While the price of bitcoin and most cryptocurrencies is experiencing one of its frequents crashes, the French government and the French regulators are steadfastly working hand in hand to make France a cryptoasset-friendly country.

After tackling the issue of initial coin offering (ICO) regulation and ICO’s access to banking earlier this year, the French government is now proposing to change the tax regime for cryptoassets. A clearer tax regime for private crypto-owners and occasional traders was considered a major missing block in French crypto-ecosystem.

Second Attempt this Year

When the tax office took notice of cryptocurrencies and cryptoassets in 2014, its doctrine was to tax occasional cryptogains as “non-commercial profits” and profits made by professional traders and miners as commercial profit. For individual taxpayers, this resulted in a taxation of between 17.2% and above 60%, depending on each person’s marginal income tax rate. This tax regime was relatively complex—which gave many a good excuse not to report their crypto-earnings to the tax authorities.

In April 2018, the French Council of State invalidated this scheme. It ruled that gains from the occasional sale of cryptoassets should fall into the category of personal property sales gains, like the sale of furniture or other goods. That decision leveled out the income tax for occasional cryptotraders to 36.2% (19% income tax plus 17.2% social contributions)—hence, a significant reduction for high-income taxpayers. The regime for professional cryptotraders and miners remained the same.

Now six months later the regime is changing again. Hopefully for good.

Digital Assets, Flat Tax, Tax Form

The current proposal is part of the government’s financial budget law for 2019. It was approved in its first reading vote by the National Assembly. It intends to harmonize the definition of cryptoassets across the tax office and financial regulators by aligning it to the notion of “digital assets” put forth by the PACTE law.

The PACTE law, which has yet to get final approval by the chambers, separates cryptoassets from securities. It proposes a voluntary-only ICO regulation scheme. Issuers of non-security tokens who fulfill legal requirements such as KYC, AML, and escrow will be able to apply for an ICO visa. Their ICO will be whitelisted.

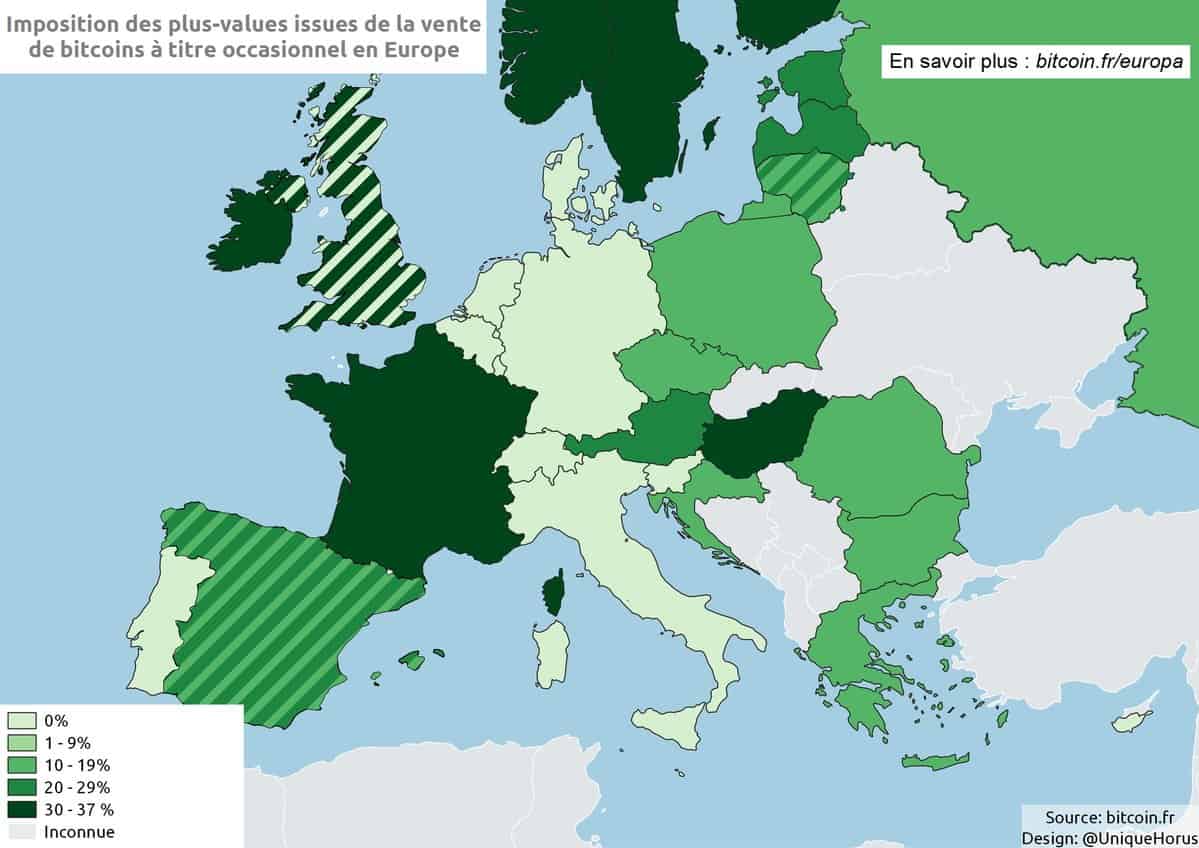

Now to the new tax regime. Gains above €305 on the sale of crypto-assets made by private individuals on an occasional basis will be taxed at the flat rate of 30%. This tax regime which includes 12.8% income tax and 17.2% social contributions, is the standard tax regime applied to capital gains.

The law also clarifies how cryptoasset gains will be recognized. Intra-crypto transactions are neutralized. Gains are counted at cash-outs, i.e. conversion into fiat currencies or purchase of goods. Gains are recognized using a prorate method similar to the one used in valuing securities portfolio gains.

Last but not least, taxpayers will have to list their cryptoasset accounts held in France or abroad on their tax form.

Mixed reactions

Reactions were quite mixed, to say the least.

While the flat tax represents a cut from previously proposed tax regimes (at least for high-income taxpayers), 30% remains on the high end of crypto-taxation in Europe, as French media bitcoin.fr pointed out.

Many observers contradicted the Minister of Economy, Bruno Lemaire, who stated that a 30% taxation rate made France attractive.

For most lawyers, however, the new regime is a welcome improvement. As Xavier Rohmer and Leslie Valloir of the law firm August Debouzy declared:

“Overall, we can welcome this turnaround and that the legislator has seized the issue. The tax administration and the Council of State did not have the legal capacity to give digital assets a more competitive tax treatment.”

Tax lawyer and tax expert for the French Cryptocurrency Management Association, Benoit Couty agrees. In his opinion, the new tax regime is definitely a step in the right direction, towards creating much needed “clarity, predictability, and security.”

In the name of the association, Benoit Couty advocates additional rules regarded as necessary to create a comprehensive and truly attractive tax regime for cryptoassets in France.

In the name of the association, Benoit Couty advocates additional rules regarded as necessary to create a comprehensive and truly attractive tax regime for cryptoassets in France.

- An optional “ad valorem” taxation at a reduced rate where the acquisition cost of crypto-assets is not known.

- A full tax exemption of purchases of goods and services paid with crypto-assets up to a reasonable amount per year.

- A simpler computation of the taxable gain, involving an immediate set-off of acquisition costs against subsequent cash outs instead of a prorate computation.

- A specific tax deferral upon investing crypto-assets to a company for business purposes.

- A clearer set of criteria distinguish private vs professional crypto-trading.

- A specific tax regime applicable to free tokens granted to employees under eligible profit-sharing schemes.

- A dedicated and consistent tax regime for crypto-miners.

- A clearer definition of conditions required to defer revenue for corporate income tax and VAT purposes for companies issuing tokens to the public (ICO).

Therese Torris, PhD, is a Senior Contributing Editor to Crowdfund Insider. She is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique.