In a stunning development earlier today, the SEC released final Regulation A+ rules under Title IV of the JOBS Act that pre-empts state law for larger Regulation A offerings up to $50M and provides for state coordinated review for offerings up to $20M. Growth companies will now soon be able to raise up to $50 million from unaccredited investors in a mini-IPO style offering serving as a potential alternative to venture capital or other institutional capital. Imagine Uber or AirBnb, instead of going to big institutions for capital, now offering their stock directly to their drivers, riders, renters and tenants as well as the general public.

When the JOBS Act was passed in April of 2012, many believed that Title IV would actually be the most powerful change, but given that there was no deadline for implementation of the rules, most ignored Title IV as too remote to pay serious attention. There was also concern about the same problem that haunts existing Regulation A, namely state securities laws that would require registration in every individual state where securities are sold making it too expense/complicated to be workable. The infamous example of this was in 1980 when Massachusetts deemed the offering of Apple Computer stock to be “too risky” and did not allow its citizens to participate in the offering.

In December of 2013, however, the SEC shocked the securities community by introducing Proposed Regulation A+ rules that, through a clever legal maneuver, pre-empted state securities regulation.

Since that stunning announcement, there has been great uproar about “pre-emption,” whether it is legal and whether it is appropriate for a federal agency to pre-empt the states in this manner. Most in the pro-business community ardently support pre-emption argue that securities offerings constitute interstate commerce and that state by state regulation is antiquated in a world where the internet blurs state lines. Many regulators, investor protection groups and even one crowdfunding platform opposed such pre-emption, arguing that state review adds value and necessary investor protections. In response, the states introduced a coordinated review process, which was designed to address these concerns. Critics argued that this was too little, too late and only resulted from the states being forced to act by the threat of pre-emption.

Since that stunning announcement, there has been great uproar about “pre-emption,” whether it is legal and whether it is appropriate for a federal agency to pre-empt the states in this manner. Most in the pro-business community ardently support pre-emption argue that securities offerings constitute interstate commerce and that state by state regulation is antiquated in a world where the internet blurs state lines. Many regulators, investor protection groups and even one crowdfunding platform opposed such pre-emption, arguing that state review adds value and necessary investor protections. In response, the states introduced a coordinated review process, which was designed to address these concerns. Critics argued that this was too little, too late and only resulted from the states being forced to act by the threat of pre-emption.

In the final rule release, the SEC settled the dispute through a brilliant compromise by confirming pre-emption for Tier II Regulation A offerings up to $50M but also increasing Tier I Regulation A offerings from $5M to $20M and leaving pre-emption intact, thus giving “coordinated review” a chance to prove itself. This appears to be the result of an extensive negotiation between Commissioner Stein who opposes pre-emption and several of the other Commissioners. In coming to this decision, the SEC noted that:

- Coordinated review is new and unproven and pre-emption is necessary at least until there is a track record of a functioning coordinated review program

- Coordinated review has great potential if the states can stick together and maintain a seamless process

- NASAA may appoint an individual to serve with the SEC internally on implementation of Reg A+

- States will retain full enforcement and anti-fraud jurisdiction in all cases

Now, with pre-emption under Tier II and coordinated review under Tier I, it looks like Title IV (Reg A+) could make Title III Crowdfunding a relic.

Here are the highlights of the new Regulation A+ exemption:

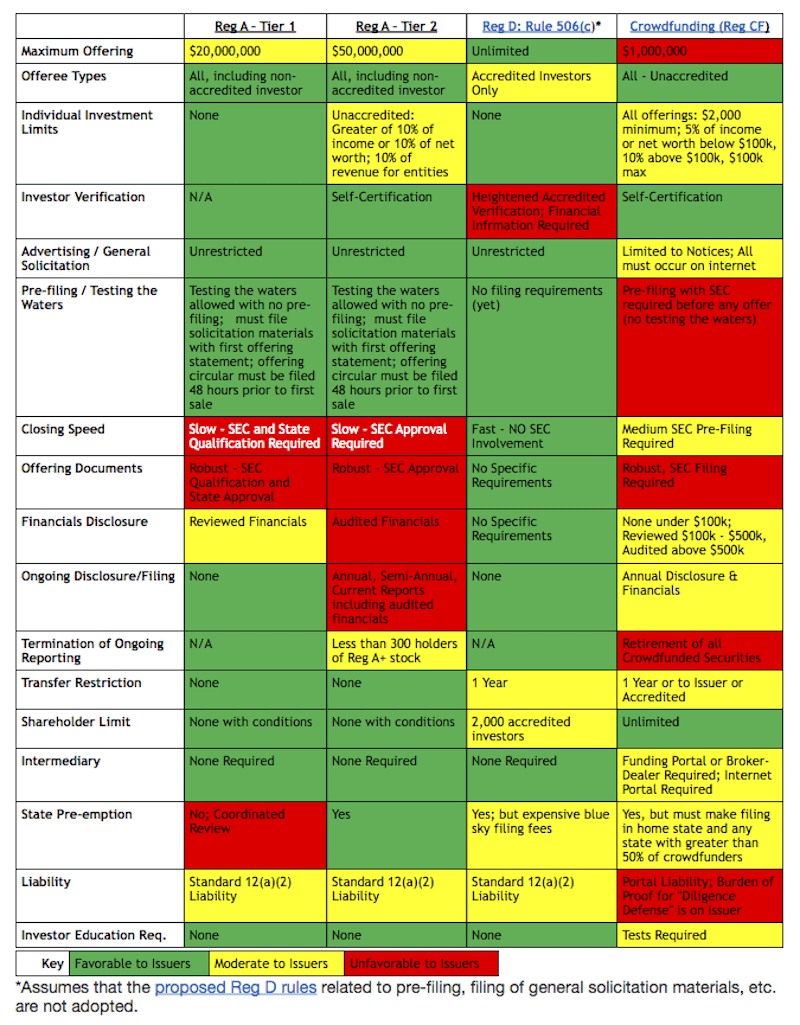

- High Maximum Raise: Issuers can raise up to $50,000,000 in a 12 month period for Tier II and $20,000,000 for Tier 1.

- Anyone can invest: Not limited to just “accredited investors” – your friends and family can invest. Tier 2 investors will, however, be subject to investment limits described below.

- Investment Limits: For Tier II, individual non- accredited investors can invest a maximum of the greater of 10% of their net worth or 10% of their net income in a Reg A+ offering (per offering). There is no limit for accredited investors in Tier II. There are no investment limits under Tier 1.

- Self-Certification of Income / Net Worth: Unlike Rule 506(c) under Title II of the JOBS Act, investors will be able to self-certify their income or net worth for purposes of the investment limits so there will be no burdensome documentation required to prove income or net worth.

- You can advertise your offering: There is no general solicitation restriction so you can freely advertise and talk about your offering, including at demo days, on television, and via social media.

- Offering Circular Approval Required: The issuer will have to file a disclosure document and audited financials with the SEC. The SEC must approve the document prior to any sales. The proposed indicate that the Offering Circular will receive the same level of scrutiny as a Form S-1 in an IPO. This is the biggest potential drawback of using Reg A+.

- Audited Financials Required: For Tier 2, together with the Offering Circular, the issuer will be required to provide two years of audited financial statements. Tier 1 offerings require only reviewed financials (not audited).

- Testing the Waters: An issuer can “test the waters” and see if there is interest in the offering prior to spending the time and money to create the Offering Circular. This would be “Preview” mode on SeedInvest where investors can express interest, but can’t yet invest. This is important so that companies don’t have to gamble on their fundraise and can see if there is interest prior to investing in legal and accounting fees.

- Ongoing Disclosure Requirements: For Tier 2, the issuer will be required to make an annual disclosure filing, a semi-annual report, and current reports, each of which are scaled back versions of Form 10-K, Form 10-Q and Form 8-K, respectively. These reports will also require ongoing audited financials. These disclosures can be terminated after the first year if the shareholder count drops below 300. There are no ongoing disclosure requirements for Tier 1.

- State Pre-Emption: As discussed above, the old Regulation A (now Tier I) was never used because it required registering the securities in every state that you make an offer or sales. New Reg A+ Tier 2 preempts state law – again – this is huge. Tier 1 Reg A+ again does not have state pre-emption but will be a testing ground for NASAA Coordinated Review.

- Shareholder Limits: In a welcome departure from the proposed rules, it appears that the Section 12(g) shareholder limits (2,000 person and 500 non-accredited investor) will not apply to Reg A under certain circumstances. This fixes a major problem from the proposed rules which would have limited the potential for very small investments (i.e. $100).

- Unrestricted Securities: The securities issued in Reg A+ will be unrestricted and freely transferable, though many issuers may choose to impose contractual transfer restrictions. Many believe this will pave the way for a secondary market for these securities in the form of Venture Exchanges.

- No Funds: Investment companies (i.e. private equity funds, venture funds, hedge funds) may not use Reg A to raise capital.

- Integration: There are several safe harbors so it seems that you can use Reg A+ in combination with other offerings. There are safe harbors for the following:

No integration with any previously closed offerings

No integration with a subsequent crowdfunding offering

No integration where issuer complies with terms of both offerings independently – can conduct simultaneous Reg D – 506(c) offering.

Also, interestingly, the SEC did not mention Title III Equity Crowdfunding a single time either in this meeting or in Chairman White’s recent testimony before Congress. This furthers the belief by many that Title III Equity Crowdfunding is dead in the water as it currently stands and may only be revived by an act of Congress.

Regulation A+ will likely go into effect 60 days after publication in the Federal Register (June 2015).

See: Title IV of the JOBS Act Final Rules

Check out this chart comparing Reg A Tier 1, Reg A Tier 2, Reg D: Rule 506(c) and Regulation Crowdfunding:

Kiran Lingam is General Counsel at equity crowdfunding platform SeedInvest. In his time before SeedInvest, Kiran worked as a corporate and securities attorney at the law firms of Jones Day LLP and DLA Piper LLP, where he served as outside legal counsel to venture capital and private equity funds, angel groups and over 30 technology startups. He has seen first-hand the struggles encountered by early stage entrepreneurs and believes strongly that many more startups would be successful with additional avenues for early stage capital. Since passage of the JOBS Act, Kiran has been an active speaker, writer and commentator on crowdfunding and the related legal issues. He is a Charter Member and Executive Team member of TiE (The Indus Entrepreneurs) and is an active member of a number of groups in the New York startup community. Kiran received a B.A. in Economics from Cornell University and a J.D., with honors, from the University of Georgia.

Kiran Lingam is General Counsel at equity crowdfunding platform SeedInvest. In his time before SeedInvest, Kiran worked as a corporate and securities attorney at the law firms of Jones Day LLP and DLA Piper LLP, where he served as outside legal counsel to venture capital and private equity funds, angel groups and over 30 technology startups. He has seen first-hand the struggles encountered by early stage entrepreneurs and believes strongly that many more startups would be successful with additional avenues for early stage capital. Since passage of the JOBS Act, Kiran has been an active speaker, writer and commentator on crowdfunding and the related legal issues. He is a Charter Member and Executive Team member of TiE (The Indus Entrepreneurs) and is an active member of a number of groups in the New York startup community. Kiran received a B.A. in Economics from Cornell University and a J.D., with honors, from the University of Georgia.