It was bittersweet walking into Commissioner Daniel Gallagher’s office for the first and last time. He has been a true champion for small business and access to capital and we all owe him a debt of gratitude. It was also wholly appropriate that the amazing infographic that he and his staff put together demarking all the regulations governing the operation of a financial services company in the US sat poster size immediately to his left. Despite the list of very specific regulatory questions I had intended to ask him, I took a different tack and decided to focus more on a retrospective and the personal experience of Commissioner Gallagher. What he shared with his usual ease and candor was both informative and instructive.

When asked what he is proud of accomplishing while in office, he noted that much of what he is proud of cannot really be talked about as it was behind the scenes maneuvering that was not obvious, such as avoiding disasters and things for which he cannot take credit. He did take pride in setting the record for the number of dissents during rulemaking votes at 16 but noted that Commissioner Piwowar is hot on his tail.

Fighting the Good Fight for Efficient Markets & SMEs

One thing he is proud of is elevating the voice of the small business community in America. He used his capital formation listening tour to really tap into the needs and concerns of small business owners and entrepreneurs. As we all know, one of the big problems small business owners face is that they are busy running their companies and don’t have the time or resources to run to Washington and lobby rule-makers the way larger establishments do. Commissioner Gallagher went to them. It is important to remember that this initiative was done in the wake of Dodd-Frank, which provided a double blow to entrepreneurs, in not only squelching capital flows, but also diverting the SEC’s attention to its required rule-makings from other potentially beneficial initiatives.

One thing he is proud of is elevating the voice of the small business community in America. He used his capital formation listening tour to really tap into the needs and concerns of small business owners and entrepreneurs. As we all know, one of the big problems small business owners face is that they are busy running their companies and don’t have the time or resources to run to Washington and lobby rule-makers the way larger establishments do. Commissioner Gallagher went to them. It is important to remember that this initiative was done in the wake of Dodd-Frank, which provided a double blow to entrepreneurs, in not only squelching capital flows, but also diverting the SEC’s attention to its required rule-makings from other potentially beneficial initiatives.

Another point of pride is the passage of Regulation A “+” especially Tier II which included state review preemption. Once a secondary market is established, he believes it will be truly transformative. Also, the proxy advisor rules were a big win. Gallagher confided that he basically used all of his political firepower and chits on those regulations and therefore, could not push other issues.

Dodd-Frank, of course, remains a sore spot for the Commissioner. The hasty legislation passed as a reaction to the financial crisis has rippled through the economy with chilling effects. Much of the bill simply left rulemaking up to administrative agencies such as the SEC. Five years after being signed into law the rulemaking and deciphering continues. Dodd-Frank basically high-jacked the itinerary of the SEC forcing its staffers to focus on drafting its regulations rather than any of the work slated by the SEC. But this also led to one of Commissioner Gallagher’s greatest contributions, which was bringing attention to the working agenda of the SEC. Before he spoke publicly on what the SEC was spending its time and resources on, we all assumed it was working toward its twin aims of efficient markets and investor protection. By turning the spotlight around and highlighting what the SEC was really up to, it allowed the public to scrutinize and comment on the merits of such activities. As it turned out, there were a lot of things on the SEC’s plate that arguably did not serve its statutory purpose.

As for regrets, spending 25% of his time on Dodd-Frank and special interest nonsense such as conflict minerals, extraction disclosure, proxy access, say on pay, pay ratio, etc., instead of meaningful issues was a low point. Also, he admitted that much of what the JOBS Act codified could have been accomplished by the SEC, without the Congressional mandate. In other words, the SEC already had the authority under their administrative powers to enact much of what the JOBS Act envisioned but did not do so. They just did not have the political willpower (or perhaps endurance) to do it.

As for regrets, spending 25% of his time on Dodd-Frank and special interest nonsense such as conflict minerals, extraction disclosure, proxy access, say on pay, pay ratio, etc., instead of meaningful issues was a low point. Also, he admitted that much of what the JOBS Act codified could have been accomplished by the SEC, without the Congressional mandate. In other words, the SEC already had the authority under their administrative powers to enact much of what the JOBS Act envisioned but did not do so. They just did not have the political willpower (or perhaps endurance) to do it.

When asked about Title III crowdfunding, Commissioner Gallagher said “it’s going to happen” and noted that no one on the commission is actually opposed to it. He said the initial legislation of the JOBS Act was so bad the SEC did not have a lot to work with. There was an internal debate at the SEC as to whether or not to wait for a congressional rework or just implement the proposed regulations. He feels the SEC is at a juncture where it can no longer wait for a Congressional “white knight” and will have to implement the proposed regulations (with some much needed modifications), although they are obviously flawed (audit requirement, etc.). But I am personally happy for this outcome. We, as an industry, just need a path—there are so many smart people working in the space, we will figure it out. We can get over, under or around the hurdles, just get the regs out and we’ll take it from there. I would love to see a Congressional fix, but to quote an article from last week, “sometimes you just have to f&*$%n’ start.”

When asked about the North American Securities Administrators Association or NASAA, Commissioner Gallagher responded that it was a vexing issue for him. In general, as a libertarian at heart, he would prefer smaller government, which often means leaving certain regulations up to state governments. Unfortunately, due to the need for interstate market efficiency, a state-by-state regulatory regime is simply inefficient. He feels NASAA should be working with the SEC instead of against it in promoting efficiencies instead of inserting itself in the process and seeking merit review. Commissioner Gallagher pointed out that one of the beauties of the federal securities regime (and one of the reasons I went into securities law) is that it is NOT a merit review process. Instead, we use a disclosure regime, which allows people to make the determination as to whether or not a security is worth investment, rather than the Federal, or in this case, state government. As long as adequate

When asked about the North American Securities Administrators Association or NASAA, Commissioner Gallagher responded that it was a vexing issue for him. In general, as a libertarian at heart, he would prefer smaller government, which often means leaving certain regulations up to state governments. Unfortunately, due to the need for interstate market efficiency, a state-by-state regulatory regime is simply inefficient. He feels NASAA should be working with the SEC instead of against it in promoting efficiencies instead of inserting itself in the process and seeking merit review. Commissioner Gallagher pointed out that one of the beauties of the federal securities regime (and one of the reasons I went into securities law) is that it is NOT a merit review process. Instead, we use a disclosure regime, which allows people to make the determination as to whether or not a security is worth investment, rather than the Federal, or in this case, state government. As long as adequate  disclosure is provided to facilitate an informed investment decision, individuals are free to succeed or fail – as they should be. Commissioner Gallagher lamented for a symbiotic relationship with NASSA, as he has utmost respect for the state regulators who are often overworked and lack resources, but noted the need for realistic procedures given the state of modern markets.

disclosure is provided to facilitate an informed investment decision, individuals are free to succeed or fail – as they should be. Commissioner Gallagher lamented for a symbiotic relationship with NASSA, as he has utmost respect for the state regulators who are often overworked and lack resources, but noted the need for realistic procedures given the state of modern markets.

Don’t Be Bullied

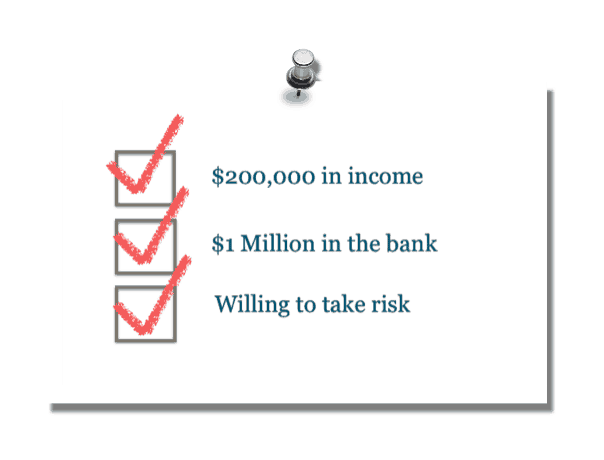

When asked what was next for him, he gave the expected “I don’t know” response. He explained that due to ethics rules and recusal policies, he was not interested in talking to anyone until he had officially left the office. He noted that soon thereafter he would be looking for gainful employment, as he is not independently wealthy. And then I uncovered an amazing fact – SEC Commissioner Gallagher is BARELY an accredited investor by the current standard – and was not accredited during much of his tenure at the SEC. Based on the base salary of a commissioner, he is not, and only just crossing the threshold with the combination of other assets is one of the primary regulators of the free market able to meet the wealth criteria to invest in it. It is a good thing that some policy-makers want to raise those thresholds, so we can protect borderline individuals like an SEC Commissioner from themselves.

What’s Next?

Back to the future, he dispelled the notion that he has plans to start, join or work with or for a venture exchange. He does want to spend more time with his family and to stay in the policy space. After leaving the SEC the first time and going back to working at a law firm, he was not able to speak out on issues, which needs to be a feature of his next endeavor.

Back to the future, he dispelled the notion that he has plans to start, join or work with or for a venture exchange. He does want to spend more time with his family and to stay in the policy space. After leaving the SEC the first time and going back to working at a law firm, he was not able to speak out on issues, which needs to be a feature of his next endeavor.

Venture Markets

On the topic of venture exchanges, when I noted that it may not be in the best interest of a small business to have its securities publicly quoted, as it causes another area of distraction when trying to actually operate a business, Commissioner Gallagher said that distraction would be present regardless, and at least having the securities on an exchange with rational price formation and inherent liquidity, as opposed to the current OTC, would be a net positive. He went on to explain that the exchange doesn’t need to allow for continuous trading, and gave an example of auctions held three times a day – this would also alleviate any high-frequency trading. He also noted that all other features of the exchange could be conducive to small business. The JOBS Act and specifically Regulation A did not factor in the relationship between the issuance of security (which is what the regs were focused on) and the liquidity needs of investors for an established secondary market. The two are fundamentally linked and are manifested in the price an issuer is able to get for its securities. Other benefits of the secondary markets are the embedded investor protections of price discovery and market surveillance.

Importantly Commissioner Gallagher noted that none of these passion issues should be partisan issues and it is crazy that support cannot be found on both sides of the aisle. Supporting small business access to capital simply makes sense and benefits us all. He blames the heavy lobbying by brokerage firms and other industries or “folks that don’t like innovation because they make too much money in the darkness.”

Importantly Commissioner Gallagher noted that none of these passion issues should be partisan issues and it is crazy that support cannot be found on both sides of the aisle. Supporting small business access to capital simply makes sense and benefits us all. He blames the heavy lobbying by brokerage firms and other industries or “folks that don’t like innovation because they make too much money in the darkness.”

On the subject of “one world regulation,” he noted that it is “not very American, to state the obvious.” He continued that “our markets are better and deeper” and we should have higher expectations for our economy. We should not be modeling our economy after Europe, but should strive to have the best economy in the world. Of course, we should cooperate with other governments, share information and conduct joint enforcement, but global laws are inefficient and dangerous and can lead to  global failure. All we need to do is look to the Basel banking regulations, which required the holding of mortgage-backed securities as a safe asset class to see an example of that. If we want to look abroad for regulatory examples, Commissioner Gallagher suggests looking to emerging markets such as the Middle East, Asia and South America where they are creating incubators of capitalism.

global failure. All we need to do is look to the Basel banking regulations, which required the holding of mortgage-backed securities as a safe asset class to see an example of that. If we want to look abroad for regulatory examples, Commissioner Gallagher suggests looking to emerging markets such as the Middle East, Asia and South America where they are creating incubators of capitalism.

In finishing up our meeting, I asked the Commissioner for one piece of advice he would give his successor, after thought, he earnestly remarked that you have got to have a thick skin. You probably will not know until you get into a job like this, but you will suffer a lot of slings and arrows. It is essential to stay positive and take comfort that you are doing the right thing.

To Commissioner Gallagher: we thank you for your thick skin.

Georgia P. Quinn is the CEO and co-founder of iDisclose, an adaptive web-based application that enables entrepreneurs to prepare customized institutional grade private placement documents for a fraction of the time and cost. Heralded by Thomson-Reuters as a Top Female Attorney in New York City, she also serves as of counsel at the leading firm in crowdfunding, Ellenoff, Grossman & Schole, specializing in facilitating financial transactions and compliance with JOBS Act regulations. A foremost expert in corporate finance, she has worked on over $1 billion in business transactions over the course of her legal career. Prior to founding iDisclose, Georgia represented several Fortune 500 companies in financings for six years at Weil, Gotshal & Manges, one of the top ten law firms in the world, and then for over two years at Seyfarth Shaw, a leader in legal technology. As a globally recognized thought leader in the crowdfunding space, she has been a featured speaker at multiple conferences and has presented to such authorities as the Securities and Exchange Commission (SEC) and the American Bar Association (ABA).

Georgia P. Quinn is the CEO and co-founder of iDisclose, an adaptive web-based application that enables entrepreneurs to prepare customized institutional grade private placement documents for a fraction of the time and cost. Heralded by Thomson-Reuters as a Top Female Attorney in New York City, she also serves as of counsel at the leading firm in crowdfunding, Ellenoff, Grossman & Schole, specializing in facilitating financial transactions and compliance with JOBS Act regulations. A foremost expert in corporate finance, she has worked on over $1 billion in business transactions over the course of her legal career. Prior to founding iDisclose, Georgia represented several Fortune 500 companies in financings for six years at Weil, Gotshal & Manges, one of the top ten law firms in the world, and then for over two years at Seyfarth Shaw, a leader in legal technology. As a globally recognized thought leader in the crowdfunding space, she has been a featured speaker at multiple conferences and has presented to such authorities as the Securities and Exchange Commission (SEC) and the American Bar Association (ABA).