The Belgian Law of 18 December 2016 on crowdfunding entered into full force yesterday. The crowdfunding law creates a specific status for equity and debt crowdfunding platforms (referred to as “alternative financing platforms”) and prescribes operating requirements for both alternative financing platforms and regulated entities (credit institutions and investment firms) that engage in alternative financing activities. Rewards and donation-based platforms are not within the scope of this law, according to the release.

The Belgian Law of 18 December 2016 on crowdfunding entered into full force yesterday. The crowdfunding law creates a specific status for equity and debt crowdfunding platforms (referred to as “alternative financing platforms”) and prescribes operating requirements for both alternative financing platforms and regulated entities (credit institutions and investment firms) that engage in alternative financing activities. Rewards and donation-based platforms are not within the scope of this law, according to the release.

The new crowdfunding law also modifies existing tax legislation in order to render effective the various tax benefits for investments in startup companies, through licensed crowdfunding platforms that were already available for direct investments in startup companies. The new law seeks to accommodate a light touch crowdfunding regime with the need to protect investors.

The law creates a specific status for alternative financing platforms and subjects these to initial authorization and operating requirements under the supervision of the Belgian financial regulator, the Financial Services and Markets Authority (FSMA). Prior to engaging in alternative financing activities, alternative financing platforms must obtain a license (authorization) from the FSMA. For this purpose, they must inter alia:

The law creates a specific status for alternative financing platforms and subjects these to initial authorization and operating requirements under the supervision of the Belgian financial regulator, the Financial Services and Markets Authority (FSMA). Prior to engaging in alternative financing activities, alternative financing platforms must obtain a license (authorization) from the FSMA. For this purpose, they must inter alia:

- adopt the form of a commercial company;

- have their management based in Belgium (except for foreign companies in the European Economic Area);

- have persons exercising control with good repute and sufficiently skilled management; and

- take out appropriate insurance to cover their professional liability.

Operating requirements require alternative financing platforms to notify the FSMA of all changes to the control and/or management of the company. Apart from providing investment advice and executing client orders, alternative financing platforms are not authorized to provide any investment services, or to hold or receive funds or financial products belonging to their clients.

The new law also prescribes “MiFID-light” operating rules setting out the usual professional duties, information requirements, procedures on conflicts of interest and appropriateness tests. The new crowdfunding law provides for an exemption from the obligation to publish a prospectus for public offerings through an alternative financing platform for less than EUR 300,000 with a maximum of EUR 5,000 per individual investor.

The new law also prescribes “MiFID-light” operating rules setting out the usual professional duties, information requirements, procedures on conflicts of interest and appropriateness tests. The new crowdfunding law provides for an exemption from the obligation to publish a prospectus for public offerings through an alternative financing platform for less than EUR 300,000 with a maximum of EUR 5,000 per individual investor.

With regard to tax benefits, Belgian individual taxpayers now benefit from a tax reduction for investments made in equity in certain startup companies and from an exemption from the 30 percent withholding tax on interest payments on loans made to certain startup companies.

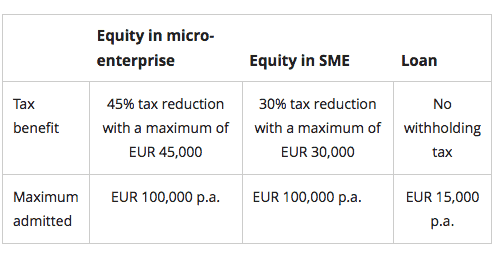

Prior to the entry into force of the crowdfunding law, the tax benefits were available only to direct investments in startup companies, because alternative financing platforms were not legally recognized, according to the release. With the creation of a regulatory framework for such platforms, the tax benefits now also apply to investments in a startup company through licensed alternative financing platforms. The tax benefits are also available to investments in or loans to alternative financing platforms, to the extent that these qualify as startup companies. Tax benefits for investments or loans in startups through alternative financing platforms are as follows:

Prior to the entry into force of the crowdfunding law, the tax benefits were available only to direct investments in startup companies, because alternative financing platforms were not legally recognized, according to the release. With the creation of a regulatory framework for such platforms, the tax benefits now also apply to investments in a startup company through licensed alternative financing platforms. The tax benefits are also available to investments in or loans to alternative financing platforms, to the extent that these qualify as startup companies. Tax benefits for investments or loans in startups through alternative financing platforms are as follows:

The new law provides for a transitional period during which existing alternative financing platforms can continue to engage in investment activities without the prior authorization of the FSMA. Within a period of two months starting from the entry into force of the law, these platforms have to notify the FSMA of their activities. These platforms are authorized to temporarily engage in alternative financing activities and have to file for authorization within four months.