Lendix, the lending marketplace that recently become number 1 in SME marketplace lending in France, announced that it has acquired crowdlending platform Finsquare. This first instance of consolidation in the French market certainly is not the last. This acquisition illustrates four trends and issues in crowdfunding and alternative finance at large that are of relevance well beyond the French market.

Crowdfunding is Too Crowded on the Offer Side

A consolidation in the French market does not come as a surprise. The French market numbers no less than 74 firms officially registered as “Intermédiaire en Financement Participatif (IFP)”, the legal status of accredited crowdlenders. After favorable regulations were issued in October 2014, many entrepreneurs rushed to join the crowdfunding fray, most of them with the intention to launch a crowdlending platform targeting small and medium enterprises (SME) as borrowers.

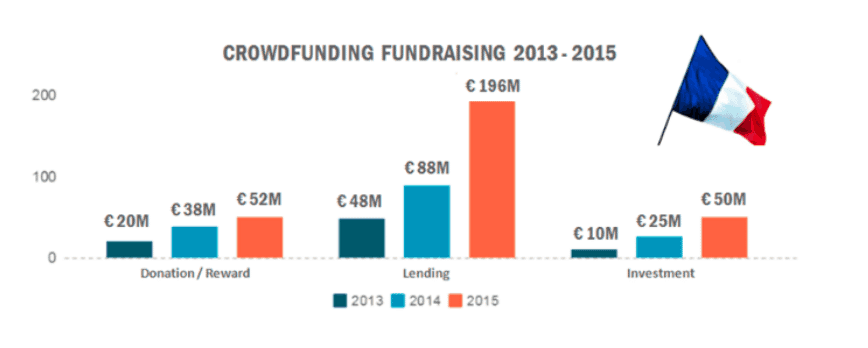

Since then, the French crowdlending market has grown at a nice 100+% per annum. But the bulk of the $198 funding raised by crowdlending in 2015 went to P2P lending by Prêt d’Union. The remaining SME crowdlending volume is not sufficient to sustain the influx of new platforms.

Quite a few platforms have given up before becoming active, and around 10 gave up their license. The market remains almost exclusively concentrated on fewer than 10 players: Lendix, Unilend, Lendopolis, (formerly) Finsquare, Lendosphere, Credit.fr, Prexem, Bolden and PretUp. Even for those, building a critical mass of business is far from easy.

French SMEs, especially the performing ones that have a good relationship with their bank, remain largely unaware of or oblivious to the financing opportunities presented by crowdfunding. The crowdfunding market may be crowded on the offer side, but it still is immature on the demand side. Much evangelization is still needed.

We can safely assume that the situation is similar in other Continental European markets such as Germany, Italy and Spain. National and international consolidation looms.

Alternative Finance is Run by Experienced Bankers

The contrast between the management of the acquiring firm Lendix and that of the acquired firm Finsquare also gives much food for thought about the evolution of crowdfunding.

The contrast between the management of the acquiring firm Lendix and that of the acquired firm Finsquare also gives much food for thought about the evolution of crowdfunding.

Launched hardly two years ago, Finsquare was a crowdlending platform specialized in short-term loans to SMEs, with a term of under 18 months. The company’s founder and managers Polexandre Joly and Adrien Wiart are two talented executives with solid experience in eCommerce, marketing, sales and strategy, but not originally specialized in finance. Finsquare cultivated a lively style of communication that attracted a small but vibrant community of 3,500 retail investors. Not enough, though, to convince their own investors to further fund the platform’s growth. The platform was running out of cash. The founders decided to give up and refocus on a somewhat more classical, marketing and sales-oriented loan broker business GoCreditPro.

Lendix, by contrast, was founded and is now managed by veterans of the finance world with decades of experience in multiple areas of finance including venture capital and private equity (Olivier Goy, founder and CEO), trading and investment banking (Patrick de Nonneville, COO) and retail banking (Pascal Ouvrard, Bus. Dev.).

This level of financial expertise, when combined with Web and alternative finance knowhow, creates a serious barrier to entry for newcomers. Hopefully, it won’t stifle innovation.

Institutional Investors Dominate Retail Investors

In their announcement of the acquisition, Lendix and Finsquare stressed the complementarity of their firms’ offerings: Lendix focuses on mid-term loans of an average term of 40 months while Finsquare was targeting short-term loans. However, Finsquare retail investors will experience more changes than loan maturity after the acquisition of the platform by Lendix.

Finsquare was geared for the active participation of retail investors who, among other interactions, were collectively determining the interest rate of SME loans through an online bidding process of reverse auction.

Finsquare was geared for the active participation of retail investors who, among other interactions, were collectively determining the interest rate of SME loans through an online bidding process of reverse auction.

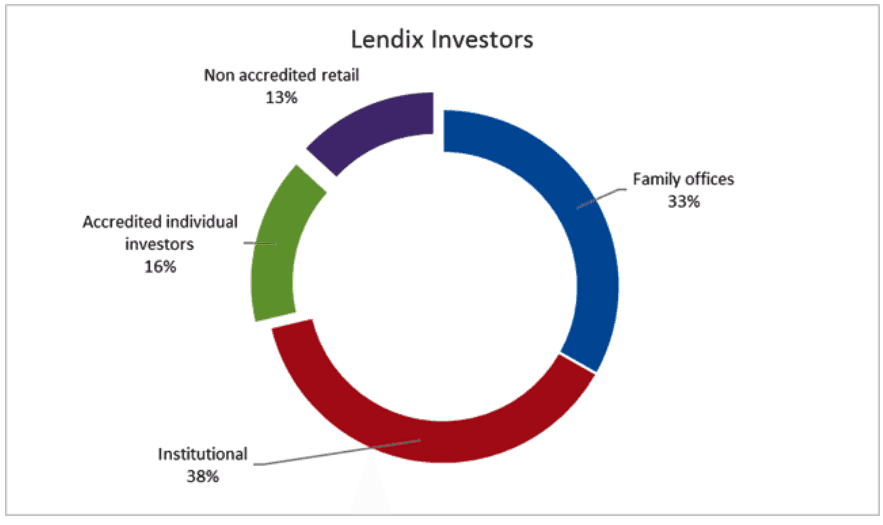

Lendix, by contrast, has built its rapid success on designing a marketplace suited to meet the needs of institutional investors, family offices and accredited investors. The crowd plays no role in vetting SME candidates or in setting the loan’s interest rate. Neither the bidding nor the “all or nothing” rule apply. The SMEs selected and scored by Lendix analysts are guaranteed to receive 100% of the loan they requested. Institutional investors (in the loose sense of the phrase, i.e. including family offices and other non-retail investors) will fund the first 51% of every loan vetted, as well as whatever remains to be financed after the project has been funded by retail investors on the platform.

As a result, non-accredited retail investors represent only 13% of the nearly €19 million raised by Lendix to date. Individual accredited investors account for 16%, family offices and institutional investors make up the remainder.

One could argue that there is very little “crowd” in this type of marketplace lending. But one should also bear in mind that the crowd of retail investors often perceives it as an advantage to co-invest with institutional investors, to have direct access to their resources and investment strategies, and this with minimal effort.

The notion of crowdfunding has become quite elastic. But semantic discussions and casuistry that seek to define clear boundaries between was is and is not crowdfunding will struggle to live up to the fast-changing pace in the field. Realities are blurred. Crowdfunding platforms cannot anymore dispense of institutional investor support to thrive. Crowdlenders that reach a sufficient volume of business do meet retail investors’ demands by offering automated allocation features that make them look more like funds.

Not Every Cessation of Operation Will Have a White Knight

One of the major concerns of regulators and industry players alike is the issue of the continuity of client account management in case of a platform’s failure. The last thing the emerging crowdfunding sector needs is, of course, a group of frustrated lenders and angry borrowers protesting because they’ve been left stranded after a platform has stopped operating.

One of the major concerns of regulators and industry players alike is the issue of the continuity of client account management in case of a platform’s failure. The last thing the emerging crowdfunding sector needs is, of course, a group of frustrated lenders and angry borrowers protesting because they’ve been left stranded after a platform has stopped operating.

For that reason, the French crowdfunding regulation requires a very strict segregation between the clients’ payment accounts and the platform’s own accounts and it foresees a run-off management process in case of a platform shutdown.

In theory, the regulator expects the independent payment services provider – in the case of Finsquare, LemonWay – to ensure the continuity of loan servicing. However, the exact terms under which the non-negligible cost and liability of loan servicing should be transferred are, to my knowledge, still unclear. Finsquare, as a first sizeable example of an active platform with €4 million worth of cumulated loans wanting to get out of business, has not put the run-off management process to the test because Lendix appeared as a providential white knight.

Lendix has acquired all Finsquare’s assets and is transitioning all accounts onto its own systems. It expects to complete the process within 3 to 5 weeks, in due time for Finsquare’s lenders to file their taxes.

We cannot expect every further consolidation to have a white knight. Yet we would like them to happen smoothly. The topic should clearly be on top of every regulator’s and industry association’s agenda.

Therese Torris is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique.

Therese Torris is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique.