.

The Final Word –Tone is Set from the Top Down

Something is amiss in the Title III rulemaking process when issues of transparency and fairness can legitimately be called into question by the appearance of backchannel communications by a regulatory agency which is the gatekeeper of the financial markets. Even the appearance of impropriety cuts sharply against the grain of the crowdfunding philosopy, which is premised on the democratization of private investment markets and equal access to investment opportunities.

I submit that this is the wrong tone to set on the eve of crowdfunding regulations, and the wrong time to set it.

I leave the final word on this matter to SEC Chair Mary Jo White, who in recent public statements has sounded a chord of zero tolerance for lawbreakers in the world of securities regulation. Less than two weeks ago, Chair White made the following statements:

I leave the final word on this matter to SEC Chair Mary Jo White, who in recent public statements has sounded a chord of zero tolerance for lawbreakers in the world of securities regulation. Less than two weeks ago, Chair White made the following statements:

“It is important because investors in our markets want to know that there is a strong cop on the beat – not just someone sitting in the station house waiting for a call, but patrolling the streets and checking on things. . . . Investors do not want someone who ignores minor violations, and waits for the big one that brings media attention. Instead, they want someone who understands that even the smallest infractions have victims . . . .”

_________________________________

Samuel S. Guzik is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience. He is admitted to practice before the SEC and in New York and California. During this time he has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.

Samuel S. Guzik is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience. He is admitted to practice before the SEC and in New York and California. During this time he has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.