LendingClub (NYSE: LC), an online lender and nascent digital bank, has announced financial results for Q4 2020 and the full year ending December. According to a release, LendingClub’s adjusted net loss was $(22.1) million in the fourth quarter, compared to adjusted net income of $7.0 million the same quarter last year. During Q3 2020, LendingClub reported an adjusted net loss of $(23.1) million.

LendingClub (NYSE: LC), an online lender and nascent digital bank, has announced financial results for Q4 2020 and the full year ending December. According to a release, LendingClub’s adjusted net loss was $(22.1) million in the fourth quarter, compared to adjusted net income of $7.0 million the same quarter last year. During Q3 2020, LendingClub reported an adjusted net loss of $(23.1) million.

Loan originations in Q4 of 2020 were $912.0 million, a decrease of 70% compared to the same quarter last year. Loan originations did bounce back from Q3 2020 rising 56% sequentially. LendingClub, like most digital lenders, has struggled during the ongoing COVID-19 health crisis. Prior to the pandemic, the Fintech lender was on track to consistently profitable quarters.

Scott Sanborn, CEO of LendingClub, issued a statement on the quarter, a culmination of a tough year, saying he was proud of what they had accomplished in 2020 which ended in completing the “groundbreaking acquisition of Radius Bank.”

“Combining the award-winning digital bank with LendingClub’s leading online marketplace provides us with substantial advantages over both traditional banks and Fintech marketplace lenders,” said Sanborn. “Adding deposit capabilities builds on our tech and data advantages as it allows us to better serve our more than 3 million loyal and highly-motivated members and digitally manage their lending, spending, and savings. We are fully aligned with both our customers and shareholders to realize incremental long-term value for decades to come.”

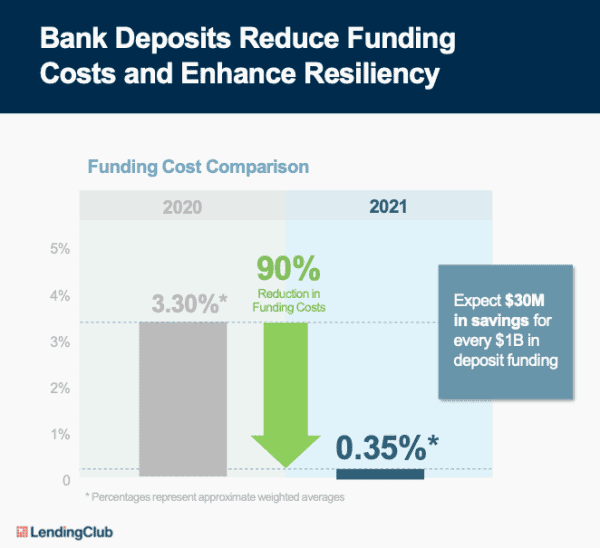

Focusing on the future, LendingClub CFO Tom Casey said the addition of bank deposits will enhance their resiliency and “unleash a new recurring revenue stream that will drive significant long-term growth once the bank is fully integrated.”

Year-over-year results primarily reflected an expected decrease in origination volume and transaction fees, and an expected reduction in net interest income, partially offset by an improvement in expenses. The change in loan origination volumes resulted in a 71% decline in transaction fees year-over-year. Lower net interest income reflected the sale of $470 million of loans in the second half of 2020 to accumulate capital in preparation for the company’s acquisition of Radius. The improvement in expenses year-over-year primarily reflected significantly lower sales and marketing expense and the company’s focus on originating loans to existing customers, which increased efficiency and resulted in lower marketing costs. The improvement in expenses also reflected proactive actions taken to improve efficiency, reduce costs and mitigate the impact of the pandemic.

Cash and cash equivalents as of December 31, 2020, totaled $525.0 million compared to $243.8 million as of December 31, 2019, and $445.2 million as of September 30, 2020.

LendingClub will host a webcast and teleconference today at 5:00 p.m. ET. A live webcast of the call will be available at http://ir.lendingclub.com under the Filings & Financials menu in Quarterly Results. Expect much of the discussion to cover the acquisition of Radius Bank.

Update: LendingClub anticipates a loss for 2021 of between $175 millin to $200 million. While providing the guidance, LendingClub said it will become profitable off the move to become a digital bank. “A bank is a thing you do. Not a place you go.” LendingClub believes it has advantages over both incumbent banks as well as Fintechs. By being unencumbered by legacy tech and high-cost branches, as well as being able to fund loans with deposits, LendingClub envisions it emerging as a profitable entity.

LendingClub said it pays around $20 million a year to partner banks in the loan origination process. As well, borrowing costs are expected to decline by 90% as deposit financed loans are far less expensive than alternatives (IE warehouse at 3.3% vs. deposits at .35%)

Asked by an analyst as to when LendingClub/Radius Bank will become profitable, the company said it was not providing long-term guidance.

“Our goal is to create a high growth, highly profitable firm.”

Let’s see how the new digital bank competes in an increasingly competitive market.