RateSetter, a leading UK peer to peer lending platform, has made a public call for a “refresh” on the Financial Services Compensation Scheme (FSCS). In a public statement RateSetter declared, “the time has come for the Financial Services Compensation Scheme to act its age”. RateSetter states there continues to be a huge lack of public awareness on the FSCS program and that “over half the nation [is] unhappy with receiving a lower rate in exchange for savings protection. In the same release, RateSetter touted its own platform and the assurances provided to lenders today.

RateSetter, a leading UK peer to peer lending platform, has made a public call for a “refresh” on the Financial Services Compensation Scheme (FSCS). In a public statement RateSetter declared, “the time has come for the Financial Services Compensation Scheme to act its age”. RateSetter states there continues to be a huge lack of public awareness on the FSCS program and that “over half the nation [is] unhappy with receiving a lower rate in exchange for savings protection. In the same release, RateSetter touted its own platform and the assurances provided to lenders today.

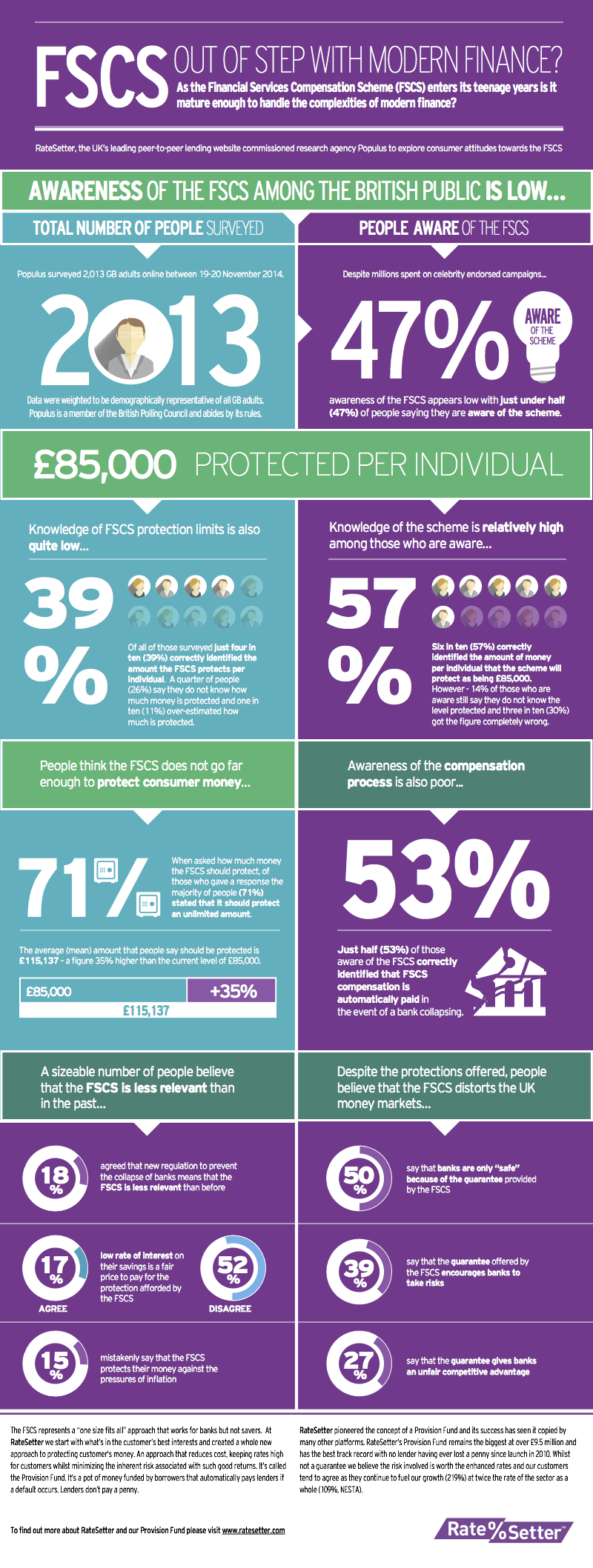

RateSetter recently commissioned a survey on the 13 year old program. The results from Populus apparently show that FSCS is “losing its relevance in the modern financial landscape”.

The data indicates that for those individuals aware of the FSCS program:

The data indicates that for those individuals aware of the FSCS program:

- one in five (22%) say they would not be worried if it ended

- Two in ten (18%) agreed that new regulation to prevent the collapse of banks means that the scheme is less relevant than before

- 17% of consumers believe a low rate of interest on their savings is a fair price to pay for the protection afforded by the FSCS.

- Over half (52%) of people disagree, showing that consumers are tired of getting a poor deal and are ready for a new breed of finance which can provide a level of protection whilst also giving them a much greater return on their investment.

- Only four in ten (39%) of those who were aware of the FSCS correctly identified the £85,000 of individual cover it provides

- One in ten (11%) over-estimating how much of their money is protected

- Majority (71%) stated that it should be unlimited, and the average based on all responses was £115,137 – a figure 35% higher than the current level of protection

RateSetter attacks the program further saying that despite many publicity attempts less than 47% of surveyed individuals are aware of the program.

Rhydian Lewis, Co-Founder and CEO, RateSetter, commented:

“Whilst the FSCS has been important for traditional financial institutions over the last decade, our findings tell us it is no longer fit for purpose. It is for this reason that its one size fits all approach has not been adopted by the burgeoning P2P industry. Instead, unique processes to protect customer’s money have been put in place by the key players in the market.

“RateSetter, for instance, pioneered the first Provision Fund in the market which remains the biggest at over £9.5 million and has the best track record with no lender having ever lost a penny since launch in 2010.

“However, the Provision Fund is by no means a guarantee, and we have worked hard to ensure transparency and education within this relatively young sector, so that consumers know their money isn’t fully protected, and can make an informed and intelligent decision on how to diversify their portfolio.

“By creating bespoke solutions for the industry, we have tried to ensure that our lenders are as protected as possible whilst allowing them to enjoy greater returns of up to 6%. Whilst we continue to strive to diminish the risk of P2P finance, it is paramount that the FSCS also takes heed of changing consumer sentiment and reacts accordingly.

“For too long consumers have suffered stagnant rates and with an upturn in the economy, the Scheme should work to become more efficient and allow a better deal for people’s hard earned money.”

The release also states that the RateSetter platform offers lenders the benefit of having cover beyond £85,000 so all their money is protected. RateSetter incorporates a “provision fund” that stands at approximately £9.5 million today and provides protection against borrower defaults. RateSetter reports that no investor has lost a penny since the platform launched in 2o1o.

The release also states that the RateSetter platform offers lenders the benefit of having cover beyond £85,000 so all their money is protected. RateSetter incorporates a “provision fund” that stands at approximately £9.5 million today and provides protection against borrower defaults. RateSetter reports that no investor has lost a penny since the platform launched in 2o1o.