In 2011, an average of 8,000 small and micro businesses were denied funding each day from traditional banks. This statement is not from some fanatical Fintech entrepreneur but our current Secretary of the Treasury, Jack Lew. It is this profound gap between demand, and supply, that has fueled the rapid growth of online non-bank finance. Ironically during the financial crises, the sector of the economy that needed credit the most, and could have helped pull the country out of recession, were denied credit by banks required to shore up their balance sheets at the behest of federal authorities. Necessity is the mother of invention, and as old banks stumbled, a legion of agile Fintech Innovators moved quickly to provide a superior service at a better cost. These new financial firms also regularly brought with them a new commitment to transparency moving away from the traditional banking shadows.

Jackson Mueller, from the Milken Institute, Center for Financial Markets, has authored a document entitled The U.S. Online, Non-Bank Finance Landscape. Mueller profiled over 70 online, non-bank finance platforms to highlight who these platforms are, how do they operate and what types of credit products do they offer. Mueller points to the massive credit gap that can “cannot be solved absent innovative new business models.” Yet online lending is going through a period of challenges on multiple fronts.

Mueller accurately states;

“As regulatory authorities and policymakers continue to examine the online, non-bank financing space, it is vital that they take the time to understand the diversity of the industry.”

Vital is the key word here as both consumers and SMEs benefit from streamlined access to credit today. Online lending is challenging traditional banking firms and, as one would expect, they are beginning to fight back on multiple fronts.

The Mueller document is the most comprehensive tally of marketplace/P2P/ online lenders we have seen to date. Platform intent is broadly consistent but channels, methodology and strategy are becoming highly differentiated. Innovation is dearly needed in the financial services sector. Online lending has experienced a doubling of “loan origination each year since 2010 and may have the potential to generate nearly half a trillion dollars in loan value globally by the end of this decade.”

The Mueller document is the most comprehensive tally of marketplace/P2P/ online lenders we have seen to date. Platform intent is broadly consistent but channels, methodology and strategy are becoming highly differentiated. Innovation is dearly needed in the financial services sector. Online lending has experienced a doubling of “loan origination each year since 2010 and may have the potential to generate nearly half a trillion dollars in loan value globally by the end of this decade.”

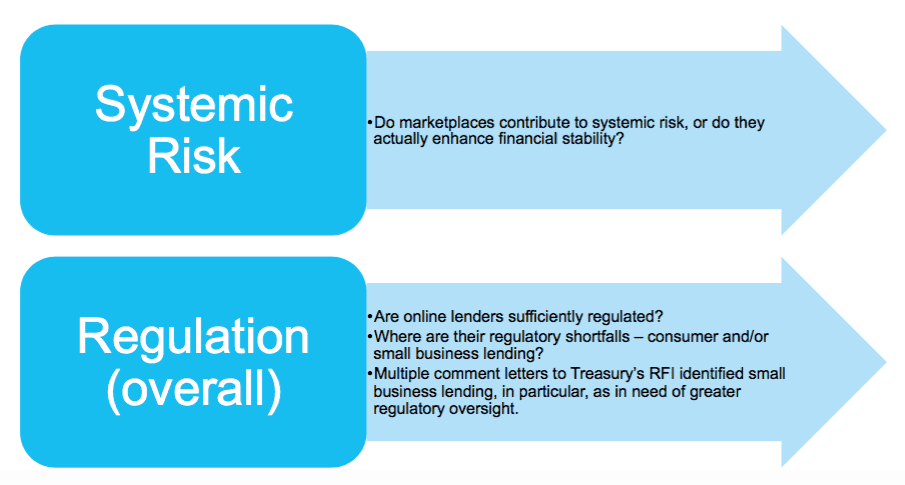

For any individual engaged in securities/banking regulation or policy-makers interested in this sector of finance, this is a must-read report. The two biggest questions facing the online lending industry are queries regarding systemic risk and the potential for ham-fisted regulation. One can better tackle these questions when you better know the platforms.