Overview of the regulatory framework

Although the Jumpstart Our Business Startups or JOBS Act was passed in April of 2012, the rules implementing Title III of that Act relating to retail investment crowdfunding have been a long time coming. They were finally promulgated on October 30, 2015, more than three years after President Obama signed the JOBS Act into law. There is much speculation around the long awaited delay but the understood rationale is that the wait was due to the sweeping transformation in the law and certain regulators’ hesitance to adopt such changes.

In brief, the new regulations allow for private businesses to raise money via online intermediaries from retail investors. It is important to understand what a radical change from traditional securities laws this concept is. Prior to this law, companies were only allowed to raise money from average investors through the IPO process or other limited exemptions (and certainly not over the internet). Otherwise, they could only raise money from high net worth individuals and institutions. The new crowdfunding laws allow companies to raise money from anyone – friends, neighbors, customers, even widows, and orphans. Of course, the devil is in the details and the final rules have 686 pages of details, the highlights of which are set forth below.

In brief, the new regulations allow for private businesses to raise money via online intermediaries from retail investors. It is important to understand what a radical change from traditional securities laws this concept is. Prior to this law, companies were only allowed to raise money from average investors through the IPO process or other limited exemptions (and certainly not over the internet). Otherwise, they could only raise money from high net worth individuals and institutions. The new crowdfunding laws allow companies to raise money from anyone – friends, neighbors, customers, even widows, and orphans. Of course, the devil is in the details and the final rules have 686 pages of details, the highlights of which are set forth below.

Issuer Limits/Requirements

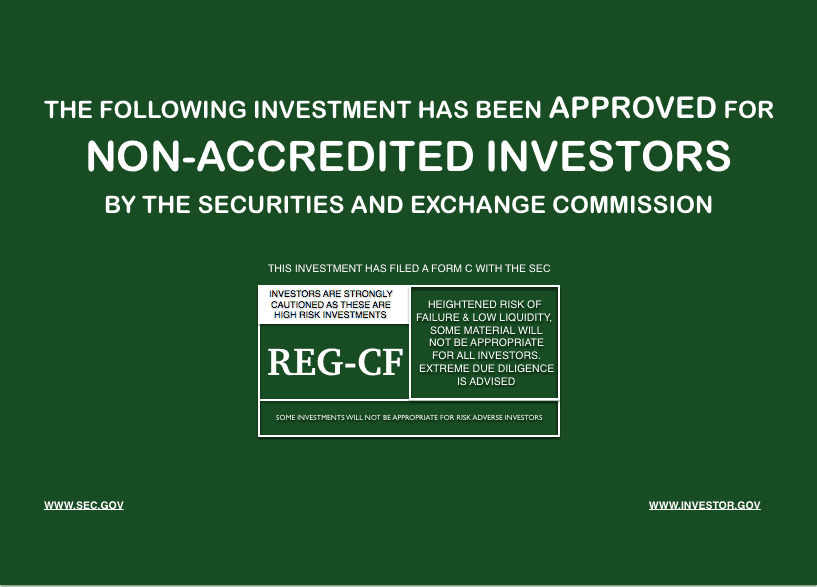

The most important restriction is that companies can only raise $1,000,000 in a rolling 12-month period using these new regulations. While a lot of people claim this will stop crowdfunding before it begins because it is simply not enough money, the fact that the majority of small business loans are under $200,000 seems to indicate that a much smaller sum is enough to get a business off the ground. Companies raising money or “issuers” must also provide a detailed disclosure document to the SEC and potential investors and they must conduct the transaction over the internet using a registered intermediary. One component of that disclosure document or “Form C” is that it must include financial statements prepared for the company in accordance with GAAP and, depending on the amount of money being raised, must have various levels of accountant review or audit. Issuers are also required to file annual updates with the SEC with respect to their business operations.

Investor Limits

Investors too are limited in the amount that they can invest in crowdfunding transactions on an annual basis. If their annual income or net worth is less than $100,000, then they can only invest the greater of $2,000 or 5% of their annual income or net worth (whichever is less) on an annual basis in crowdfunding investments. If their income and net worth is $100,000 or more, then they can invest 10% of their income or net worth (whichever is less) up to a maximum $100,000 in crowdfunding investments on an annual basis.

Investors too are limited in the amount that they can invest in crowdfunding transactions on an annual basis. If their annual income or net worth is less than $100,000, then they can only invest the greater of $2,000 or 5% of their annual income or net worth (whichever is less) on an annual basis in crowdfunding investments. If their income and net worth is $100,000 or more, then they can invest 10% of their income or net worth (whichever is less) up to a maximum $100,000 in crowdfunding investments on an annual basis.

Intermediaries

Intermediaries are the online platforms where the transactions will actually be conducted. Issuers must use an SEC and FINRA registered intermediary to conduct their deals. The intermediaries have a multitude of regulations that apply to them, pursuant to the SEC and FINRA registration, but importantly they are required to provide educational information to investors to explain the investment process and risks involved, provide a communication channel among investors and between investors and issuers and assist the issuer in conducting the mechanics of the transaction. They must also perform a preliminary diligence or gatekeeper function in an attempt to reduce the risk of fraud.

Views on Title III Crowdfunding’s place as a fundraising tool in the startup ecosystem (what types of companies are most likely to use Title III)

Title III crowdfunding is not for every company seeking financing. In fact, companies that can raise funds using less regulated means should do so. However, Title III crowdfunding opens up financing opportunities for many types of businesses that have traditionally been denied other means of capital. In addition, there are certain business types that lend themselves to the medium of crowdfunding and are more likely to be successful using this strategy.

Consumer Products Companies

One such type of business is a consumer-facing company that has a passionate and preexisting user base. Crowdfunding will allow these companies to leverage each and every satisfied customer, and convert them into an investor. This could have great appeal for “treats, potions and lotions” as I call them. These are products that people are passionate about, that they use frequently and that they want to promote and participate with in the brand awareness. Now instead of just purchasing and using your favorite organic moisturizer or eating your favorite all natural fruit snack, you can invest, become a part of the team and a brand champion. This will be extremely valuable to companies who have already done a great job of building brand loyalty and fervor around their products. Companies will simply be able to reach out using social media to inform their customer base that they now have the opportunity to invest in the company. This is truly a “never before” opportunity. Even before the securities laws, which restrict selling to unaccredited investors, because the ability to connect instantly with so many customers and potential investors was not possible, investment on this scale is truly unprecedented. Previously, in order to invest in private companies, investors primarily had to be accredited investors (high net worth individuals), but with Title III crowdfunding, anyone is eligible to be an investor, which opens up every single customer to being a potential financier.

Affinity Companies

Another related group of businesses are those with affinity products that have an almost cultish following built in. These companies include certain exercise regimes (think SoulCycle), health products, video games or game series, niche media (like campy horror films) and breweries and distilleries. These companies and products draw in a passionately loyal following who are quite likely to want to invest in something they believe in alongside the founders or creators. In addition, the online medium of crowdfunding will allow for the communication of the opportunity in a way that resonates with the potential investor. In many ways, the medium is the message. There is a coolness and anti-establishment factor to this type of financing which has an appeal to certain types of companies and their respective customers. The followers of these companies may jump at the opportunity to be an “insider” or “team member” of the company and this stronger sense of community and longer-term view may provide more than just cash to the company in the future.

Local Brick and Mortar Businesses

Another type of business that could get a revitalization from crowdfunding are the local brick and mortar businesses, specifically, restaurants, coffee shops, beauty shops, etc. These are places with a strong local appeal that again, have a loyal customer base, which can be converted into investors. In addition to investing in a product or service that they appreciate, the investor is investing in his or her community to ensure that reputable establishments remain a part of the local fabric. This has multiple benefits including giving investors a sense of ownership in their communities even at low investment amounts. Crowdfunding could also fill the void left by the community banks, which were the traditional sources of capital for these types of businesses. In the wake of bank consolidation and the Dodd-Frank capital requirements, those traditional lenders have dried up, leaving small, local, low-growth business with few financing alternatives. Large banks have not found these low-dollar loan amounts to be profitable and venture capital firms have no interest in the low-growth profile of these local operations.

Another type of business that could get a revitalization from crowdfunding are the local brick and mortar businesses, specifically, restaurants, coffee shops, beauty shops, etc. These are places with a strong local appeal that again, have a loyal customer base, which can be converted into investors. In addition to investing in a product or service that they appreciate, the investor is investing in his or her community to ensure that reputable establishments remain a part of the local fabric. This has multiple benefits including giving investors a sense of ownership in their communities even at low investment amounts. Crowdfunding could also fill the void left by the community banks, which were the traditional sources of capital for these types of businesses. In the wake of bank consolidation and the Dodd-Frank capital requirements, those traditional lenders have dried up, leaving small, local, low-growth business with few financing alternatives. Large banks have not found these low-dollar loan amounts to be profitable and venture capital firms have no interest in the low-growth profile of these local operations.

Women and Minority Owned Businesses

Speaking of traditional capital sources, there is no mystery that traditional financing sources have a typical racial and gender profile. It is also no secret (and statistically proven) that people tend to invest in and lend to people that look like themselves and have similar backgrounds. Only 7% of venture capital principals are women, and I think we can all agree about the demographics of the banking industry. This has left women and minority-owned businesses with few places to turn for financing. In addition, some of the traditional qualifiers such as individual wealth, uninterrupted employment history and certain levels of education have prevented women and minorities from “qualifying” for traditional sources of capital, such as small business loans, based on a fixed criteria. By simply broadening the gender and racial makeup of potential investors, which crowdfunding does, opportunities for women and minority-owned business will increase. By expanding the pool of individuals who might be able to identify with you or your business you will increase the chances of finding financing. In addition, the medium of crowdfunding allows women and minorities to leverage their skills and assets, which are not valued by the traditional financing criteria. Those assets are their social networks and brand equity, which can be utilized to convert customers and fans into investors and partners.

Speaking of traditional capital sources, there is no mystery that traditional financing sources have a typical racial and gender profile. It is also no secret (and statistically proven) that people tend to invest in and lend to people that look like themselves and have similar backgrounds. Only 7% of venture capital principals are women, and I think we can all agree about the demographics of the banking industry. This has left women and minority-owned businesses with few places to turn for financing. In addition, some of the traditional qualifiers such as individual wealth, uninterrupted employment history and certain levels of education have prevented women and minorities from “qualifying” for traditional sources of capital, such as small business loans, based on a fixed criteria. By simply broadening the gender and racial makeup of potential investors, which crowdfunding does, opportunities for women and minority-owned business will increase. By expanding the pool of individuals who might be able to identify with you or your business you will increase the chances of finding financing. In addition, the medium of crowdfunding allows women and minorities to leverage their skills and assets, which are not valued by the traditional financing criteria. Those assets are their social networks and brand equity, which can be utilized to convert customers and fans into investors and partners.

Businesses in the Middle of the Country

Another bias that crowdfunding solves is that of geographic bias. Because venture capital firms and other institutional investors are concentrated on the coasts of the United States for the most part, companies located in the middle of the country have an additional challenge of just getting in front of potential investors. They either have to expend significant resources traveling to San Francisco and/or New York or hope to get “discovered” at some regional demo day or showcase. This puts these companies at a significant disadvantage and is often an insurmountable hurdle to receiving financing. Keep in mind there are likely legitimate reasons for such companies to be located where they are, such as proximity to research facilities, lower cost of overhead and labor, regional customer bases, etc. Crowdfunding and the internet solve this geography problem by bringing everyone together virtually. Investments are presented and made online, so no need for in-person meetings. Meetings, presentations and chats are held on the online platform and available to all potential investors. Access is the name of the game and neither investors nor issuers are limited to a select few. This could have a profound effect on certain capital starved areas of our country – think about places like Michigan and Mississippi. These are areas where there are passionate supporters throughout the United States who until now have lacked the medium to invest in those areas important to them. Now businesses in those areas have the opportunity to reach out to the diaspora of potential investors across the country with roots or ties to the area and additionally simply to people who are passionate about their business regardless of where they live.

Another bias that crowdfunding solves is that of geographic bias. Because venture capital firms and other institutional investors are concentrated on the coasts of the United States for the most part, companies located in the middle of the country have an additional challenge of just getting in front of potential investors. They either have to expend significant resources traveling to San Francisco and/or New York or hope to get “discovered” at some regional demo day or showcase. This puts these companies at a significant disadvantage and is often an insurmountable hurdle to receiving financing. Keep in mind there are likely legitimate reasons for such companies to be located where they are, such as proximity to research facilities, lower cost of overhead and labor, regional customer bases, etc. Crowdfunding and the internet solve this geography problem by bringing everyone together virtually. Investments are presented and made online, so no need for in-person meetings. Meetings, presentations and chats are held on the online platform and available to all potential investors. Access is the name of the game and neither investors nor issuers are limited to a select few. This could have a profound effect on certain capital starved areas of our country – think about places like Michigan and Mississippi. These are areas where there are passionate supporters throughout the United States who until now have lacked the medium to invest in those areas important to them. Now businesses in those areas have the opportunity to reach out to the diaspora of potential investors across the country with roots or ties to the area and additionally simply to people who are passionate about their business regardless of where they live.

The Future of Title III Crowdfunding

“Whimper Not a Bang”

The Title III crowdfunding industry will not start with floods of new issuers pouring forth, but will instead begin with several highly vetted potential deals. Once proven as a viable option, more companies will use the channel and more investors will be attracted to the opportunity.

Steady Growth

I predict steady yet measurable growth over the first two years similar to the marketplace lending industry when it began. After several successes and pending the absence of a major fraud, I foresee new legislation easing some of the burdens of crowdfunding and allowing for a more robust industry.

Need for Education

The most vital thing for crowdfunding is education of both the investors and the issuers. People need to understand the pros and cons of this as an investment and as a financing alternative. The vast majority of Americans have no idea what investment crowdfunding is, and that needs to change if this industry has any chance of survival.

The Unknown

The most important insight I have, however, is that the problems people are projecting are not the problems that will impair the industry. All of the concerns over disclosures, cap tables, investment limits, etc. will be, and many have been, solved. The real problems with this new industry and set of regulations are unknown to us and will only be uncovered in practice. We must do our best to anticipate these challenges and remain alert to identify them when they do materialize.

Thomson Reuters Practical Law is collaborating with Crowdfund Insider on a series of articles about the recent regulatory changes in the crowdfunding industry. The themes include JOBS Act Title III overview, global regulatory framework, and future regulatory improvements for existing crowdfunding regimes. The views expressed by the authors of these articles do not necessarily represent the views of Thomson Reuters nor any of its affiliates.

Georgia P. Quinn is a Senior Contributor for Crowdfund Insider. She is also the CEO and co-founder of iDisclose, an adaptive web-based application that enables entrepreneurs to prepare customized institutional grade private placement documents for a fraction of the time and cost. Georgia also serves as of counsel at a leading law firm in crowdfunding, Ellenoff, Grossman & Schole, specializing in facilitating financial transactions and compliance with JOBS Act regulations.

Georgia P. Quinn is a Senior Contributor for Crowdfund Insider. She is also the CEO and co-founder of iDisclose, an adaptive web-based application that enables entrepreneurs to prepare customized institutional grade private placement documents for a fraction of the time and cost. Georgia also serves as of counsel at a leading law firm in crowdfunding, Ellenoff, Grossman & Schole, specializing in facilitating financial transactions and compliance with JOBS Act regulations.