Canada may be a smaller market but it has a robust, highly sophisticated economy and a vibrant Fintech sector. Toronto, the financial center of the country, is home to dozens of Fintechs including payment firms, online lending, AI, wealth management, blockchain and more. Yet while there are promising indications of financial innovation and a good number risk-taking Fintech entrepreneurs, a recent Canadian report noted a “need for a clear Fintech strategy by the federal and provincial governments with the intent of supporting innovation and growth for the Canadian financial services sector.”

Like most other industries, competition in financial services is intense. As it is a highly regulated sector of industry, participants must continuously manage compliance demands while interacting with diverse public officials and regulatory requirements. These same rules, if duplicative or misaligned, can act as a barrier to positive innovation and change that challenges established firms and entrenched orthodoxies.

The emergence of Fintech and the digitization of financial services, from banking and beyond, has seen multiple Fintech centers of prominence emerge. The UK has long been known for its Fintech friendly regulatory environment. Regulators frequently engage with emerging new business models as it is mandated for these officials to foster competition.

In Hong Kong, an important global financial center, public officials have not only talked about fostering Fintech innovation, but much money and resources have been dedicated to encouraging innovation. Fintech is viewed as strategically important to maintain a dominant position in the global financial industry.

So can Canada do more?

Crowdfund Insider recently reached out to Michael King for his perspective on the status of Fintech in Canada. King is co-Director of the Scotiabank Digital Banking Lab at Ivey Business School and an advisor to the National Crowdfunding and Fintech Association of Canada. He spent multiple years in the private sector working in the global banking industry so he has plenty of hands-on experience.

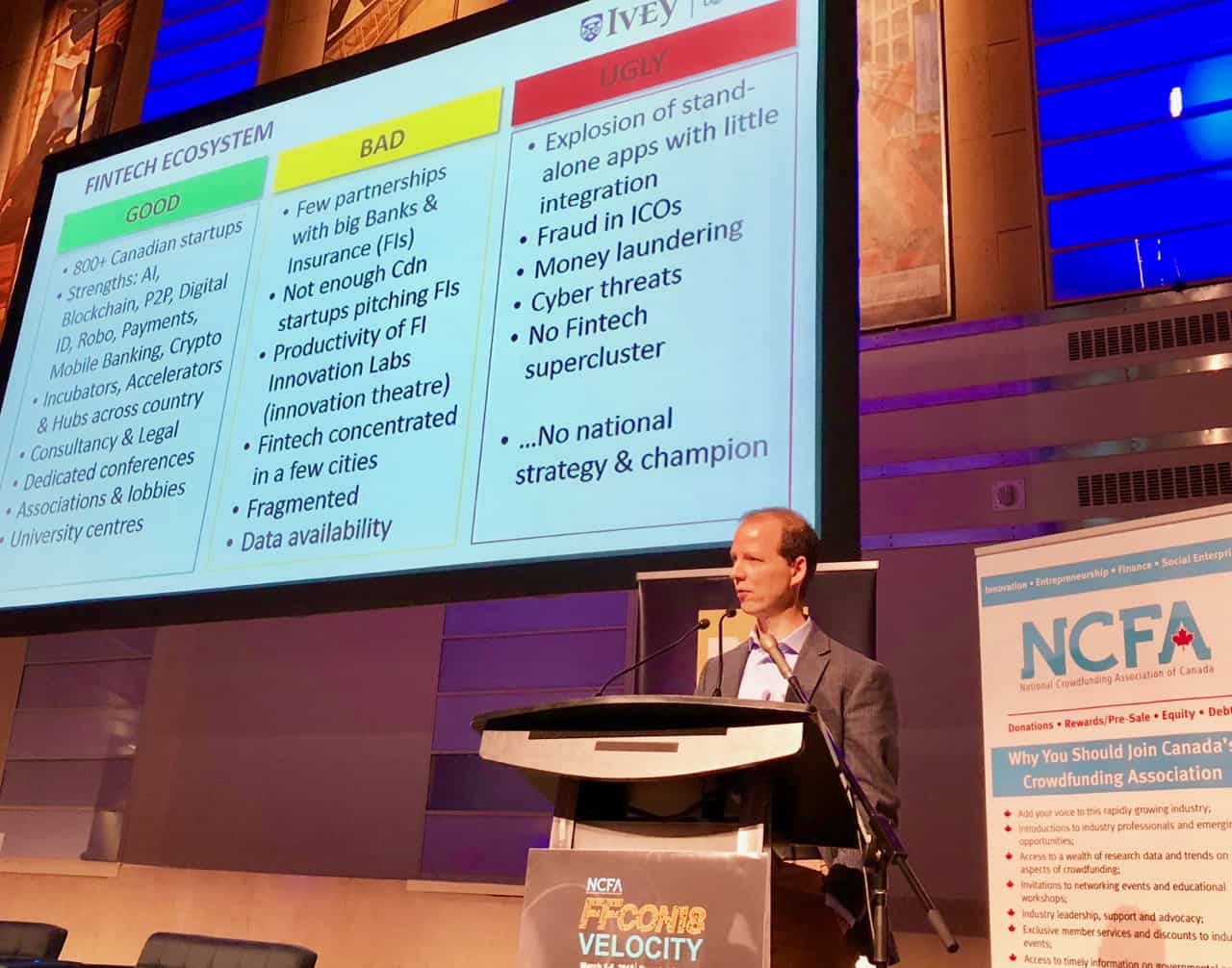

King recently created a helpful database of Fintechs operating in Canada which provides a good overview of these new firms. King believes Canadian officials, both regulatory and elected, must do more to catch up in the international race to remain relevant and competitive in the global financial sector.

So will Canadian policymakers listen? Our conversation is shared below.

Which international jurisdictions do you believe are doing the best in fostering Fintech innovation?

Michael King: The leading jurisdictions for Fintech are the UK, Australia, Hong Kong, and Singapore. Each of these countries has outlined a national strategy to be a leader in Fintech and is coordinating both public sector and private sector bodies towards achieving this goal. These small open economies understand that financial services are a global industry that has been opened up to foreign competition by the internet, cloud computing, smartphones and other technologies.

Canada is lagging, with no coordination nationally and harmful competition between Fintech centres across Canada.

Which sectors of Fintech do you believe hold the most promise?

Michael King: The payments sector is the front line of the battle between Fintechs and incumbents. This trillion-dollar industry is complex, with many players collaborating and competing in overlapping networks. Consumers and businesses face many pain points, such as high costs, slow transfers, poor service and little to no transparency. Payments is where the largest and most successful Fintech companies have made their mark, led by PayPal, Square, Stripe and Adyen.

Canada’s Lightspeed POS is the leader in this space, although there are dozens of smaller start-ups targeting lucrative segments of this value chain.

Payments is also the space where global technology companies are able to compete most effectively by bundling payments with their other customer offerings: Alipay (Alibaba), Amazon Pay, Apple Pay, Google Pay, Samsung Pay and WePay (Tencent).

These “Techfins” have put technology first and financial services second when developing their ecosystems. But access to customer payments will bring data and insights to drive future financial product offerings.

On relative terms, how does Canada size up when it comes to Fintech innovation?

Michael King: Canada remains in the top 10 for Fintech innovation with investment by both start-ups and incumbent banks, insurance companies and asset managers.

Canada has been gaining ground in key areas of Fintech, namely payments, cryptoassets and blockchain, online lending, and wealth management.

On a public policy basis, what has been done so far?

Michael King: Federal politicians in Canada are pursuing a policy of benign neglect towards the Fintech sector, preferring to leave policy to provincial governments and regulators while focusing on other innovation priorities. Canada has not published a national strategy on Fintech, none of the funding for superclusters was directed to Fintech, and no politicians are offering speeches to support this sector. The only recent indication of support is the public consultations on open banking, which has already been adopted in the European Union, United Kingdom and Australia.

Canada prefers to be a follower on open banking, balancing the need for more openness with the desire to maintain a sound and stable financial system.

What about regulators? Are they encouraging innovation in financial services or is the risk to grand?

What about regulators? Are they encouraging innovation in financial services or is the risk to grand?

Michael King: Canada’s regulatory system for Fintech is complex, costly and chaotic. It is stifling Fintech innovation, with overlapping jurisdictions and mandates that are not being coordinated.

In your opinion, which policies should be pursued to foster more innovation? Regulatory change? Access to capital? Other?

Michael King: The key policy to promote Canada’s Fintech industry is to adopt a national Fintech strategy, where the federal government coordinates the efforts of other levels of government, streamlines the regulatory framework, consults with the private sector on desirable policies, and promotes public sector procurement to support Canadian Fintech entrepreneurs.