(This is First in a Series of Articles Focusing on the Road Ahead to Final Rules and Beyond)

(This is First in a Series of Articles Focusing on the Road Ahead to Final Rules and Beyond)

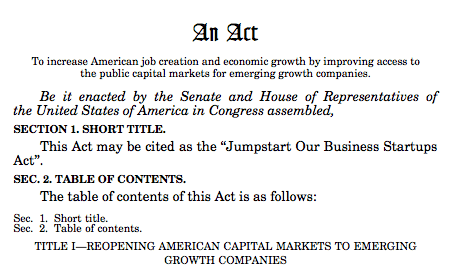

Like many others around the country and around the world, I was excited to hear that nearly 19 months after the JOBS Act was signed into law, and more than nine months after the 270 day deadline set by Congress to enact the Title III crowdfunding regulations, the SEC Commissioners were finally meeting yesterday to propose the long awaited crowdfunding regulations.

And like many other SEC observers and crowdfunding supporters, I was heartened to see and hear five SEC Commissioners unanimously approve the proposed crowdfunding rules – certainly a far cry from the contentious divisions at the Commission level which accompanied the initial Title II JOBS Act rules allowing general solicitation in unregistered offerings, which ushered in historic changes last July.

Given the monumental directive that Congress had given to the SEC, to propose and implement regulations for a new investor market, equity crowdfunding, and the widespread controversy swirling around crowdfunding, it is no wonder that when the proposed rules were finally issued the Commissioners were sending shout-outs to the more than 50 SEC staffers who wrestled with the unenviable task of fitting a square peg (crowdfunding) into the rigid regulatory hole of market regulation, that took root more than 80 years ago following the stock market crash of 1929.

Given the monumental directive that Congress had given to the SEC, to propose and implement regulations for a new investor market, equity crowdfunding, and the widespread controversy swirling around crowdfunding, it is no wonder that when the proposed rules were finally issued the Commissioners were sending shout-outs to the more than 50 SEC staffers who wrestled with the unenviable task of fitting a square peg (crowdfunding) into the rigid regulatory hole of market regulation, that took root more than 80 years ago following the stock market crash of 1929.

The SEC’s mission then, and for decades thereafter, has been to oversee laws intended to protect the integrity of the marketplace and the uninformed investor – so as to avoid another calamitous financial meltdown – while at the same time shaping and regulating market structures that would facilitation capital formation. To this end, a company normally could not solicit investments from unaccredited investors outside a very small circle of friends absent registering the offering with the SEC and being subjected to even more stringent state Blue Sky regulations.

Yet ironically, in 2012, out of the midst of the collapse of financial markets and record joblessness – in what economists dubbed “The Great Recession” – Congress gave birth to a new market structure, crowdfunding, to create jobs –with a vehicle that would allow startups and small businesses, using the power of the Internet, to raise capital from large numbers of investors, both accredited and unaccredited. However this new vehicle was intended to thrive without the burden and expense of registering the securities offering with federal and state regulators. At least that was the theory.

It is no small wonder, therefore, that the long awaited proposed rules were couched by the SEC in a 565 page release – and seeking comment from the public on over 200 issues.

The statement by Commissioner Kara Stein at the Commission’s October 23, 2013, meeting approving the proposed regulations aptly summed up the magnitude of the task:

The statement by Commissioner Kara Stein at the Commission’s October 23, 2013, meeting approving the proposed regulations aptly summed up the magnitude of the task:

The proposal before us is a particularly challenging one for the Commission. Today, we are proposing an entirely new regime for the regulation of some types of securities offerings. The proposal before us seeks to strike a balance between our statutory duty to create a new regulatory regime for capital formation and our longstanding duty to protect investors.

Initial Impressions

First impressions are often incorrect. My initial take of the proposed regulations following their release was captured in my 140 character Tweet yesterday, far less words than contained the 565 page rule release:

Samuel Guzik @SamuelGuzik1: SEC Meeting: Excellent Tone by Commissioners – The Devil Will be in the (innumerable) Details – Lots of Work Ahead to Get to the Finish Line

Having now had the opportunity to read the proposed regulations in more depth – I stand by my Tweet. However, given the volume of material in the release, and the relatively short period of time in which to digest it, I am granting myself license to revise and extend my remarks in the coming days and weeks.

Moreover, because of the amount of detail contained in the proposed regulations and the issues they raise, I will be covering the proposed rules and the statutory provisions of Title III over several articles – focusing on different aspects of the regulations and the related statutory provisions – with analysis and insight as to how the current regulatory framework should change in order for crowdfunding to succeed. For now, suffice it to say that as much as crowdfunding is a revolution, it will at the same time be an evolution that will, in my opinion, require further rulemaking and Congressional action.

On the bright side for crowdfunding

On the bright side for crowdfunding

These rules are proposed rules, and are subject to a public comment period, further deliberation by the Commission and a final Commission vote. And as to those impediments to a robust equity crowdfunding ecosystem which are embedded in the JOBS Act itself, and therefore require further legislation to correct, a majority of Congress is up for re-election 12 months from now (as in JOBS Act 2.0 and the power of the (voting) crowd).

From Title II to Title III – What a Difference a Roman Numeral Makes

Title II of the JOBS Act was relatively straightforward – issuers could engage in general solicitation and advertising in a private placement of unlimited dollar amounts, without registering with the SEC, so long as all of the money raised was from accredited investors and the issuer had taken reasonable precautions to ensure that all of the investors were in fact accredited. Though implementation of Title II was dependent upon SEC rulemaking, the truth of the matter is that there was very little latitude in this part of the JOBS Act for SEC rulemaking.

Title III of the JOBS Act, crowdfunding, was an entirely different matter.

Many interested parties had their hand in crafting of this new, and radically different market –crowdfunders, state securities regulators, FINRA, and consumer protection advocates, to name a few. Each left their mark on the final product known as Title III. And though a myriad of finishing details were left to the discretion of the SEC, the fundamental provisions defining this new market were, in effect, carved in stone. Unlike Title II, however, Congress expressly directed the SEC to use its rulemaking powers to protect investors –authority which was conspicuously absent from Title II.

With the focus of Title III crowdfunding squarely on investor protection, the proposed rules are true to this tenet – a market structure with built in circuit breakers, firewalls and provisions intended to weed out shady stock promotions.

With the focus of Title III crowdfunding squarely on investor protection, the proposed rules are true to this tenet – a market structure with built in circuit breakers, firewalls and provisions intended to weed out shady stock promotions.

The Highlights

Following is a summary of the highlights in the proposed regulations.

Intermediaries – Crowdfunded offerings must be conducted through an intermediary, either a “funding portal” registered with the SEC and subject to FINRA rules, or a licensed broker-dealer.

Limitation on Total Amount Raised – $1,000,000 in a 12 month period is the maximum raise under the crowdfunding exemption, Section 4(a)(6) of the Securities Act.

Limitation on Amount Invested – Limitations on amount invested, which were ambiguous (by the SEC’s admission) in the original JOBS Act, have been clarified in the proposed rule:

Investors, over the course of a 12-month period, would be permitted to invest up to:

$2,000 or 5 percent of their annual income or net worth, whichever is greater, if both their annual income and net worth are less than $100,000.

10 percent of their annual income or net worth, whichever is greater, if either their annual income or net worth is equal to or more than $100,000. During the 12-month period, these investors would not be able to purchase more than $100,000 of securities through crowdfunding. The net equity in the investor’s primary residence would be excluded.

And as rumored last week in the media by Bloomberg Businessweek, the proposed regulations provide that investors will “self-certify” these requirements, with no independent verification required – a detail left out of the statute itself.

Excluded Issuers – Title III carved out exclusions for certain types of companies, but leaving the SEC with a free hand to add to the list where necessary to protect investors. The original Act excluded from the crowdfunding exemption non-U.S. companies, companies that are reporting companies (filers of annual and quarterly reports with the SEC), and companies whose management and affiliates were “bad actors” under SEC disqualification provisions. Added to the list in the proposed regulations are “shell companies,” essentially companies with no specific business plan or whose business plan is to engage in a merger or acquisition with an unidentified company.

Restrictions on Resale of Crowdfunded Securities – The proposed regulations add little of significance to restrictions on resale of securities acquired in a crowdfunded offering. Securities purchased In a crowdfunded offering may not be resold for one year, with limited exceptions:

To the issuer of the securities;

To an accredited investor;

As part of an offering registered with the Commission; or

To a member of the family of the purchaser or the equivalent, to a trust controlled by the purchaser, to a trust created for the benefit of a member of the family of the purchaser or the equivalent, or in connection with the death or divorce of the purchaser or other similar circumstance.

Offering Disclosure – Title III spelled out in some detail the types and categories of disclosure required to be provided by the issuer to the investor for an offering – the regulations track the statutory disclosure, but with additional detail – some of it resembling the type of information required in a registered offering.

The nature and extent of disclosure will certainly be a focus of attention in the upcoming weeks and months by those who believe that equity crowdfunding under Title III is overburdened with rules and regulations which increase its complexity and cost.

The issuer will be required to file its disclosures with the SEC (under cover of a new “Form C”), and provide these disclosures to the intermediary and investor.

This information must be made publicly available on the intermediary’s platform, in a manner that reasonably permits a person accessing the platform to save, download, or otherwise store the information.

This information must be made publicly available on the intermediary’s platform for a minimum of 21 days before any securities are sold in the offering, during which time the intermediary may accept investment commitments.

The required disclosures include:

Information about officers and directors, including business experience during the past three years

Identity of the owners of 20 % or more of the company.

A description of the company’s business and the anticipated business plan.

The price to the public of the securities being offered or the method for determining the price, the target offering amount, the deadline to reach the target offering amount, whether the company will accept investments in excess of the target offering amount, and procedures for oversubscription.

Information regarding related party transactions during the past year , or presently proposed, involving officers, directors or 20% owners

A description of the financial condition of the company, including a discussion, to the extent material, of historical results of operations, liquidity and capital resources. For companies with no operating history, the description should include a discussion of financial milestones and operational, liquidity and other challenges.

A description of the financial condition of the company, including a discussion, to the extent material, of historical results of operations, liquidity and capital resources. For companies with no operating history, the description should include a discussion of financial milestones and operational, liquidity and other challenges.

Financial statements of the company for the two most recent years, the type depending upon the amount raised in the offering, but including in all cases, a balance sheet, income statement, statement of cash flows and statement of changes in owners; equity and notes to the financial statements, all prepared in accordance with U.S. GAAP:

$100,000 or less – tax returns of the issuer for the most recently completed year; and financial statements, certified the company’s CEO.

Up to $500,000 – financial statements for the past two years “reviewed” by an independent accountant.

Over $500,000 – financial statements for the past two years, audited by an independent accountant.

A “reasonably detailed” description of the use of proceeds.

Discussion of all material risk factors.

The target offering amount, the deadline to meet the target, and procedures regarding oversubscription .

Description of the process to complete the transaction or cancel an investment commitment, including a statement that the investor may cancel until 48 hours prior to the deadline identified in the offering materials. If material changes to the offering or to the information provided by the issuer regarding the offering occur within five business days of the maximum number of days that an offering is to remain open, the offering must be extended to allow for a period of five business days for the investor to reconfirm his or her investment.

A description of the ownership and capital structure of the issuer, including the terms of the securities offered and/or outstanding, whether the securities have voting rights, how the offered securities may be modified, and a summary of the differences between the offered securities and each other class of security of the issuer, and how the rights of the offered securities may be limited, diluted or qualified by the rights of other securities of the company.

A description of how the exercise of rights by the principal shareholders could affect purchasers of the offered securities.

How the securities are being valued, and examples of methods for how such securities may be valued by the issuer in the future, including during subsequent corporate actions.

The risks to purchasers relating to minority ownership and the risks associated with corporate actions such as issuance of additional securities, repurchases of securities by the company, sale of the company or its assets, or transactions with related parties.

A description of the material terms of any outstanding debt of the issuer.

A description of the material terms of any offerings conducted during the past three years, including the exemption from registration relied upon.

Filing for Material Changes for the Offering –Information regarding material changes to the disclosed information prior to completion of the offering must be provided to investors and filed with the SEC under new Form C-A. In the event of material changes, the investor’s money will be returned unless the investor re-affirms the investment within five business days.

Filing to Report Progress Updates – Form C-U must be filed with the SEC and furnished to the investors and intermediary, to disclose progress in raising the offering amount no later than five business days after the issuer reaches 50% and 100% of the target offering amount.

Post-Offering Disclosure -Annual Reports – The proposed regulations provided that an issuer must file an Annual Report on Form C-AR within 120 days after the end of each fiscal year. The information required to be disclosed annually is similar to the categories of information provided for the original offering, excluding information relating to the terms of the completed offering.

Advertising for the Offering– Both Title III of the JOBS Act and the proposed regulations prohibit advertising a crowdfunded offering, directly or indirectly, by the issuer, except for notices that direct investors to the intermediary’s platform. The proposed rules provide some additional detail regarding what may be contained in the issuer’s notice, permitting an issuer to provide information regarding the terms of the offering and a brief description of the company’s business.

Advertising for the Offering– Both Title III of the JOBS Act and the proposed regulations prohibit advertising a crowdfunded offering, directly or indirectly, by the issuer, except for notices that direct investors to the intermediary’s platform. The proposed rules provide some additional detail regarding what may be contained in the issuer’s notice, permitting an issuer to provide information regarding the terms of the offering and a brief description of the company’s business.

In what appears to be a departure from Title III’s strict prohibition by the issuer on advertising, the proposed rules provide that an issuer may communicate with investors and potential investors about the “terms of the offering” through communication channels provided by the intermediary on the intermediary’s platform, provided that an issuer identifies itself as the issuer in all communications. Note, however, that information regarding terms of the offering is limited to information regarding the amount of securities offered, the nature of the securities, the price of the securities and the closing date of the offering period.

Promoter compensation – A company is permitted to compensate a person to promote its crowdfunded offering through communication channels provided by an intermediary on the intermediary’s platform, but only if the issuer takes reasonable steps to ensure that such person clearly discloses the receipt, past or prospective, of such compensation with any such communication. A founder or an employee of the issuer that engages in promotional activities on behalf of the issuer through the communication channels provided by the intermediary must disclose, with each posting, that he or she is engaging in those activities on behalf of the issuer.

Intermediary’s Rights and Duties

One of the hallmarks of Title III crowdfunding is the requirement that crowdfunded securities be offered and sold through an intermediary which is either a licensed broker-dealer or a funding portal registered with the SEC. The intermediaries have rights and duties relating to such things as monitoring funds, providing educational materials, and obtaining a certification from the issuer that it has established means to keep accurate records of the holders of the securities it would offer and sell through the intermediary’s platform.

As to the two types of intermediaries created by the JOBS Act for crowdfunding – licensed broker-dealers and SEC registered funding portals, they have different rights and duties – such as the ability to curate crowdfunding companies. These differences could have major implications for a company seeking to complete an equity crowdfunding – they will be analyzed and discussed in a subsequent article.

Denial of Access to Intermediary’s Platform – The intermediary also has a duty to take certain actions in order to reduce the risk of fraud. In particular:

Denial of Access to Intermediary’s Platform – The intermediary also has a duty to take certain actions in order to reduce the risk of fraud. In particular:

An intermediary is required to deny a company access to its platform unless the intermediary has a reasonable basis for believing that neither the issuer nor any of its officers, directors (or any person occupying a similar status or performing a similar function) or beneficial owners of 20 percent or more of the issuer’s outstanding voting equity securities, calculated on the basis of voting power, is subject to a disqualification under the “bad actor” provisions. To fulfill this requirement, an intermediary must, at a minimum, conduct a background and securities enforcement regulatory history check on each issuer whose securities are to be offered by the intermediary and on each officer, director or beneficial owner of 20 percent or more of the issuer’s outstanding voting equity securities.

An intermediary must also deny access to its platform if it believes that the issuer or the offering presents the potential for fraud or otherwise raises concerns regarding investor protection. In satisfying this requirement, an intermediary must deny access if it believes that it is unable to adequately or effectively assess the risk of fraud of the issuer or its potential offering. In addition, if an intermediary becomes aware of information after it has granted access that causes it to believe that the issuer or the offering presents the potential for fraud or otherwise raises concerns regarding investor protection, the intermediary must promptly remove the offering from its platform, cancel the offering, and return or direct the return of any funds that have been committed by investors in the offering.

Investor Questionnaire –The intermediary is responsible for obtaining a questionnaire completed by the investor demonstrating the investor’s understanding that:

There are restrictions on the investor’s ability to cancel an investment commitment and obtain a return of his or her investment;

It may be difficult for the investor to resell securities acquired in reliance on Section 4(a)(6) of the Securities Act; and

Investing in securities offered and sold in reliance on Section 4(a)(6) of the Securities Act involves risk, and the investor should not invest any funds in an offering made in reliance on Section 4(a)(6) of the Securities Act unless he or she can afford to lose the entire amount of his or her investment.

Communication Channels – An intermediary must provide on its platform communication channels by which persons can communicate with one another and with representatives of the issuer about offerings made available on the intermediary’s platform. However, if the intermediary is not a licensed broker-dealer, the intermediary is generally not allowed to participate in these communications other than to establish guidelines for communication and remove abusive or potentially fraudulent communications.

The Bottom Line

There is a lot of detail and nuance in the proposed regulations – which will be addressed by me in future articles. For those of us who see the value and potential in equity crowdfunding, there is more work to be done before we get to the finish line.

____________________

Samuel S. Guzik is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience. He is admitted to practice before the SEC and in New York and California. During this time he has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.

Samuel S. Guzik is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience. He is admitted to practice before the SEC and in New York and California. During this time he has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.