The debt train keeps on running.

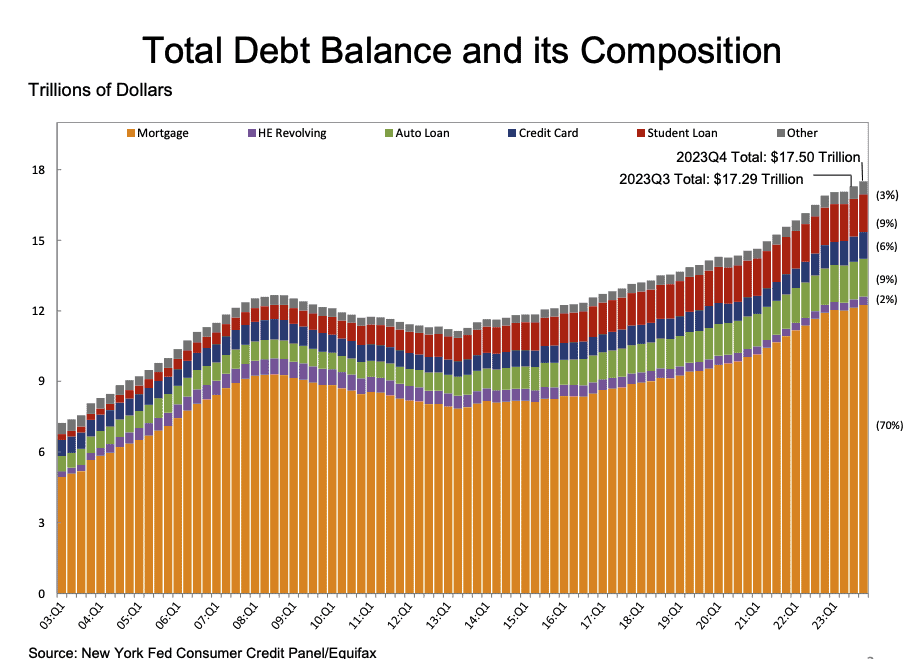

A New York Fed report published today shares that total household debt has now topped $17.5 trillion as of Q4 2023. If you compare it to the same quarter in 2022, when total debt stood at $16.9 trillion, this means in the past year, debt has risen by $600 billion.

Credit card debt during Q4 2023 registered $1.13 trillion compared to $990 billion in Q4 2022.

Wilbert van der Klaauw, economic research advisor at the New York Fed, shares that credit card and auto loan debt transitioning into delinquency is still rising about pre-pandemic levels.

“This signals increased financial stress, especially among younger and lower-income households.”

The Fed report shares:

- Mortgage balances rose by $112 billion from the previous quarter and stood at $12.25 trillion at the end of December.

- Balances on home equity lines of credit (HELOC) increased by $11 billion, the seventh consecutive quarterly increase after Q1 2022, and now stand at $360 billion.

- Credit card balances increased by $50 billion to $1.13 trillion.

- Auto loan balances rose by $12 billion, continuing the upward trajectory seen since 2020, and now stand at $1.61 trillion.

Of course, it does not help that inflation has remained sticky, albeit showing some signs of slowing in recent months. Still, prices tend to rise less quickly – not reverse the increases. This can lead to shrinkflation – less for more – or higher prices. At the same time, the Biden administration has shown an incredible lack of understanding regarding economic reality – spending money like a drunken sailor – which fuels inflation – and then chastising merchants for raising prices – something they need to do to stay in business. Perhaps the silver lining is that employment remains pretty strong which leads some to predict a soft landing – or just a bumpy one.

While Americans love to borrow and spend, they follow a prominent example: the US Federal government, which shoulders more than $34 trillion in debt. You get the government you elect.