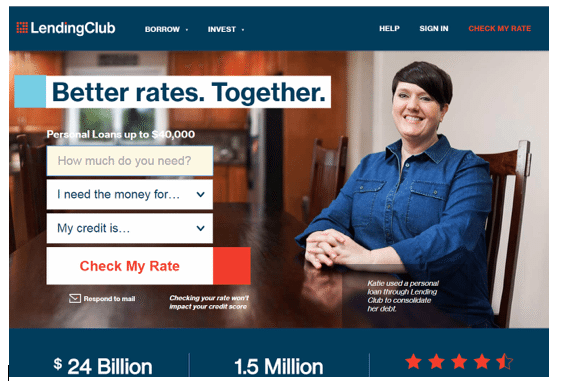

One of the fundamental differences between Chinese and US lending platforms can be found just by examining the home pages of their websites. Most, if not all, US platforms’ landing pages are targeted at borrowers and exhibit mainly information around borrowing whereas, on those of Chinese platforms, the information displayed on the home page are designed to attract new investors.

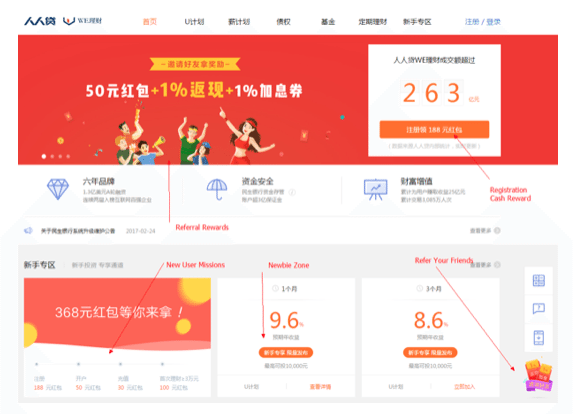

In most cases, the landing page directly lists the notes or wealth management products available for sale. Since US platforms rely primarily on institutional funding for loans, the need to attract and source borrowers has a higher priority in their overall marketing strategy than acquiring individual investors. The opposite is true for Chinese platforms: the lack of institutional funding has driven platforms to utilize a myriad of promotional and gamification strategies to acquire and retain individual investors.

LendingClub’s landing page contains only information for borrowers

US platforms rarely offer any promotions aside from a simple referral bonus. For example, SoFi offers a referral bonus for only new borrowers of particular loan products and is not targeted toward new investors. Even if we look at investor-facing wealth management platforms such as Betterment or Wealthfront, promotions are never overtly advertised on their websites or other advertisement channels. Meanwhile, Chinese lending platforms plaster their promotional offers on the banners of landing pages and headline their advertising message across various SEM and digital marketing channels.

Renrendai’s (aka. we.com) home page with over 80% of the display area dedicated to promotions for new users and referrals

Let’s first take a look at some of the basic tools and strategies Chinese platforms have at their disposal.

Cash Rewards

Rooted in tradition, the “red envelope” is the most common type of cash reward promotion found on nearly all Chinese lending platforms. In the industry’s earlier years, red envelopes were awarded for either new user registration or referrals. However, since legitimate phone numbers and personal information can be easily purchased on the black market in China, criminals often took advantage of these promotions by registering hundreds or thousands of fake accounts using stolen identities to extract rewards from platforms. Now red envelopes are offered as cash rewards for completing tasks more valuable to the platform, such as depositing funds or investing amounts beyond a specified threshold.

Rooted in tradition, the “red envelope” is the most common type of cash reward promotion found on nearly all Chinese lending platforms. In the industry’s earlier years, red envelopes were awarded for either new user registration or referrals. However, since legitimate phone numbers and personal information can be easily purchased on the black market in China, criminals often took advantage of these promotions by registering hundreds or thousands of fake accounts using stolen identities to extract rewards from platforms. Now red envelopes are offered as cash rewards for completing tasks more valuable to the platform, such as depositing funds or investing amounts beyond a specified threshold.

Discount Coupons

Red envelopes are also often offered in the form of discount coupons for note purchases. While the concept of using a coupon to buy retail goods may not translate

very well to the scenario of funding a loan, Chinese platforms make it work by funding the amount stated on the coupon.

Rate Boosters

Essentially a cash reward tied to the amount invested in a particular asset, these rewards are power-ups for investments. For example, a note with an 8% expected return becomes an investment that pays 9% when a 1% booster is applied. Since the platforms are providing the additional returns, the base amount on which the booster can be used is often capped.

Investment Simulators

In order to create a low barrier of entry for first-time investors, platforms offer investment simulations that recreate the investment process and attract users to complete the account opening process. The goal is to allow new investors walk through the entire investment process without actually using any of their own funds and receive rewards at the end to encourage actual investment. Upon registration, new users are given a high dollar value of “simulation funds” in the tens or even hundred thousand RMB range. These simulation funds can only be used to invest in fake notes offered by the platform for a short period, usually less than a week. At the end of the simulation period, the interest return on the fake note is rewarded to the investor in the form of a red envelope or discount coupon. The simulation funds themselves cannot be cashed out.

In order to create a low barrier of entry for first-time investors, platforms offer investment simulations that recreate the investment process and attract users to complete the account opening process. The goal is to allow new investors walk through the entire investment process without actually using any of their own funds and receive rewards at the end to encourage actual investment. Upon registration, new users are given a high dollar value of “simulation funds” in the tens or even hundred thousand RMB range. These simulation funds can only be used to invest in fake notes offered by the platform for a short period, usually less than a week. At the end of the simulation period, the interest return on the fake note is rewarded to the investor in the form of a red envelope or discount coupon. The simulation funds themselves cannot be cashed out.

Newbies Zone

The newbies zone is a step up from investment simulators. After a new investor has become comfortable with investing through the simulation process, platforms seek to convert the new investor with simple products that offer the highest returns only to first-time investors on the platforms. For example, if returns on a platform are typically around 8% APR, the newbies zone would offer first-time users investments with a 15% APR that have a shorter locked in term. Again, since it’s the platforms themselves making up for that additional return increase, the amount is usually capped to minimize such expenses.

Now let’s illustrate how a platform may use these tools and strategies to gamify the entire onboarding process to ultimately drive new investor referrals and first-time investments.

Investor A completed registration on a certain lending platform and immediately received a 50 RMB cash reward for verifying her identity and linking up a bank account.

Since an ongoing investment simulator promotion was occurring at the time, Investor A also receives 50,000 RMB in simulation funds to try out the investment process on the platform. The simulation is capped at 5 days, and upon its completion, the investment gives a return at an 8% APR totaling 55 RMB, which is awarded to Investor A in the form of a discount coupon.

Investor A then deposits 45 RMB of her own funds into the account and in combination with the 55 RMB coupon, she invests for the first time and funds a 100 RMB portion of a loan.

At this time, Investor A notices that there is a newbies zone where she can invest in notes that offer 15% APR returns for a period of 3 months (offer valid only on investments under 15,000 RMB). Investor A promptly deposits more money into the account and makes an investment at this attractive rate.

Now Investor A has taken advantage of all the promotional offers available for her first-time investment. However, she now notices that there are rewards for referring friends to the platform.

Investor A refers Investor B to the platform via a personalized link, and both investors receive a 50 RMB red envelope upon Investor B’s registration and bank account link up.

Investor B then goes through the entire simulation and newbie zone process and makes his first real investment. At this time, Investor A receives 1% referral commission based on Investor B’s initial investment. This commission is capped at 500 RMB. Investor A also receives a 1% rate booster that she can use for future investments not exceeding the amount of 20,000 RMB. Investor B also receives the same booster reward and then receives an additional 100 RMB cash reward since his initial investment exceeded a threshold amount of 30,000 RMB.

As illustrated above, incentive after incentive is offered to new investors to encourage them into completing the crucial milestone of investing for the first time. To gamify this process even further, these promotions are often laid out as “missions” for new users experiencing the platform for the first time.

Once the initial investment has been achieved, investors are further segmented by different metrics and these promotional tools are continuously applied to retain investors and increase their investments on the platform. For example, investors that meet duration goals for maintaining a balance for a specific time period are granted additional red envelopes or rate boosters.

Once the initial investment has been achieved, investors are further segmented by different metrics and these promotional tools are continuously applied to retain investors and increase their investments on the platform. For example, investors that meet duration goals for maintaining a balance for a specific time period are granted additional red envelopes or rate boosters.

In other cases, not unlike strategies employed by major commercial banks, investors that meet account balance goals are granted access to VIP customer service or other types of premium services. Furthermore, platforms may also partner with third parties and offer rewards such as Didi taxi credits, Pizza Hut coupons, or gift cards for popular Chinese e-commerce sites.

The variety of methods that Chinese lending platforms use to attract investors is astounding and can seem quite overwhelming to a western audience. However, Chinese users are accustomed to these types of promotional strategies, which have long been used in a similar fashion across a variety of platforms from e-commerce to social networking apps to even food delivery apps. For lending platforms seeking to leverage digital marketing channels to acquire users, it’s very necessary to employ an arsenal of promotional strategies to attract and compete for investors.

Until institutional funding becomes more widely available to Chinese lending platforms, we will continue to see this phenomenon. So in the near term, you may be able to tell which platforms are desperate for investors by looking at the area of their home page dedicated to advertising promotions and the value that these promotions offer.

Spencer Ang Li has served as Fincera’s Vice President of Product since June 2015 and as Chief Executive Officer for Fincera’s multiple product development subsidiaries since March 2014. Prior to joining Fincera, Mr. Li was an Investment Banking Analyst at Cogent Partners in New York, a sell-side advisor for private equity secondary transactions, from 2011 to 2014. During his tenure at Cogent, Mr. Li conducted fund due diligence, managed marketing processes, and participated in the sale and transfer of nearly $2 billion in limited partnership interests on behalf of public pensions, large regional banks, asset managers, and other financial institutions. Mr. Li received a BS in Economics and BA in Psychology from Duke University in 2011.

Spencer Ang Li has served as Fincera’s Vice President of Product since June 2015 and as Chief Executive Officer for Fincera’s multiple product development subsidiaries since March 2014. Prior to joining Fincera, Mr. Li was an Investment Banking Analyst at Cogent Partners in New York, a sell-side advisor for private equity secondary transactions, from 2011 to 2014. During his tenure at Cogent, Mr. Li conducted fund due diligence, managed marketing processes, and participated in the sale and transfer of nearly $2 billion in limited partnership interests on behalf of public pensions, large regional banks, asset managers, and other financial institutions. Mr. Li received a BS in Economics and BA in Psychology from Duke University in 2011.