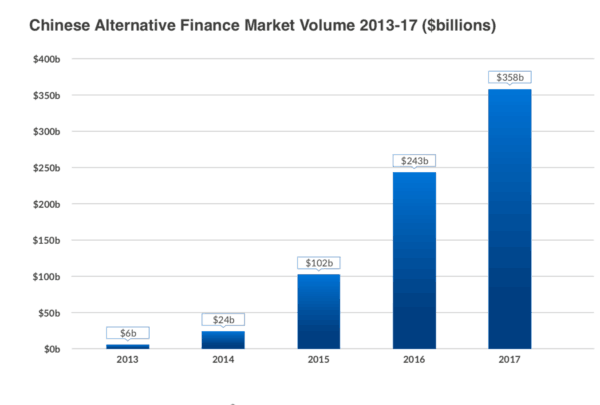

The Cambridge Centre for Alternative Finance (CCAF) is out with their 3rd Asia Pacific Region Alternative Finance Industry Report. According to CCAF, the alternative finance sector in the Asia Pacific (APAC) region increased to $358 billion in 2017 but overall growth has slowed.

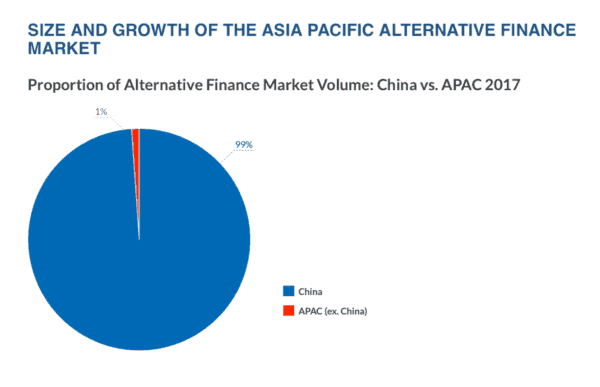

As in previous years, the APAC region was dominated by China, a market that accounts for around 99% of the total volume. The Report states that alternative finance in China grew at 47% rate – markedly lower than the year prior where alternative finance increased at a sturdy 138%. The slowing rate of growth in China was said to be due to sector consolidation and a changing regulatory environment.

Outside of China, alternative finance grew at 81%. The report is based on data collected from 340 alternative finance platforms in 29 countries across the region plus 782 platforms in China.

Even while ex-China growth was strong, the overall volume remains quite small in comparison with alternative finance growing from just $2 billion in 2016 to $3.6 billion in 2017. Australia was the second largest market at $1.15 billion with South Korea following at just over $1 billion.

Dr. Robert Wardrop, Director of CCAF, said this year’s report “illustrates the geographically uneven yet considerable growth of online alternative finance in many countries across the Asia Pacific region.”

Dr. Robert Wardrop, Director of CCAF, said this year’s report “illustrates the geographically uneven yet considerable growth of online alternative finance in many countries across the Asia Pacific region.”

In China, consumer-facing models continue to be the largest market segment for the third year but business finance was considerable at $111.8 billion having grown 20% versus 2016.

Business finance in China is almost entirely from the peer to peer/marketplace lending sector. In the rest of the region, business funding accounted for 61% of all volume, the equivalent to $2.23 billion, with debt-based models responsible for 98% of the volume.

Just as was reported in the CCAF UK report, institutionalization of funding continues to grow across the region. CCAF notes that institutional funding was most significant in Balance Sheet models (93%), followed by P2P/Marketplace Consumer Lending (43%) and Invoice Trading (42%) across the Asia Pacific region.

In regards to institutional money, India was the top market with 74% of its funding coming from institutional investors, followed by Australia (65%) and Indonesia (61%).

Other interesting data points gleaned from the CCAF research include:

- Regulation remains a “hot-button topic” across the region. In China, regulatory clampdowns has led to a fall in the number of platforms operating in the country.

- While the future of regulation is unclear in China, other countries such as Australia, Singapore and Malaysia have a more positive view of the regulatory ecosystem. Malaysia was the country where platforms were most satisfied with their regulatory regime.

- Even while growth has slowed in China it still tops other regions. The USA grew by 24% annually, and the UK grew by 35% annually. China is by far the global market leader in alternative finance ahead of the United States ($42.8 billion in 2017) and UK ($7.98 billion in 20172).

- The two largest models in China, P2P/Marketplace Consumer Lending and P2P/Marketplace Business Lending, both saw an annual increase in volume. P2P/Marketplace Consumer lending grew by 64%, accounting for $224 billion, and capturing 63% of the alternative finance market share in China.

- Real Estate Crowdfunding experienced exponential growth, growing by 1042% between 2016 and 2017, making it the fifth largest model. The model grew from a mere US$ 32.2 million in 2016 to US$ 367.9 million in 2017.

- Equity-based Crowdfunding experienced significant decline (52%) in 2016 and this trend was expected to continue into 2017. However, model volume grew by 2.4%.

- Over the last five years, online alternative finance has grown rapidly and has become an established means of financing for entrepreneurs, especially for SMEs across the Asia Pacific region. In fact, 61% of all alternative finance volume from the Asia Pacific went towards funding an SME in 2017.

The Report notes that China’s alternative finance industry is “facing challenges to its sustainability.” An economic downturn, tightening liquidity, and stricter regulations are taking a toll.

Professor Ben Shenglin, Dean of the Academy of Internet Finance at the Zhejiang University – a CCAF partner, qualified the Asia Pacific market as experiencing a “challenging period of transformation.”

Professor Ben Shenglin, Dean of the Academy of Internet Finance at the Zhejiang University – a CCAF partner, qualified the Asia Pacific market as experiencing a “challenging period of transformation.”

“Developing countries have experienced an inadequacy of regulatory capabilities, where too much “regulation leads to the cessation of activities all together, but no regulation leads to a messy market”. However, the gradually emerging ecosystem built by enterprises, governments and industry associations will lead to a bright future.”

Prof. Shenglin described the shift as being “from quantity to quality.”

CI contacted Prof. Shenglin to clarify this statement:

“This statement is more applicable to Chinese market, which experienced a period of “Wild West” growth before the recent introduction and tightening of regulations. The industry has been going through a rapid “consolidation” process with number of platforms rapidly decreasing, demonstrating the flight to “quality” (and most of time also scale, the larger platforms).”

This being the case, has the pendulum swung too far too fast in China? Prof. Shenglin said it has due to a “nationwide campaign style” of government actions, the absence of updated/coherent regulations and/or their lack of clarity such as who has the jurisdiction, the central government or local government, the central bank or banking/insurance/securities regulators.

“What is encouraging is that there is now a consensus and concerted effort,” Prof. Shenglin added.

Asked about the impact of blockchain, a sector of Fintech where China is quite active, Prof. Shenglin said that emerging blockchain platforms are not necessarily disrupting the distruptors but are there to improve and supplement the platforms.

As for the emergence of institutional money fueling the alternative finance sector, Prof. Shenglin said that a lot of capital has been invested in the sector in China in the form of VC/PE stakes, as institutional lenders are few and far between in China, given the lack of market benchmarks, transparency and liquidity and general maturity of the institutional investors.

“China has achieved the scale (market volume) despite the lack of institutional participation, but sustaining it has become a challenge,” Prof. Shenglin explained. “There have been some partnerships between institutions like banks, asset managers and the platforms. The sector of micro-loan lenders (mainly institutional money) are embracing the digital bandwagon and may enter the space, provided that the regulations become less burdensome for them.”

The report is jointly produced by The Cambridge Centre for Alternative Finance at University of Cambridge Judge Business School, The Academy of Internet Finance at Zhejiang University, and the Asian Development Bank Institute. The report was also supported by KPMG Australia, Invesco, and CME Group Foundation.

The 3rd Asia Pacific Region Alternative Finance Industry Report is available below.