EY conducted a survey from September to October of last year. They published their results in the heart of the holiday season which made them easy to miss but no less relevant. According to EY and Fintech Adoption Index, Fintech usage could double among digitally active consumers within the next twelve months. This is an interesting statement as some, more cynical types, have noted that Fintech startups are showing up on every street corner – posing the question; who is using all of this cool stuff?

EY conducted a survey from September to October of last year. They published their results in the heart of the holiday season which made them easy to miss but no less relevant. According to EY and Fintech Adoption Index, Fintech usage could double among digitally active consumers within the next twelve months. This is an interesting statement as some, more cynical types, have noted that Fintech startups are showing up on every street corner – posing the question; who is using all of this cool stuff?

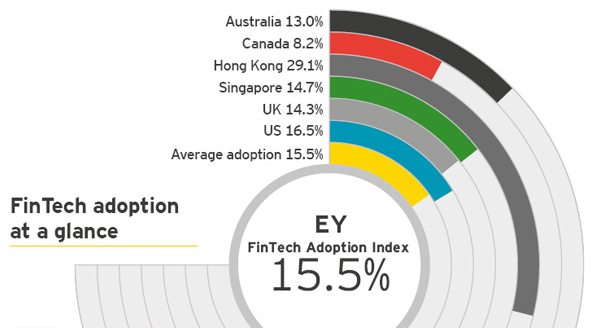

The data from EY polled 10,131 digitally active consumers in Australia, Canada, Hong Kong, Singapore, the UK and the US. According to their results, just 15.5% have used at least two Fintech services in the past 6 months.

And who is using all of this hot tech that seeks to make our lives easier and more enjoyable? Young, savvy and generally more affluent individuals. Of course as these consumers age, the adoption rate should increase and acceptance will broaden.

And who is using all of this hot tech that seeks to make our lives easier and more enjoyable? Young, savvy and generally more affluent individuals. Of course as these consumers age, the adoption rate should increase and acceptance will broaden.

Those between the ages of 25 and 34 years old used Fintech the most at 25.2%, followed by those aged 35 to 44 at 21.3%, and those aged 18 to 24 17.7%.

And which services are they using? Payment services are at the top of the heap at 17.6%. Savings and investments come in at number 2 with 16.7% utilization.

Also, as one would expect, urban financial centers were the hotbeds of utilization. New Y0rk, Hong Kong, and London were 1,2 and 3 for usage.

EY attests that ease of use remains one of Fintech’s key selling point. Lack of awareness or knowledge of services is the single largest hurdle to greater adoption. But of course getting the message out takes time – and money.

For most individuals engaged in the sector, these numbers are more reassurance as opposed to a surprise. Really the message is for traditional finance to wake up and embrace change as finance is inevitably moving completely online. EY states that, while banks are not standing still, it is Fintech that is setting the pace. Old school finance must deal with; regulatory compliance, legacy operations, antiquated IT infrastructure, ossified culture and executives resistant to change. Banks need to decide whether to; build, borrow, invest, fund or buy? Or perhaps all of the above. But they need to decide soon.