Rising interest rates, giga-high inflation, and a wobbly economy is having a profound impact on the housing market, according to data from Proptech Redfin (NASDAQ: RDFN). The company reports that home sales and listings in the US have tanked by 20% during the month of September.

Redfin states that the number of homes sold dropped by 25% year over year, and new listings fell 22%—the largest declines since May 2020 and April 2020, respectively.

Redfin Economics Research Lead Chen Zhao said that housing is at a standstill, but the causes are very different than what happened at the beginning of the pandemic. This time it is rising mortgage rates and many people are staying put after re-financing their homes at a very low rate.

“The housing market is going to get worse before it gets better,” said Zhao. “With inflation still rampant, the Federal Reserve will likely continue hiking interest rates. That means we may not see high mortgage rates—the primary killer of housing demand—decline until early to mid-2023.”

Approximately 60K purchase agreements were canceled in September, or 17% of homes under contract.

In regards to pricing – many cities are still showing increases, but three metros saw year-over-year price declines: New Orleans (-5.7%), Oakland, CA (-2.1%) and San Francisco (-1.9%).

In looking at inventory, Austin, TX, saw the largest increase in the number of homes for sale, up 41.4% year over year, followed by North Port at 41.3%, Nashville – at 36.9%, Las Vegas – at 34.1%, and New Orleans – at 31.9%.

The median sale price versus the month prior was $403,797, a decline of 0.5%. Year over year the median price is still higher at 7.6%.

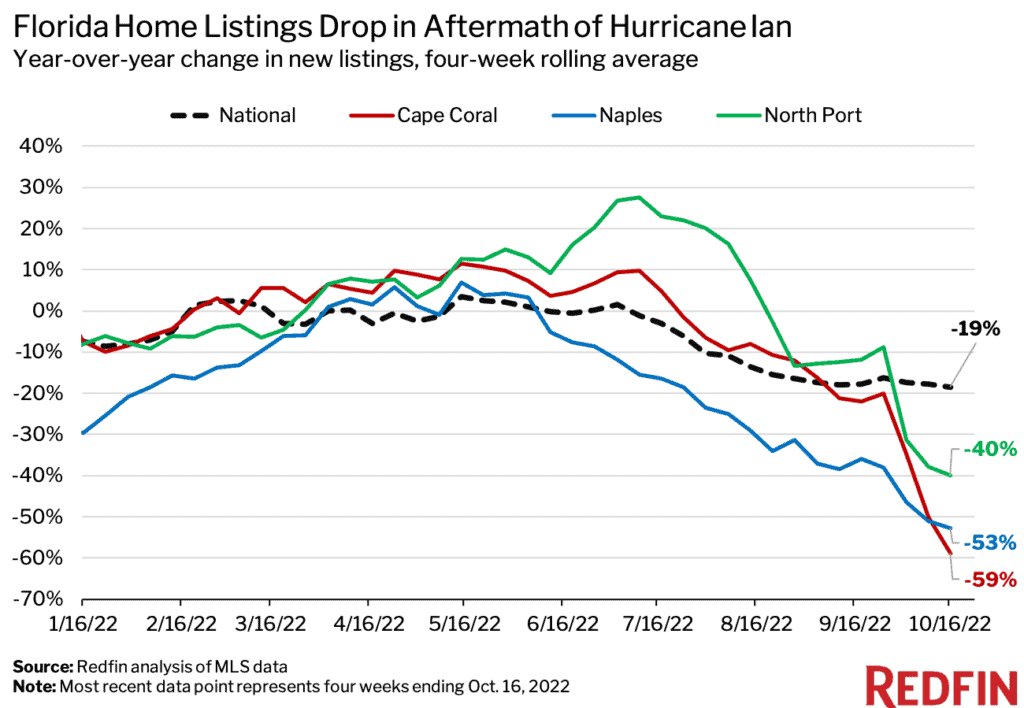

In looking at the hot Florida market, Hurricane Ian has taken a severe toll on housing. Pending home sales cratered by over 50% in three markets, including Naples, North Port, and Cape Coral.

Other Florida markets experienced significant declines, including a drop of 47% in Miami, 46% in Jacksonville, and 43% in West Palm Beach. Home sales were down more than 40% in Deltona, Tampa, and Orlando.

If one of the unspoken goals of the Federal Reserve is to cool the housing market, it is working.

Redfin anticipated the housing market rout this past summer by announcing layoffs as it prepared for a challenging economy.