Rangewell, a business finance firm that assists SMEs in accessing capital, has launched a dashboards tracking the Coronavirus Business Interruption Loan Scheme (CBILS) and the Bounce Back Loans – two UK government programs providing support to smaller firms that have struggled in the wake of the COVID-19 pandemic. While the data is publicly available posted by the UK government, Rangewell has posted a more visually appealing depiction of these two programs.

Rangewell notes that the value of payments via the Bounce Back Loan Scheme in the first week alone surpassed the total amount of CBIL Loans in totality to date – an incredible leap. Bounce Back Loans received a 90% approval rating in the 2nd week funding £14.2 billion in total.

During the full period for both schemes, the average size of Bounce Back Loans has been £30,534 versus £178,334 for CBILS loans.

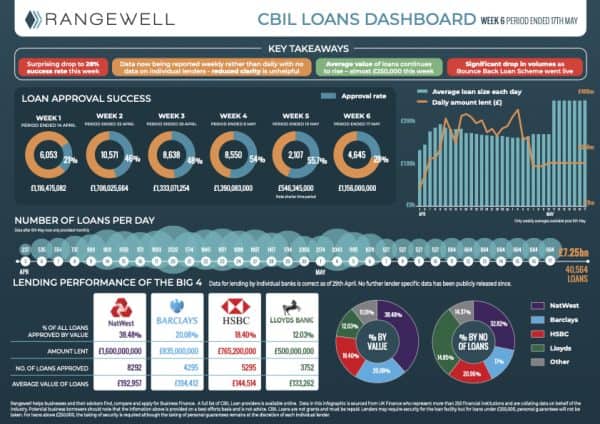

Approval rates for CBILS last week was only 28% compared to the overall rate of 50% since the scheme started. The reason for this change is not quite clear.

The volume of CBILS applications has continued to fall but the value of approved loans is now at £249,000 – the highest to date (compared to an average since start of £178,334). The Bounce Back Loans are probably garnering the bulk of the loans under £50,000.

Nic Conner, Rangewell’s Research Consultant, said that with the 7th week of CBILS data and the 3rd week of Bounce Back Loan information, we run the risk of “data blindness” hence Rangewell’s attempt to produce a visually appealing depiction of lending activity:

“Most of the data we use for the dashboard is released once a week by the Treasury. It is not as detailed or as helpful as it should be given it only contains headline figures, rather than a detailed breakdown: By sector, By region By lender. Rangewell recently wrote an open letter to the Chancellor calling for the data to be released in more detail and via open data. We welcome their move a few weeks ago to publish this information but they need to go further.”

Connor believes the current data provided by the UK government is not fully transparent and that if public officials want to ensure greater success they encourage more granular information that will allow banks, other lenders, trade associations etc. to monitor activity:

“Although it’s unfashionable to say so, the response from lenders, on the whole, has been highly impressive in terms of the volume of loans they have been able to approve – on the ground, we have seen impressive examples of local managers at all lenders doing everything they can to help their business clients,” said Conner. “It is important to note that, especially with the Bounce Back Loans, participating lenders are not going to profit from the Scheme. The small size of the loans, substantial administrative costs and the high expected losses that they will have to manage on behalf of the government make that a certainty – in our opinion, their participation should be seen as a genuine effort to step up and help the British economy; as well as, no doubt, reacting to a certain extent to government “requests”.”

Rangewell encourages the government to consider more detail going forward:

“We see most switched-on businesses now preparing for the next 6 – 18 months, rather than just on day-to-day survival. The government should be thinking and planning alongside them for the next stage of economic recovery.”