The recent economic downturn is not the only challenge for entrepreneurs in the EB-5 and JOBS Act industries. Rather, the challenges include close regulatory scrutiny by the United States Securities and Exchange Commission’s (SEC) Division of Enforcement. While both EB-5 and the JOBS Act were designed by Congress to generate capital, jobs and ultimately growth, both industries face identical scrutiny by the SEC on two key issues. The first is whether there is proper disclosure of all material facts in a securities offering, and second, when are these businesses pursuing opportunities provided by Congressional legislation operating illegally as unregistered broker-dealers.

EB-5 has been around for many years, whereas much of the JOBS Act rules including Reg A and Reg CF were finalized in 2015. Thus, a review of SEC enforcement actions taken in EB-5 serves as a useful roadmap as to what one can expect from the SEC in the JOBS Act space.

While this article focuses on SEC action, the EB-5 and JOBS Act industries should well understand FINRA and the state regulators are also in a deep dive to learn and identify abuses in these industries. These regulators will also bring enforcement actions to protect investors who are harmed or defrauded by unlawful conduct. Entrepreneurs beware: errors of judgment may result in allegations of fraud or other wrongdoing. Regulatory action to remedy perceived wrongs may be in the form of a criminal, civil or administrative actions. Regardless, all of it is serious, and so it is helpful to have a roadmap.

While this article focuses on SEC action, the EB-5 and JOBS Act industries should well understand FINRA and the state regulators are also in a deep dive to learn and identify abuses in these industries. These regulators will also bring enforcement actions to protect investors who are harmed or defrauded by unlawful conduct. Entrepreneurs beware: errors of judgment may result in allegations of fraud or other wrongdoing. Regulatory action to remedy perceived wrongs may be in the form of a criminal, civil or administrative actions. Regardless, all of it is serious, and so it is helpful to have a roadmap.

In his recent testimony to the United States Senate Committee on the Judiciary on February 2, 2016, Stephen Cohen, Associate Director of the SEC Division of Enforcement, summarized SEC action involving the EB-5 industry. He also acknowledged EB-5 actions are a growing part of the SEC docket. Between February 2013 and December 2015, the SEC filed nineteen cases relating to EB-5 offerings, with almost half involving fraud allegations. Eleven of these matters reportedly involved unregistered broker-dealer activity.

The JOBS Act enforcement history is much less developed, with only one reported SEC enforcement action (discussed below). SEC Chairman Mary Jo White, however, made clear during her keynote address at the 47th Annual Securities Regulation Institute on October 28, 2015, that enforcement investigations open in the JOBS Act space concern potential fraud and unregistered broker-dealer activity, amongst other things. In essence, Chairman White’s comments made clear that the SEC has the same enforcement priorities for the JOBS Act industry as it does for EB-5.

The JOBS Act enforcement history is much less developed, with only one reported SEC enforcement action (discussed below). SEC Chairman Mary Jo White, however, made clear during her keynote address at the 47th Annual Securities Regulation Institute on October 28, 2015, that enforcement investigations open in the JOBS Act space concern potential fraud and unregistered broker-dealer activity, amongst other things. In essence, Chairman White’s comments made clear that the SEC has the same enforcement priorities for the JOBS Act industry as it does for EB-5.

As Mr. Cohen testified on February 2, 2016, the first EB-5 case was brought in February 2013 to stop a fraudulent EB-5 investment offering involving over 250 investors. In SEC v. A Chicago Convention Center, LLC, et al., 13CV982 (Feb. 6, 2013), the SEC alleged fraud concerning the efforts to build the “World’s First Zero Carbon Emission Platinum LEED certified” hotel and conference center. The defendants purportedly raised over $145 million plus another 11 million in administrative fees through false representations including that all necessary permits and approvals were obtained to construct the project, that several major hotel projects had signed on to the project, and that defendants would contribute land to the project worth $177 million. The SEC obtained emergency relief and a court order led to the return of $145 million to injured investors, and the perpetrator was criminally indicted in an action prosecuted by the U.S. Attorney, Northern District of Illinois.

Later, on June 23, 2015, the SEC settled its first stand-alone (no fraud) unregistered broker-dealer case charging two firms involved in handling investments for more than 150 EB-5 investors. In the Matter of Ireeco, LLC and Ireeco Limited, Securities Exchange Act of 1934 Release No. 75268, Administrative Proceeding File No. 3-16647 (June 23, 2015), the defendants reportedly used their website to solicit EB-5 investors promising to help investors choose the right regional center to invest their funds. Rather, the defendants allegedly directed most EB-5 investors to the same handful of regional centers, and ones that paid them a commission of approximately $35,000 per investor once a conditional green card was approved. Notably, neither firm was registered as a broker-dealer although their activities clearly required same.

Later, on June 23, 2015, the SEC settled its first stand-alone (no fraud) unregistered broker-dealer case charging two firms involved in handling investments for more than 150 EB-5 investors. In the Matter of Ireeco, LLC and Ireeco Limited, Securities Exchange Act of 1934 Release No. 75268, Administrative Proceeding File No. 3-16647 (June 23, 2015), the defendants reportedly used their website to solicit EB-5 investors promising to help investors choose the right regional center to invest their funds. Rather, the defendants allegedly directed most EB-5 investors to the same handful of regional centers, and ones that paid them a commission of approximately $35,000 per investor once a conditional green card was approved. Notably, neither firm was registered as a broker-dealer although their activities clearly required same.

Later, at the end of 2015, the SEC instituted ten settled administrative proceedings against seven individuals (six of whom were lawyers) and three law firms, and also announced a litigated district court action against a lawyer and his law firm alleging fraud. These cases were the first to bring charges against lawyers and law firms for acting as unregistered brokers in the EB-5 space. In addition to charging legal fees, the lawyers purportedly received commissions for selling EB-5 securities when they successfully sold securities to their clients. Commissions are transaction-based compensation, which has always been a clear cut indication of unregistered broker-dealer activity. In addition, the attorneys were allegedly recommending securities to their clients, acting as liaison between the investment offeror and their client (investor), and facilitating the transfer of investment funds, all without broker-dealer registration.

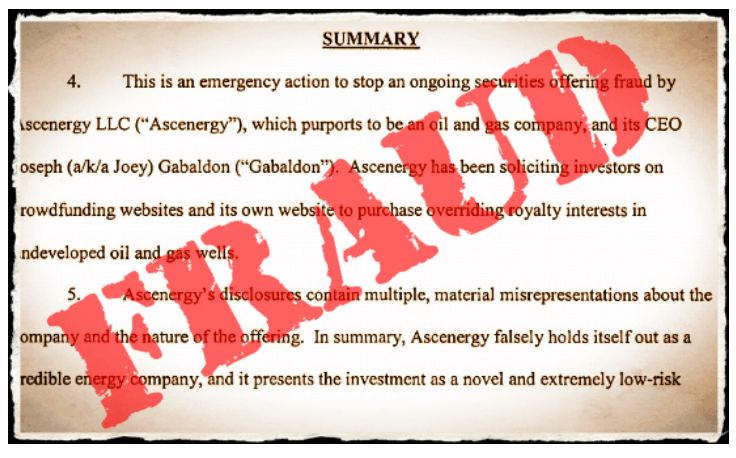

On the JOBS Act side, in late October 2015, the SEC announced as action, Securities and Exchange Commission v. Ascenergy, LLC, et al, Civil Action No. 2:15-cv-01974 (D. Nev., October 13, 2015) pursued an issuer, Las Vegas-based Ascenergy. LLC, and its CEO Joseph Gabaldon, for fraudulently raising approximately $5 million under Rule 506(c). They purportedly sold securities on their own website and on the websites of several funding platforms. Ascenergy and Gabaldon allegedly were diverting investor funds. This includes for such things like foreign travel, fast food restaurants, Apple stores and iTunes, dietary supplements and personal care products, all clearly unrelated to their oil and gas business. Also, the SEC alleged that the defendants made multiple, material misrepresentations about the company and the nature of the offering, including that Ascenergy described the offering as having “exceptionally low risk,” and an “extremely low risk profile” when, in fact, it was a high-risk investment in undeveloped and unproven wells.

On the JOBS Act side, in late October 2015, the SEC announced as action, Securities and Exchange Commission v. Ascenergy, LLC, et al, Civil Action No. 2:15-cv-01974 (D. Nev., October 13, 2015) pursued an issuer, Las Vegas-based Ascenergy. LLC, and its CEO Joseph Gabaldon, for fraudulently raising approximately $5 million under Rule 506(c). They purportedly sold securities on their own website and on the websites of several funding platforms. Ascenergy and Gabaldon allegedly were diverting investor funds. This includes for such things like foreign travel, fast food restaurants, Apple stores and iTunes, dietary supplements and personal care products, all clearly unrelated to their oil and gas business. Also, the SEC alleged that the defendants made multiple, material misrepresentations about the company and the nature of the offering, including that Ascenergy described the offering as having “exceptionally low risk,” and an “extremely low risk profile” when, in fact, it was a high-risk investment in undeveloped and unproven wells.

For those not familiar with the securities laws, the misrepresentation or omission to state all material facts may constitute fraud, and fraud allegations may be brought by criminal prosecutors, securities regulators, or plaintiff or class action attorneys. So all offerors of securities, whether under EB-5 or a JOBS Act internet offerings, must make sure their offering documents and marketing materials comport to the requirements of law. As is obvious, this means that the issuer cannot make misrepresentations of material fact, or omit to disclose a material fact that an investor would reasonably want to know in advance of making their investment.

If you have been in this business for a while, you already know what constitutes fraud largely depends on the facts and circumstances. The critical question is whether there is a substantial likelihood a reasonable investor would consider the fact important in deciding whether to invest their money. If so, it is a material fact that must be disclosed, and the failure to disclose it may be fraud. It is hard for entrepreneurs lacking familiarity with the securities laws to understand that not disclosing something can and will be construed to fraud in the securities industry. What makes matters worse is the significant remedies available to the government. Government may pursue criminal prosecutions or seek bars from the securities industry that prevent someone from ever selling securities again.

Similarly, whether someone is acting as an unregistered broker-dealer requires a review of an assortment of factors that need to be assessed and evaluated to determine whether registration is required. Section 3(a)(4)(A) of the Securities Exchange Act of 1934 generally defines a broker broadly as any person engaged in effecting transactions in securities for the accounts of others. Individuals or entities who participate in important parts of a securities transaction, including solicitation, negotiation, or execution of the transaction, or who are otherwise engaged in the business of effecting or facilitating securities transactions, may be required to register as a broker-dealer. Receiving transaction-based compensation, or compensation that is related to the outcome or size of a securities offering, is clear cut indicia of broker-dealer activity. SEC guidance here is not always clear, however, as the factors only indicate that you “may” need to be registered as a broker-dealer. Many entrepreneurs wrongly conclude that if you do not receive transaction-based compensation (basically, commissions), that this alone eliminates the broker-dealer conundrum. It does not. Even when you do not receive transaction-based compensation, if your acts are important parts of effecting a securities transaction for others, your activities still may be considered to be those of an unregistered broker-dealer and you are potentially subject to an enforcement action.

So what is an enforcement action? The SEC is a securities regulatory agency with significant enforcement powers. Its Enforcement Division recommends and initiates investigations of securities law violations. These investigations can be extremely lengthy and expensive, and the costs alone may be the death knell to any start up. The SEC Enforcement Division ultimately may recommend that the SEC bring an action in federal court or before an administrative law judge, or sometimes both, and SEC Enforcement prosecutes the case. It can also make a criminal referral to the U.S. Attorney’s office or a local prosecutor. As the SEC is the government, its resources are basically unlimited and the challenges in overcoming an enforcement action are quite substantial.

So what is an enforcement action? The SEC is a securities regulatory agency with significant enforcement powers. Its Enforcement Division recommends and initiates investigations of securities law violations. These investigations can be extremely lengthy and expensive, and the costs alone may be the death knell to any start up. The SEC Enforcement Division ultimately may recommend that the SEC bring an action in federal court or before an administrative law judge, or sometimes both, and SEC Enforcement prosecutes the case. It can also make a criminal referral to the U.S. Attorney’s office or a local prosecutor. As the SEC is the government, its resources are basically unlimited and the challenges in overcoming an enforcement action are quite substantial.

You now understand more about SEC priorities. And, this is only part of the picture. Broker-dealers and their agents are also regulated by FINRA, which has separate enforcement powers, and all the states have their own securities laws, regulators and enforcement actions. The states often bring cases to enforce their state (blue sky) laws when sales of securities are made to residents of their state. While FINRA’s enforcement powers are administrative, states while also having administrative powers in many instances also have civil and even criminal powers too. And there is nothing in the world so unpleasant as having three or four state securities regulators investigate your securities offering at the same time. I have previously participated in such efforts on the regulatory side, and am well versed in the costs and pressures it imposes on the subjects of the investigation.

You now understand more about SEC priorities. And, this is only part of the picture. Broker-dealers and their agents are also regulated by FINRA, which has separate enforcement powers, and all the states have their own securities laws, regulators and enforcement actions. The states often bring cases to enforce their state (blue sky) laws when sales of securities are made to residents of their state. While FINRA’s enforcement powers are administrative, states while also having administrative powers in many instances also have civil and even criminal powers too. And there is nothing in the world so unpleasant as having three or four state securities regulators investigate your securities offering at the same time. I have previously participated in such efforts on the regulatory side, and am well versed in the costs and pressures it imposes on the subjects of the investigation.

The offer and sale of securities is highly regulated and require the disclosure of all material facts. And regulators take their responsibilities in this area very seriously and will bring enforcement actions to remedy violations of law. So entrepreneurs beware: you are not selling automobiles, but securities. What is helpful is to understand are areas of regulatory concern. And both SEC public statements and precedent helps us to understand the areas of priority for EB-5 and the JOBS Act. With this knowledge, and some careful thought and planning, you can be well on your way to having a successful and compliant securities offering.

Scott Andersen is principal at finLawyer.com and General Counsel of FundAmerica. He has also been Deputy Regional Chief Counsel at FINRA, Enforcement Director at FINRA and the NYSE, Co-Chief of the Securities Prosecutions Unit of the NY Attorney General’s office, and Asst. Attorney General for the State of NY. He has been investigating, prosecuting and supervising criminal, civil and regulatory enforcement actions for over nineteen years. He concentrates his practice on SEC, FINRA and state regulatory defense and securities regulatory counseling.

Scott Andersen is principal at finLawyer.com and General Counsel of FundAmerica. He has also been Deputy Regional Chief Counsel at FINRA, Enforcement Director at FINRA and the NYSE, Co-Chief of the Securities Prosecutions Unit of the NY Attorney General’s office, and Asst. Attorney General for the State of NY. He has been investigating, prosecuting and supervising criminal, civil and regulatory enforcement actions for over nineteen years. He concentrates his practice on SEC, FINRA and state regulatory defense and securities regulatory counseling.

The information and materials in this article are provided for general informational purposes only and are not intended to be legal advice. The issues discussed include complicated areas of law and legal advice should be obtained from a securities attorney about your specific circumstances.