Apple (NASDAQ:AAPL), one of the largest Fintechs in the world, is gaining traction with its new Buy Now Pay Later (BNPL) product.

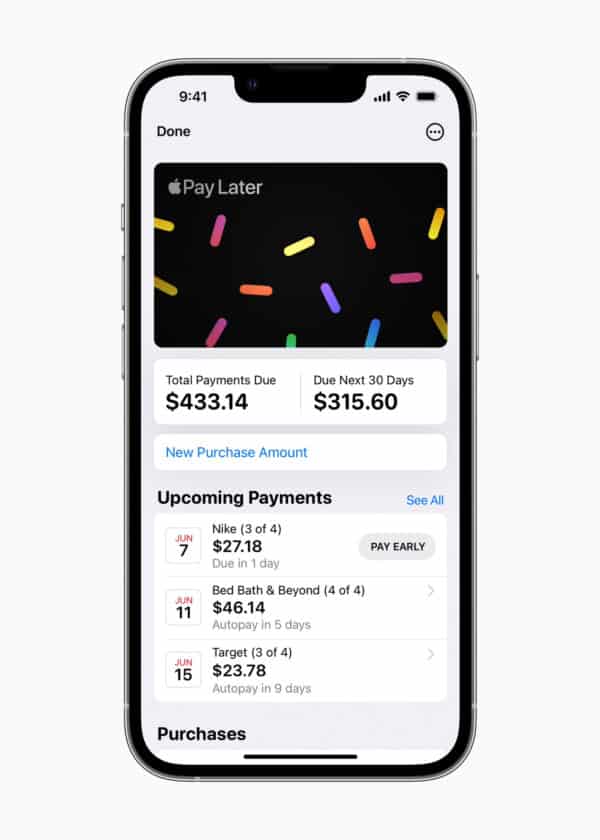

Released this past March but announced months prior, Apple says that Apple Pay Later wants to support its users financial health. The credit product allows a user to segregate purchases over 6 weeks time with four payments. There are no interest payments or other fees. It is available for purchases of $50 to $1000. Offered in partnership with Goldman Sachs – the company that powers the popular Apple Card.

According to research by JD Power, Apple Pay Later has been used by more individuals than BNPL providers like Sezzle and Zip since its launch.

To quote the report:

“Nearly one-fifth (19%) of BNPL customers used Apple Pay Later in its first three months. PayPal was still the most-used BNPL brand over the same period (39%), with Afterpay (33%) as the next-most used brand.

The average Apple Pay Later user tended to be more financially healthy than most other BNPL customers, potentially giving it a more sustainable user base than its competitors. That said, Apple did attract a higher percentage of overextended users vs. other brands in its early days, which may have resulted from existing BNPL users’ willingness to try a new payment option from what they consider a trusted brand.”

Apple Pay Later is scaling quickly because it is available anywhere Apple Pay is accepted – so everywhere.

Apple has been inching into the Fintech space for years. The company is well-known for taking its time, eschewing a first-mover advantage to get it right and then trounce its competitors.

It has been reported that Apple will also offer a longer-term credit product that may charge an interest rate. This makes a lot of sense.

Apple already has a savings product that is pretty much idiot-proof. While not the highest interest rate paid in the market – it is far higher (at 4.15%) than the majority of established banks. If you have an Apple Card, you can set it up so that your cashback money (1 to 3%) gets deposited into your savings. As well you can deposit money from any connected bank account. Takes mere seconds.

Apple should be viewed as a top Neobank – providing bank services without a banking charter. But it is not much of a leap for Apple to gain a bank charter – especially if banking partner Goldman Sachs – Marcus decides to get out of the business.

So what’s next? How about Apple Investments for securities trading? Apple Insurance? One area where Apple consistently tops everyone is customer service – an area where legacy banks fall rather short. The financial world is the limit for Apple.