Bitbond is one of the most interesting SME lenders around today. Launched in 2013, the online lender eschewed dollars and euros to focus on digital currencies, specifically Bitcoin.

The global peer to peer lender provides access to capital for small business around the world. As many parts of the globe are under-banked, Bitbond can provide a valuable credit option matching lower rates to SMEs in need of growth capital. In the overall scheme of things, Bitbond is small having facilitated just over $870,000 for 1500+ loans. But the platform is growing rapidly (65% month over month) filling a vacuum in the credit market.

The global peer to peer lender provides access to capital for small business around the world. As many parts of the globe are under-banked, Bitbond can provide a valuable credit option matching lower rates to SMEs in need of growth capital. In the overall scheme of things, Bitbond is small having facilitated just over $870,000 for 1500+ loans. But the platform is growing rapidly (65% month over month) filling a vacuum in the credit market.

Founded by former banker and consultant Radoslav Albrecht, Bitbond became the first regulated Bitcoin P2P Lender in Germany receiving approval from BaFin – thus validating its operations. Albrecht has set the bar high for his company as he envisions Bitbond becoming a key player in the global small business lending sector – all without the help of a bank.

Crowdfund Insider recently corresponded with Albrecht to learn more about what drives Bitbond’s success.

Crowdfund Insider: How did you decide to launch a Digital Currency P2P lending platform?

Radoslav Albrecht: In 2013 I started bootstrapping Bitbond – the world’s first global peer-to-peer lending platform for small business loans. As a former investment banker in London and later management consultant, I had seen the inefficiencies of the banking system first hand, and set my mind on creating a better alternative.

Radoslav Albrecht: In 2013 I started bootstrapping Bitbond – the world’s first global peer-to-peer lending platform for small business loans. As a former investment banker in London and later management consultant, I had seen the inefficiencies of the banking system first hand, and set my mind on creating a better alternative.

Bitcoin was launched in 2009 and by 2013 it had proven its durability and offered many potential benefits over conventional currencies and payment networks. Most importantly, bitcoin allowed for global transactions to take place cheaply and efficiently, while operating completely independently of the banking system. For lenders, this means that they now have the opportunity to invest in an international fixed income asset class with an expected return of 13% per year. Borrowers on the other hand, get access to working capital at affordable rates, and can grow their business.

Additionally, anyone with an internet connection can use Bitcoin, which makes it a great tool for financial inclusion, potentially bringing in the 2 billion adults who do not have access to a bank account.

Today, I think we are on a really good way to establishing Bitcoin peer to peer lending as an attractive alternative for borrowers and lenders around the world. We now have 6 full-time employees and help fund loans of over $100,000 a month.

![]()

![]() Crowdfund Insider: Congratulations on the BaFin (German Federal Financial Supervisory Authority) license. What were the regulatory challenges to setting this up?

Crowdfund Insider: Congratulations on the BaFin (German Federal Financial Supervisory Authority) license. What were the regulatory challenges to setting this up?

Radoslav Albrecht: Thank you! Getting the BaFin licence is a huge step for us. It provides regulatory clarity for our users and investors. It also shows that it is possible to get regulatory approval for Bitcoin based business models. We’ve seen a great response from the peer-to-peer community since the news broke.

Getting the licence was a comprehensive process and BaFin checked numerous aspects of our platform. We have been in contact with them since our launch in 2013, so the whole process took three years. At the beginning the main challenge was to explain our business model to BaFin in detail. Then they needed to find a way to apply the existing regulatory framework to our business model.

Eventually a solution was found and then the actual application for our licence began. The application covered aspects such as the technical setup of our platform, know your customer (KYC) and anti money laundering procedures, capitalization and qualification of the leadership team.

Although you might think three years is a long time, it’s worth noting that we found a way to work together with BaFin and I think it’s fair to say that both sides learned a lot throughout the process. One reason why the application took three years is down to the unprecedented nature of our business. There were no clear guidelines for a global peer to peer Bitcoin lending platform, and a lot of time was spent on creating a fair precedent. We’re proud to have helped set this precedent in Germany.

Crowdfund Insider: How has loan volume / investing volume been growing?

Radoslav Albrecht: Growth has been really encouraging and we’ve seen 65% month over month growth in October. The task now is to push on with another strong month in November, in which we aim to originate $120,000 in loan volume. Whether we achieve this or not, will depend on our ability to bring high-quality borrowers and lenders onto the platform.

Because we use Bitcoin as a payment network, Bitbond operates internationally. In terms of growth, this gives us the opportunity to draw from a vast reservoir of borrowers and lenders located anywhere in the world.

Because we use Bitcoin as a payment network, Bitbond operates internationally. In terms of growth, this gives us the opportunity to draw from a vast reservoir of borrowers and lenders located anywhere in the world.

On the flipside, our global availability results in a large number of diverse applications. This is why we’ve just rolled out our automated credit scoring, which decreases the need for manual interaction during the credit scoring process. Through automation, applicants can be assessed instantly. Not only does this reduce the time between a borrower applying and publishing a loan on Bitbond, but it also produces more accurate ratings and higher returns for investors.

By automating the credit scoring system, we are in the perfect position to scale Bitbond and significantly grow loan volume in the future. The more accurate assessments will result in lower default rates, and higher returns for investors, which should further spur on growth.

On the investor side, we are also working hard to bring more institutional investors onto the platform. This forms another important aspect of our growth strategy.

Crowdfund Insider: How do you source investors? Borrowers?

Radoslav Albrecht: Good question. Despite our alternative approach to peer to peer lending, we face similar challenges to traditional platforms like Lending Club and Prosper. The most important of which is getting the balance between high-quality borrower and lenders right on the platform.

An excess of loans on the platform means some great borrowers don’t get funded. On the other hand, too many lenders on the platform causes loans to get funded instantly, and results in a lack of investment opportunities for new users. Both eventualities can cause disenchantment with the platform.

This is why sourcing the right investors and borrowers is so important to peer to peer lending platforms. Typically, the likes of Lending Club and Prosper would mail letters to potential borrowers. Being a startup with a global audience, we can’t rely on these kinds of marketing methods and need to find new ways of attracting excellent borrowers and lenders through more innovative channels.

Working towards high rankings in Google has so far been the best way to attract new users. We do this by targeting relevant, high-intent keywords and creating high-quality content which search engine’s love. We find that searchers trust organic results more than paid ads, and the higher conversion and activation rates reflect this. The added benefit of this approach, is that it keeps our acquisition costs low.

SEO helps in the long run, but we work on more immediate marketing channels as well. Perhaps the most important here, is creating a strong relationship with the community of small business owners and independent investors.

It’s also our job to educate our audience about the possibilities of bitcoin and the benefits it brings for investors and borrowers. One worry we hear a lot for example, concerns the volatility of the bitcoin price. Many investors are intrigued by our platform, but don’t want to take on a currency risk.

It is up to us to explain that investors can pick exchange rate pegged loans on Bitbond. These are denominated in USD and don’t carry bitcoin price risk for either borrower or lender. In these cases, the US dollar is used as a base currency, so the installment values remain the same throughout the lifetime of the loan.

This is just one example of how we are trying to educate investors, and seeing great results on the platform so far.

Crowdfund Insider: Is there a typical type of borrower on Bitbond?

Radoslav Albrecht: Yes, we specialise in global small business lending. This means that most borrowers run their own business and need financing to cover a short-term liquidity gap, make a bulk purchase, or hire new staff.

Most borrowers will run some sort of online business. This might be a store on eBay, Amazon, MercadoLibre, Etsy or their own eCommerce website. These kind of sellers are particularly drawn to Bitbond for two reasons:

Most borrowers will run some sort of online business. This might be a store on eBay, Amazon, MercadoLibre, Etsy or their own eCommerce website. These kind of sellers are particularly drawn to Bitbond for two reasons:

Firstly, our credit scoring can more accurately assess their creditworthiness than traditional alternatives. This results in lower interest rates for online sellers. Secondly Bitbond is available in regions which are underserved by traditional sources of financing. As a result, we are often the best available choice to online sellers.

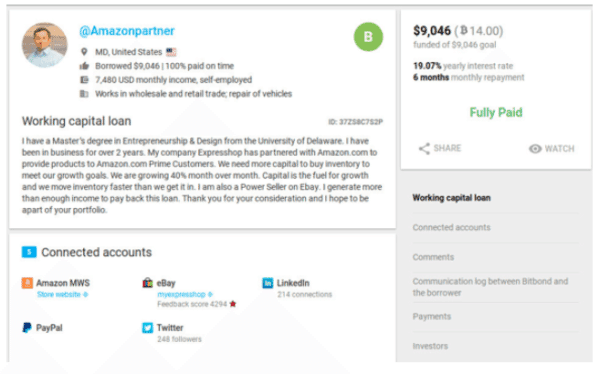

On the other hand, we specialise in online sellers because they typically offer a wealth of information not provided by retail borrowers. This helps us to accurately assess their creditworthiness, and ensures that only reputable borrowers get funded on the platform. To illustrate this point, let’s take a typical online seller from the US.

From the screenshot we can see the loan purpose along with the online accounts connected. Our credit scoring algorithm has used the vast amount of data provided by (among others) the Amazon, eBay, LinkedIn, PayPal and Twitter accounts to give this borrower a “B”. A retail borrower would not be able to provide this level of information, making a creditworthiness assessment more difficult.

Crowdfund Insider: Which countries are the main users (both investors & borrowers) of your site?

Radoslav Albrecht: We are proud to have users from over 120 countries. The bulk of our current user base is located in the US, Germany, India or the Philippines, but we are seeing meaningful traction in Brazil, Spain, the United Kingdom and Canada as well.

If we take a look at these countries we can already get an indication of how borrowers and lenders are spread across the world. Small business owners from the Philippines for example find Bitbond particularly attractive because the bitcoin ecosystem over there is strong, and access to traditional working capital is difficult.

Many Filipinos use bitcoin on a day-to-day basis, sending remittances and paying bills with it. Their affinity for bitcoin makes Bitbond a welcome alternative to banks which are restrictive and typically involve a long application process. On Bitbond they can get a loan of $10,000 at 12% per year.

Many Filipinos use bitcoin on a day-to-day basis, sending remittances and paying bills with it. Their affinity for bitcoin makes Bitbond a welcome alternative to banks which are restrictive and typically involve a long application process. On Bitbond they can get a loan of $10,000 at 12% per year.

Our affordability is also what makes us attractive to SME’s in Brazil and Venezuela, where interest rates on unsecured loans start at around 33% per year. In India, a loan from a bank commands similarly high interest rates, but here we have the added factor of banks underserving the region. Only 53% of adults in India own a bank account, giving us a clear advantage and making Bitbond very attractive for small business owners there.

Most loans on Bitbond are funded by retail and institutional investors from Germany, Northern America and the United Kingdom. The value proposition here, is that Bitbond offers access to an international fixed income asset class with an expected return of 13% per year.

For ordinary people who have seen their money eaten away by inflation, or invested at 1-2% pa, our platform offers an attractive alternative. Sophisticated investors see us as an opportunity to diversify their portfolio internationally, and more effectively spread risk.

Crowdfund Insider: What type of data are you leveraging to establish a credit score for a borrower?

Radoslav Albrecht: For security reasons I can’t share exactly what data we evaluate in order to assess borrowers, but the most important front-facing measures include the connection of online selling accounts. Every borrower must connect at least two online accounts in order to complete the application. These might be a PayPal, eBay, Amazon, MercadoLibre, Google Analytics, Debitoor (i.e. accounting software), or a bank account.

We then get ‘read-only’ access to these accounts and evaluate the data we find. In the case of Amazon we see the number of shipped orders for example, while a connected eBay account shows us the number and quality of feedback received. This, along with some additional data (like number of listed items), gives us a good idea of the borrower’s’ business acumen, which correlates with repayment probability.

We then get ‘read-only’ access to these accounts and evaluate the data we find. In the case of Amazon we see the number of shipped orders for example, while a connected eBay account shows us the number and quality of feedback received. This, along with some additional data (like number of listed items), gives us a good idea of the borrower’s’ business acumen, which correlates with repayment probability.

On top of that, Bank and PayPal accounts shed light on the financial health of the borrower and show outstanding loans from other service providers. Ensuring all borrowers are financially stable is a crucial step of the credit scoring system. Once a Google Analytics account is connected we see the traffic and revenue generated by the site. Because most of our borrowers run an online business, these metrics are good indicators whether an applicant runs a strong business and if they are creditworthy. Successful small business owners are far less likely to jeopardise their business and livelihood by failing to honour financial obligations.

Our credit scoring algorithm then takes this information along with thousands of other data-points to establish a credit rating for the applicant.

Crowdfund Insider: How do you manage defaults?

Radoslav Albrecht: At Bitbond we understand that keeping the default rate down is crucial to the success of our platform. That is why we have implemented a number of collection measures.

The first step is attracting creditworthy borrowers to the platform, and using a sophisticated credit scoring system, free of human bias, to rate applicants as accurately as possible. Then we require every user to go through a live video session to verify their identity with a security officer. Once these steps are completed, the applicant may publish a loan on our platform.

We start sending daily emails, reminding the borrower of his obligation to pay, should they fall behind on their payments. If this fails to get a response we move on to frequent phone calls and text messages, culminating in letters threatening legal action. If the borrower is communicative, we work together to figure out a payment plan which best serves both parties.

If our internal collection measures do not get a response, we pass the loan to our debt collection partner, which works to recoup the funds and disburse it to investors. This also includes potentially suing the defaulted borrower.

Crowdfund Insider: Are there any new features or verticals planned in the near future?

Crowdfund Insider: Are there any new features or verticals planned in the near future?

Radoslav Albrecht: The next step for us is to include the euro as a base currency. Once this is completed, we will turn our attention to creating a secondary market for investors to buy and sell notes on our platform.

We also plan to bring larger institutional investors onto the platform in 2017 in order to scale more efficiently.