As the crypto markets have evolved rapidly during the last year and institutional investors (like Arca Funds) have begun to invest, fitting into the existing financial services framework has proven difficult. The primary debate around legacy intermediary systems and how they relate to real money (institutional investors) centers around custody.

What is Custody

In order to understand the friction involved with fitting current custody requirements with crypto-assets, we need to explore custody in traditional finance.

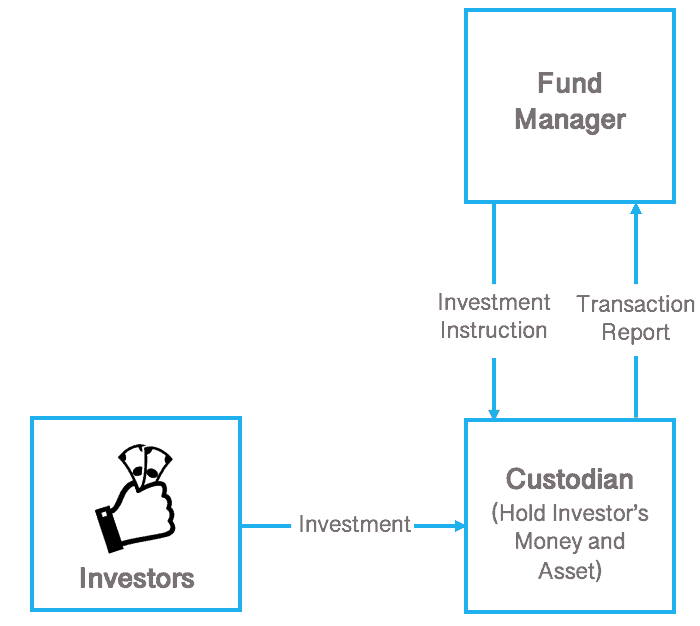

When investing and managing funds for customers, SEC-registered investment advisers (i.e. funds) are required to custody these cash and security assets with third-parties known as “Qualified Custodians.”

These custodians meet certain criteria set out by federal and state law, and provide a layer of protection for customers by preventing fraud and misappropriation of funds. Traditionally, custodians are responsible for the storage, record keeping, and transfer of securities.

In addition, they are responsible for verifying to investors, through account statements, assets in their possession. In a sense, the investment advisers are only making the investment decision and not actually handling any of the assets involved in transactions.

Flow of Assets in Traditional Financial Services

Traditional qualified custodians include recognizable firms such as JP Morgan, State Street, Mitsubishi, BNY Mellon, and CitiGroup.

Why is Custody Important

Early in my asset management career, I was responsible for private equity and 3rd party investments for a handful of life insurance companies. Not only did I initially analyze investments, I maintained an expected return and markdowns of those investments.

I was so nervous about maintaining a sizable $3 billion book at the time, that I would compare the monthly custodian statements to the values that the 3rd party managers provided. I was the only person I was aware of that regularly performed a full audit of the statements, and my colleagues thought I was a bit nuts.

I was so nervous about maintaining a sizable $3 billion book at the time, that I would compare the monthly custodian statements to the values that the 3rd party managers provided. I was the only person I was aware of that regularly performed a full audit of the statements, and my colleagues thought I was a bit nuts.

In 2009, Madoff pleaded guilty and the details of the case came out, the list of institutions and family offices that lost money appeared. I thought to myself, if the advisor or portfolio manager who was responsible for just one of those investor groups had compared the custodian statements to Madoff’s statements, in any period over the prior 10 years, they would have seen the fraud. Third party custody serves a real purpose.

Why Custody is Different in Crypto

Blockchains offer a novel feature: everyone can see all transactions taking place on the blockchain at all times (transparency).

In addition, these transactions, once entered cannot be changed (immutability). If investors could always see where their assets are, and know that information could not be manipulated, what purpose do custodians serve? The most valuable service a custodian can offer is securing private keys (which really isn’t the definition of a custodian).

Crypto-assets are not physically, or digitally, owned, they are always located on the blockchain. Ownership of assets is represented by access to public and private keys which are represented by a long string of numbers and letters. A public key is like a Twitter profile: it is publicly available, anyone can see your profile and what you tweet.

However, no one can tweet for you without a password to your account. Similar to how a password unlocks access to your Twitter account, a private key in crypto can be thought of as an “account password,” that unlocks access to digital assets.

In reality, public and private keys are a sophisticated form of cryptography that allows an asset owner to access and prove ownership of his or her cryptocurrency. Private keys act like a digital signature, which must be present to initiate a transaction. The blockchain network then confirms a transaction, using encrypted mathematical equations to match public and private keys. This process is what makes blockchain networks so secure.

A signed transaction never reveals the underlying private key with which the transaction was signed. The system is similar in concept to placing a wax seal on a document: the recipient can see the wax seal and verify the authenticity of the document, but seeing the wax seal does not provide access to the underlying sealing mechanism.

Any person in possession of a private key can sign a transaction. Knowledge of a private key is the only verification needed to spend a digital asset. Private keys are therefore the weakness in securing blockchain assets. Although no one can guess your private key (they would have a 1 in 2^256 chance), these keys are liable to accidental loss and theft. Therefore, keeping private keys secure is the primary goal of custodians.

Custody Solutions

There are three main ways to custody private keys of crypto-assets.

Exchanges: some of the more reputable digital asset exchanges provide strong security of private keys, but expose users to counter party risk.

When digital assets are stored on an exchange, users do not actually own their crypto, instead they own the right to trade or withdraw it. Assets held by exchanges are commingled and held in parent addresses, not individual addresses. This means that users are at risk of losing their assets if the exchange is hacked. As a result, it is recommended that only a minimal amount of “immediately tradable” digital assets should be held at any exchange.

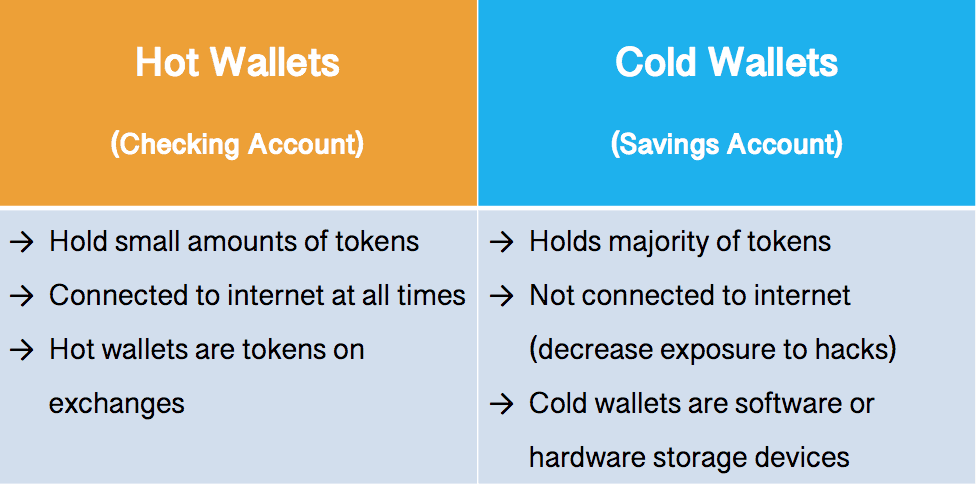

Self-Custody: this is the most common and, to date, trusted form of custody typically implemented through a combination of hot and cold wallets.

A cryptocurrency wallet is a digital wallet that stores your public and private keys. The wallet software only uses the private key to sign a transaction, it does not actually store any assets. There are a large number of wallets available, both in hardware and software format designed for consumer and institutional use. However, self-custody, is subject to human error such as loss and theft.

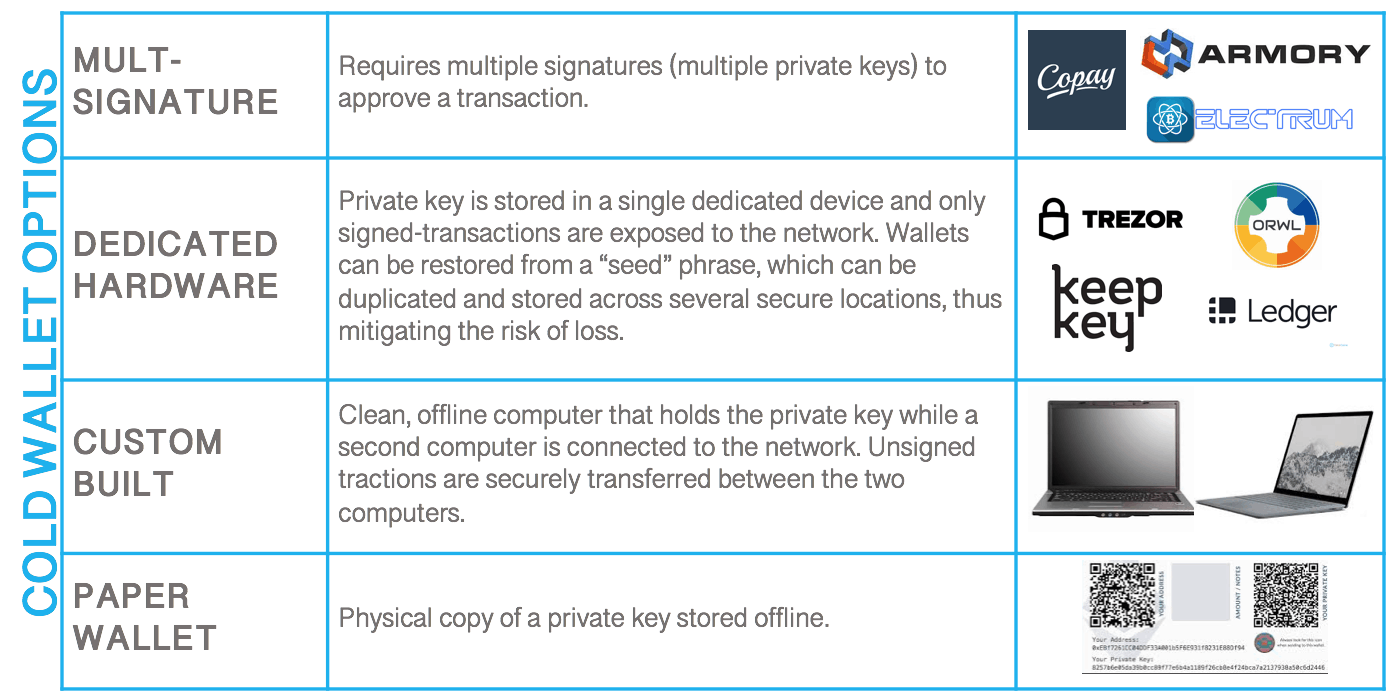

Third-Party Custodians: as the market for digital assets has developed, a few players have entered the space offering strong technology and security protocols to secure private keys. Most do not detail their security procedures, but offerings include use of 24/7 armed guards, frequently rotating locations, and multi-signature requirements for access.

Unfortunately, as these groups are not established firms, nor do most of them meet the criteria of a qualified custodian, mainstream adoption has been impeded.

However, a few new entrants to the market, such a DACC (Digital Asset Custody Company), have founders and employees that are personally established with a long history and great reputation from traditional custodians and prime brokerages, such as Morgan Stanley, JP Morgan, and Deutsche Bank.

Today’s Crypto Custodian Resources

The state of custody today is a mix of old and new players, all of whom are racing to develop and launch their product offering. There are a slew of businesses that have entered the custody space from both the exchange and independent side such as Coinbase, Gemini, Kingdom Trust, BitGo, and Digital Asset Custody Company.

In addition, established firms such as Fidelity and Northern Trust recently announced they will offer crypto custody solutions, although these services may not be available for some time. What has begun is essentially an arms race as these firms concentrate on acquiring as many customers as the crypto space matures.

As discussed, the drawbacks to exchange custody puts investors at risk of hacks. Solutions offered by players such as Coinbase have gone to great lengths to separate out their custody and exchange business, while still offering seamless interactions between the two platforms for institutional investors. We question, however, if acting as both an exchange and custodian does not present a conflict of interest for these businesses.

Third-party firms on the other hand, offer much more independence – dare we say decentralization – and neutrality from these larger parties.

BitGo, a company that started out as a multi-signature wallet solution for blockchain, recently received approval as a qualified custodian. They are the first of many custodians that will likely receive approval as the crypto ecosystem develops. However, as there are over 2000 crypto-assets freely traded today, none of these firms can custody every single asset.

With all these available options, why has institutional money not poured into the space?

One issue, besides their untested reputation, is that almost all of these firms are not qualified custodians.

If a fund is SEC-registered and manages over $150 million in assets, it must use a qualified custodian. Adding to the uncertainty, is that the SEC has not broadly ruled that crypto-assets are securities, and therefore funds do not necessarily need a qualified custodian. Although the rules may not apply for digital assets, funds – particularly larger asset managers – should always err on the side of caution.

A group of blockchain mainstays, including former Morgan Stanley executive Caitlin Long, are working with the SEC to explain the unique nature of crypto-assets; particularly, why centralized custody requirements are contra to the innovation of blockchain that removes the need for intermediaries. We believe in that innovation and the decentralization and disintermediation that it creates.

Steven McClurg is a founding partner and CIO at Arca Funds, a full service asset management firm specializing in blockchain. Prior to Arca Funds, Mr. McClurg was a Managing Director and Portfolio Manager at Guggenheim Partners. Mr. McClurg holds an MBA and MS from Pepperdine University, where he has served as a guest lecturer.

Steven McClurg is a founding partner and CIO at Arca Funds, a full service asset management firm specializing in blockchain. Prior to Arca Funds, Mr. McClurg was a Managing Director and Portfolio Manager at Guggenheim Partners. Mr. McClurg holds an MBA and MS from Pepperdine University, where he has served as a guest lecturer.

Katie Talati is Head of Research and Portfolio at Arca Funds. Ms. Talati is responsible for all research initiatives at Arca Funds, which includes fundamental research in all varieties of cryptocurrencies,  blockchain technologies, as well as broad consideration of macroeconomics and other investment vehicles. She is the first female executive investment professional for a major blockchain asset manager and is a prominent member of the Silicon Beach startup community and leader in the women in tech community. Ms. Talati holds a Series 7, 63, and 79 (she is currently not registered as a broker) and is a graduate of UCLA.

blockchain technologies, as well as broad consideration of macroeconomics and other investment vehicles. She is the first female executive investment professional for a major blockchain asset manager and is a prominent member of the Silicon Beach startup community and leader in the women in tech community. Ms. Talati holds a Series 7, 63, and 79 (she is currently not registered as a broker) and is a graduate of UCLA.

Sources

- Investor Bulletin: Custody of Your Investment Assets – SEC

- Staff Letter: Engaging on Fund Innovation and Cryptocurrency-related Holdings – SEC

- The Ultimate List of Cryptocurrency Custody Solutions – Medium

- Announcing BitGo Trust Company – Business Wire

- Coinbase Physical Vault to Secure a Virtual Currency – Wired

- Applying the Custody Rule to Cryptocurrency Holdings – Cordium

- Cryptofunds: The Tough Due Diligence Test – FinOps

- The perils of custodial trading & the promise of non-custodial trading – Underscore.VC