The Cambridge Centre for Alternative Finance (CCAF), the leading global research institute for all things Fintech, has published its fourth annual survey on UK alternative finance. According to the report, entitled Entrenching Innovation: The 4th UK Alternative Finance Industry Report, the sector of emerging financial innovation grew by 43% in 2016, jumping to £4.3 billion in the UK. In 2015, the total amount was pegged at £3.2 billion. The CCAF said that UK startups and smaller businesses were the beneficiaries of alternative finance as it increasingly became an important source of growth capital.

As part of the research, the CCAF surveyed more than 8,300 investors and online lenders, as well as 77 crowdfunding and peer-to-peer platforms in the United Kingdom. Based on these findings, the CCAF has provided input to the Financial Conduct Authority (FCA), which is currently reviewing its regulatory regime for crowdfunding (which incorporates both P2P Lending and equity crowdfunding) in the UK.

As part of the research, the CCAF surveyed more than 8,300 investors and online lenders, as well as 77 crowdfunding and peer-to-peer platforms in the United Kingdom. Based on these findings, the CCAF has provided input to the Financial Conduct Authority (FCA), which is currently reviewing its regulatory regime for crowdfunding (which incorporates both P2P Lending and equity crowdfunding) in the UK.

In the six year period from 2011 through 2016, there has been a total of £11 billion in UK alternative finance market volume. Approximately 72% of all 2016 UK alternative finance market volume, or £3.3 billion, was raised for start-ups and SMEs. This is a dramatic increase of 50% versus year prior and thus makes an important policy statement for both regulators and elected officials to further streamline the alternative finance ecosystem. Approximately 33,000 smaller firms accessed these innovative funding channels in 2016 – in contrast to the 20,000 in 2015 – as awareness improved and platforms improved processes. In comparison to this rapid growth, the UK retail investor and lender market has remained relatively stable.

Bryan Zhang, Executive Director of the Cambridge Centre for Alternative Finance, commented on the report’s findings;

Bryan Zhang, Executive Director of the Cambridge Centre for Alternative Finance, commented on the report’s findings;

“Online alternative finance has become an ever more established component of the UK financial landscape. With equity-based crowdfunding now accounting for 17% of all seed and venture stage equity investment in the UK, and peer-to-peer business lending providing an equivalent of 15% of all new loans lent to small businesses by UK banks, alternative finance has entered the mainstream and is likely here to stay.”

[clickToTweet tweet=”equity-based #crowdfunding now accounting for 17% of all seed and venture stage equity investment in the UK” quote=”equity-based #crowdfunding now accounting for 17% of all seed and venture stage equity investment in the UK”]

“Progress in financial innovation is, nevertheless, not linear within such a dynamic landscape,” Zhang stated. “As market consolidation accelerates there is greater pressure on alternative finance platforms to distinguish themselves through better services and more innovative products, whilst simultaneously responding to emerging regulatory and supervisory demands.”

SyndicateRoom CEO and co-founder Gonçalo de Vasconcelos said the CCAF research confirmed the importance of alternative finance to the UK and the economy in general;

SyndicateRoom CEO and co-founder Gonçalo de Vasconcelos said the CCAF research confirmed the importance of alternative finance to the UK and the economy in general;

“This report by CCAF puts to rest any doubts about whether alternative finance was here to stay. It is. This is to be welcomed and celebrated by both investors and those looking for finance as a more efficient solution than mainstream finance players provide is now at their disposal. Not only are large financial institutions sitting up and noticing, they are more importantly starting to worry about a market that they used to take for granted. Competition has always been good for the end customer and alternative finance is no different.”

Anil Stocker, CEO and co-founder of invoice finance firm MarketInvoice, commented on the data in the CCAF research report;

Anil Stocker, CEO and co-founder of invoice finance firm MarketInvoice, commented on the data in the CCAF research report;

“We very much recognise this trend [alternative finance growth]. We advanced £414 million to UK businesses in 2016 during which we passed the £1b in cumulative funding milestone since we started in 2011. This year (2017) we’ve already advanced £657 million and are close to reaching £2 billion in funding (currently at £1.7 billion).”

Stocker said his Fintech business was adding new financing solutions due to increasing demand.

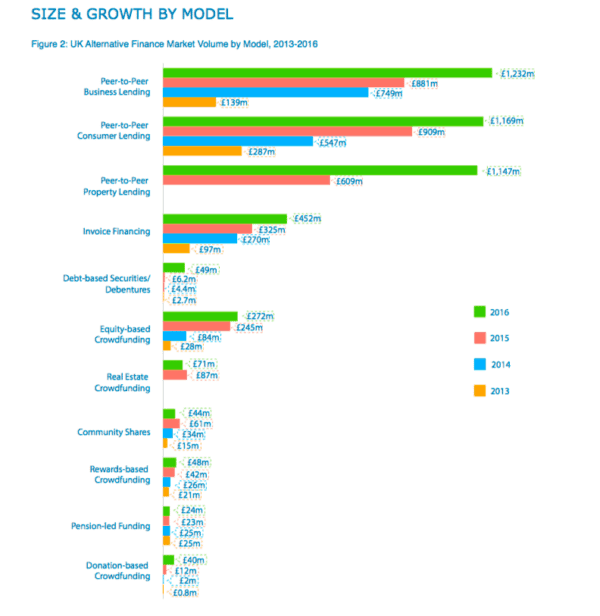

The report said peer-to-peer business lending was the largest market segment in 2016, growing by 36% last year to reach £1.23 billion. This was followed by peer-to-peer consumer lending at £1.17 billion (up 47%) and peer-to-peer property lending at £1.15 billion (up 88%).

Following the three top peer to peer lending sectors were: invoice trading (factoring) at £425 million, equity crowdfunding at £272 million, real estate crowdfunding at £71 million with rewards based crowdfunding being the smallest category at £48 million.

The UK alternative finance market was dominated by the five largest platforms that hoovered up 64% of activity in 2016. While few new entrants cropped up in 2016, over 35 UK platforms either merged or simply went away during the year.

Traditional finance became more involved in various sectors of alternative finance. The trend appears to be that established financial firms, including banks, asset managers and funds, accounted for 34% of peer to peer property lending, 28% of peer to peer business lending and 32% of peer to peer consumer lending.

Traditional finance became more involved in various sectors of alternative finance. The trend appears to be that established financial firms, including banks, asset managers and funds, accounted for 34% of peer to peer property lending, 28% of peer to peer business lending and 32% of peer to peer consumer lending.

According to the survey, 88% of loan-based crowdfunding platforms deemed existing FCA loan-based crowdfunding regulations to be adequate and appropriate. In contrast, 7% said existing rules are too relaxed and 5% believed they were too stringent.

For investment-based crowdfunding (encompassing equity-based crowdfunding and debt-based securities), 93% of surveyed investment-based crowdfunding platforms said existing FCA regulation is adequate and appropriate, with 7% finding them too relaxed and none finding the rules too stringent.

When asked by the CCAF, 84% of surveyed platforms said that they considered the FCA’s ongoing crowdfunding regulatory review process to be adequate and appropriate.

The CCAF report received support and backing from the CME Group. Kim Taylor, President, Clearing and Post-Trade Services of CME Group, commented that crowdfunding and peer to peer lending are just a few examples of innovations in finance that create new marketplaces;

The CCAF report received support and backing from the CME Group. Kim Taylor, President, Clearing and Post-Trade Services of CME Group, commented that crowdfunding and peer to peer lending are just a few examples of innovations in finance that create new marketplaces;

“The size and growth of the online alternative finance market, new entrants and partnerships, and the impacts on regulation and tax incentives, have the potential to transform the global economy,” said Taylor. “But this transformation can be best achieved only with thoughtful analysis and a thorough understanding of the alternative finance landscape. CME Group, as the world’s leading and most diverse derivatives marketplace, is proud to support the publication of this UK report through its Foundation.”

Bruce Davis, co-founder and Joint MD of Abundance Investment, who also helped to launch P2P lender Zopa, said the report painted a positive picture of the UK alternative finance market.

Bruce Davis, co-founder and Joint MD of Abundance Investment, who also helped to launch P2P lender Zopa, said the report painted a positive picture of the UK alternative finance market.

“This report provides a very positive picture of a new and exciting sector maturing steadily and providing an increasingly significant source of capital to the powerhouse of UK economic growth – startups and SMEs. Abundance was particularly pleased to see our category (debt securities) confirmed as the fastest growing of all at 1,147% year on year, with an accompanying 40% increase in average deal size to £1.4m. It was also good to see hard evidence of investors in debt securities conducting their own due diligence and being comfortable with the risk/reward offers they found.”

Zhang added that benefits go beyond a more effective financial services industry;

“Good financial innovation not only improves the efficiency of capital allocation and reduces information asymmetry, but also can achieve a greater degree of financial inclusion, increase welfare and benefit communities. In that sense, perhaps this report marks just the ‘end of beginning’ for the UK alternative nance industry”.

[clickToTweet tweet=”Financial innovation not only improves capital allocation but also can achieve greater financial inclusion #Fintech” quote=”Financial innovation not only improves capital allocation but also can achieve greater financial inclusion #Fintech”]