In my last article on Crowdfund Insider, entitled: “JOBS Act Crowdfunding Begins on May 16, 2016: Don’t Get Busted for Solicitation!,” I warned of one of the hidden dangers for companies embarking on a Title III equity crowdfunding campaign – which goes live on May 16. In particular, I highlighted the limited ability of an issuer to engage in advertising its offering, courtesy of the JOBS Act.

In particular, Congress, in its wisdom, departed dramatically from the House version of this legislation, prohibiting all advertising in connection with Title III offerings unless this advertising took place on the SEC registered portal hosting the campaign. Hence, a limited ability for issuers to leverage social media of the portal. The SEC, in its Final Rules, provided a modest workaround: issuers could circulate an “off portal” notice with limited information – including a brief description of the business and the terms of the offering, albeit with a link to the crowdfunding portal. But that was all she wrote.

In particular, Congress, in its wisdom, departed dramatically from the House version of this legislation, prohibiting all advertising in connection with Title III offerings unless this advertising took place on the SEC registered portal hosting the campaign. Hence, a limited ability for issuers to leverage social media of the portal. The SEC, in its Final Rules, provided a modest workaround: issuers could circulate an “off portal” notice with limited information – including a brief description of the business and the terms of the offering, albeit with a link to the crowdfunding portal. But that was all she wrote.

To make matters more complicated, in the Final Rules Release the SEC cautioned issuers about engaging in pre-offering advertising or solicitation under other long standing SEC rules. Yes, a company could continue to engage in regular business communications in the ordinary course immediately prior to the campaign launch, but with no mention of an offering. And if the issuer had no prior history of engaging in regular business communications, even these types of communications in close proximity before the formal portal launch of a crowdfunding campaign could spell trouble for the issuer.

To make matters more complicated, in the Final Rules Release the SEC cautioned issuers about engaging in pre-offering advertising or solicitation under other long standing SEC rules. Yes, a company could continue to engage in regular business communications in the ordinary course immediately prior to the campaign launch, but with no mention of an offering. And if the issuer had no prior history of engaging in regular business communications, even these types of communications in close proximity before the formal portal launch of a crowdfunding campaign could spell trouble for the issuer.

As might have been expected, those folks immersed in the rewards-based crowdfunding regime were somewhat taken aback by these revelations. “Say it ain’t so,” some said. Others: that makes no sense. Well, it is so, and yes, it makes no sense!

It’s Time for these Solicitation Rules to Go Into Rehab

It’s Time for these Solicitation Rules to Go Into Rehab

I am loathe to simply call out obstacles in the path of capital formation for SME’s without offering solutions. Fortunately, many of my colleagues as well as would be Title III portals have been on this issue from the get go. In the age of the Internet and social media, these are useful and inexpensive means of communication which ought to be afforded to the smallest of companies on a shoe string budget. In fact, in an area where the SEC’s hands were not tied down by the JOBS Act, Regulation A+, solicitation and advertising of offerings at any time before an offering formally launches are not only allowed – but specifically protected by the JOBS Act itself.

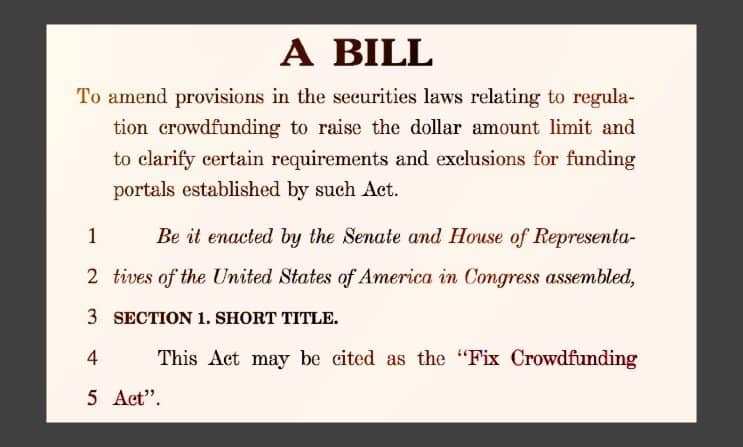

There are now tangible signs that a legislative fix is in the works, courtesy of, once again, equity crowdfunding champion Congressman Patrick McHenry. Without a great deal of fanfare, Congressman McHenry introduced a new bill into the House of Representatives, entitled the “Fix Crowdfunding Act.” It is limited in scope, and deliberately so, as there remain a number of crowdfunding skeptics in Congress, and some of those who went along to get along back in 2012 have come down with a case of buyer’s remorse. And lest we not forget, the armies of consumer lobbyists, etcetera who have continued to frequent the halls of Congress for the past four years.

Most significantly, the new bill raises the annual crowdfunding ceiling from $1 million to $5 million, clarifies the scope of a portal’s liability, allows crowdfunders to invest in large groups through specially formed entities (commonly referred to as “SPVs”), and last, but not least, allows companies exploring the use of equity crowdfunding to “test the waters” through public solicitation and advertising before a campaign formally begins – to both generate and measure interest in a prospective crowdfunding campaign.

Most significantly, the new bill raises the annual crowdfunding ceiling from $1 million to $5 million, clarifies the scope of a portal’s liability, allows crowdfunders to invest in large groups through specially formed entities (commonly referred to as “SPVs”), and last, but not least, allows companies exploring the use of equity crowdfunding to “test the waters” through public solicitation and advertising before a campaign formally begins – to both generate and measure interest in a prospective crowdfunding campaign.

The bill makes its debut on April 14 in the Capital Markets Subcommittee of the House Financial Services Committee along with three other bills geared to remove various obstacles in the path of SME capital formation. I expect that because of HR 4855’s strategically narrow focus it will be well received in Committee on a bi-partisan basis. From there it would move to the House for a floor vote later this year, and hopefully find a willing partner on the Senate side, something that has often proved elusive, indeed fatal, for SME legislation.

And Here Comes the Micro Offering Safe Harbor Act

Another of the four bills expected to be introduced at the April 14 Subcommittee meeting is HR 4850, the Micro Offering Safe Harbor Act, introduced by Congressman Tom Emmer last month. At the heart of this bill is a provision which allows companies to raise up to $500,000 in a 12 month period, free of state “blue sky” regulation, and with none of the bells and whistles which currently populate Title III crowdfunding. This idea was first floated by David Burton, Senior Fellow at The Heritage Foundation, and cited by former SEC Commissioner Dan Gallagher in a public speech back in March 2015. Though not touted as a crowdfunding bill, this proposed legislation could be the nucleus for the fix that startups have been (and will be) looking for, a kinder, gentler crowdfunding regime for the smallest of companies – circumventing the much criticized complexities of Title III crowdfunding. And in my opinion, this is a fix which is much needed – in effect, a “demilitarized zone”, where startups and small companies can raise money without the costs and complexities that frequently makes SME fundraising a nightmare.

Another of the four bills expected to be introduced at the April 14 Subcommittee meeting is HR 4850, the Micro Offering Safe Harbor Act, introduced by Congressman Tom Emmer last month. At the heart of this bill is a provision which allows companies to raise up to $500,000 in a 12 month period, free of state “blue sky” regulation, and with none of the bells and whistles which currently populate Title III crowdfunding. This idea was first floated by David Burton, Senior Fellow at The Heritage Foundation, and cited by former SEC Commissioner Dan Gallagher in a public speech back in March 2015. Though not touted as a crowdfunding bill, this proposed legislation could be the nucleus for the fix that startups have been (and will be) looking for, a kinder, gentler crowdfunding regime for the smallest of companies – circumventing the much criticized complexities of Title III crowdfunding. And in my opinion, this is a fix which is much needed – in effect, a “demilitarized zone”, where startups and small companies can raise money without the costs and complexities that frequently makes SME fundraising a nightmare.

Congressman Emmer recently shared his views with me on what is behind his legislative proposal, reflecting a keen understanding of what his constituents need and want in order to get ahead:

“The fact is that it is very expensive to start a new business. By maximizing the amount of money small businesses can raise, this legislation will allow for more businesses to open, more jobs to be created, more people to be lifted out of poverty, and more Americans to fully realize their dreams.”

So you say, what about investor protection? Well, no market will function for long without some form of investor protection. The solution of first resort here are the existing anti-fraud provisions of federal and state securities laws: if a company makes a statement which it knows is false, or omits information required to make its statement not misleading – it can and will get busted by federal and state regulators, and an investor has a legal claim to get his or her money back.

So you say, what about investor protection? Well, no market will function for long without some form of investor protection. The solution of first resort here are the existing anti-fraud provisions of federal and state securities laws: if a company makes a statement which it knows is false, or omits information required to make its statement not misleading – it can and will get busted by federal and state regulators, and an investor has a legal claim to get his or her money back.

I expect that this bill will generate a number of friendly and not so friendly amendments before it is voted out of the House Financial Services Committee, particularly in view of the broad state blue sky exemption. Hopefully what emerges will be a useful, and long overdue, solution for capital raising for our country’s smallest of job creators. And, if done right, this could be just the ticket for jumpstarting equity crowdfunding at the lowest end of the SME capital formation food chain.

And what ever happened to that champion of small business who once occupied a Commissioner’s seat at the SEC, Dan Gallagher? Well, it seems he is sending his new boss, Paul Atkins, CEO of Patomak Global Partners, to testify before the Capital Markets Subcommittee on April 14.

Kudos to Congressmen McHenry and Emmer, their dedicated Staff, and the modest, but staunch advocate of SME’s, Commissioner Dan Gallagher. Good Luck this Week! This ought not to be a partisan issue. To borrow a phrase: It’s the economy, stupid! And our country’s economic future is depending on it.

Samuel S. Guzik, a Senior Contributor to Crowdfund Insider, is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience in private practice. Guzik is also former President and Board Chair of the Crowdfunding Professional Association (CFPA). A nationally recognized authority on the JOBS Act, including Regulation D private placements, investment crowdfunding and Regulation A+, he is and an advisor to legislators, researchers and private businesses, including crowdfunding issuers, service providers and platforms, on matters relating to the JOBS Act. As an advocate for small and medium sized business he has engaged with major stakeholders in the ongoing post-JOBS Act reform, including legislators, industry advocates and federal and state securities regulators. In 2014, some of his speaking engagements have included leading a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy, a panelist at the MIT Sloan School of Business 2014 Crowdfunding Roundtable, and a panelist at a national bar association event which included private practitioners, investor advocates and officials of NASAA. His articles on JOBS Act issues, including two published in the Harvard Law School Forum on Corporate Governance and Financial Regulation, have also served as a basis for post-JOBS Act proposed legislation.

Samuel S. Guzik, a Senior Contributor to Crowdfund Insider, is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience in private practice. Guzik is also former President and Board Chair of the Crowdfunding Professional Association (CFPA). A nationally recognized authority on the JOBS Act, including Regulation D private placements, investment crowdfunding and Regulation A+, he is and an advisor to legislators, researchers and private businesses, including crowdfunding issuers, service providers and platforms, on matters relating to the JOBS Act. As an advocate for small and medium sized business he has engaged with major stakeholders in the ongoing post-JOBS Act reform, including legislators, industry advocates and federal and state securities regulators. In 2014, some of his speaking engagements have included leading a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy, a panelist at the MIT Sloan School of Business 2014 Crowdfunding Roundtable, and a panelist at a national bar association event which included private practitioners, investor advocates and officials of NASAA. His articles on JOBS Act issues, including two published in the Harvard Law School Forum on Corporate Governance and Financial Regulation, have also served as a basis for post-JOBS Act proposed legislation.