Crowdfunding May Require JOBS Act 2.0.

It started out as a noble idea. If only crowdfunding could go to the next level – from a paradigm where a multitude of individuals could join together – courtesy of the Internet – and fund a worthwhile social or civic project – to a paradigm where individuals could support a worthy commercial venture and receive, in return, not only the satisfaction of building something larger than the collective wisdom of a multitude of individuals – but also an economic stake in the commercial enterprise.

It started out as a noble idea. If only crowdfunding could go to the next level – from a paradigm where a multitude of individuals could join together – courtesy of the Internet – and fund a worthwhile social or civic project – to a paradigm where individuals could support a worthy commercial venture and receive, in return, not only the satisfaction of building something larger than the collective wisdom of a multitude of individuals – but also an economic stake in the commercial enterprise.

The only thing that stood in the way of this idea was a law borne out of another noble idea – the Securities Act of 1933 – a decades old statute intended to protect investors from themselves – by requiring a commercial enterprise to navigate a regulatory path requiring registration of the economic interests to be offered to the public. The anecdote to protecting would-be investors from their own avarice or ignorance – dozens, even hundreds, of pages of financial and non-financial information – assembled by a team of high priced lawyers and accountants.

And in 1934 Congress imposed additional layers of protection for the ostensible benefit of the investing public – extensive regulation of the persons who sought to make a living from selling these economic interests to the public.

And in 1934 Congress imposed additional layers of protection for the ostensible benefit of the investing public – extensive regulation of the persons who sought to make a living from selling these economic interests to the public.

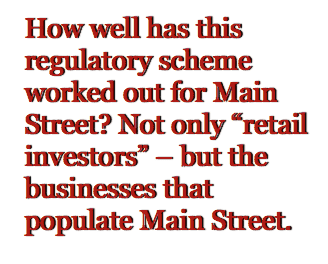

By and large, this regulatory scheme has worked well for Wall Street, albeit not without some tweaking and refinement along the way. But looking back 80 years later the question remains – how well has this regulatory scheme worked out for Main Street – not only “retail investors” – but the businesses that populate Main Street – the same businesses that house the entrepreneurial spirit, responsible for the large majority of jobs and technological innovation in this country? If the recent history of the JOBS Act of 2012, supported and signed into law by President Barack Obama, is to be the yardstick – things have not worked out very well for small business.

The Best Laid Plans . . .

What started out as a simple piece of legislation, introduced in Congress by Congressman Patrick McHenry in the fall of 2011 – soon fell prey to a number of factors – which held small business job creation and economic growth hostage to special interests, political expediency and the apparent disinterest – if not disdain – of the institution charged with protecting investors – the Securities and Exchange Commission (SEC).

What started out as a simple piece of legislation, introduced in Congress by Congressman Patrick McHenry in the fall of 2011 – soon fell prey to a number of factors – which held small business job creation and economic growth hostage to special interests, political expediency and the apparent disinterest – if not disdain – of the institution charged with protecting investors – the Securities and Exchange Commission (SEC).

What ultimately emerged as Title III of the JOBS Act, retail investment crowdfunding, was a shadow of its former self. When compared to the original bill it is now plagued with intricacies which appear likely to ultimately seed the demise of a promising vehicle for job creation for startups and small local businesses. And perhaps the biggest fly in the ointment – leaving key provisions to the uncertain rulemaking process at the SEC.

The result, nearly two years later, is obvious to all who care to look– there is virtually nothing to be shown for the efforts of Congress’ attempt to innovate –- in what was to be a promising avenue for small business capital formation. Leaving aside, momentarily, the unforgivable delay by the SEC in issuing proposed rules, what ultimately emerged from the SEC is a patchwork of proposed rules which, in the aggregate, threaten to kill retail investment crowdfunding, and along with it – the potential to rekindle the entrepreneurial spirit desperately needed by this country.

The result, nearly two years later, is obvious to all who care to look– there is virtually nothing to be shown for the efforts of Congress’ attempt to innovate –- in what was to be a promising avenue for small business capital formation. Leaving aside, momentarily, the unforgivable delay by the SEC in issuing proposed rules, what ultimately emerged from the SEC is a patchwork of proposed rules which, in the aggregate, threaten to kill retail investment crowdfunding, and along with it – the potential to rekindle the entrepreneurial spirit desperately needed by this country.

The Six Deadly Sins? Four Industry Killers?

On January 9, 2014, I laid out six major flaws in the SEC’s proposed crowdfunding rules – each of which I argued threatened to kill the crowdfunding industry before it could get off the ground. And on February 9, two of the innovators behind the original crowdfunding legislation, Sherwood Neiss and Jason Best, came up with three of the same flaws – as well as a fourth proposal intended to enhance the crowdfunding process – the ability of a company to “test the waters” for interest in their offering before a startup or small business sunk significant dollars into the cost of conducting the crowdfunded offering.

On January 9, 2014, I laid out six major flaws in the SEC’s proposed crowdfunding rules – each of which I argued threatened to kill the crowdfunding industry before it could get off the ground. And on February 9, two of the innovators behind the original crowdfunding legislation, Sherwood Neiss and Jason Best, came up with three of the same flaws – as well as a fourth proposal intended to enhance the crowdfunding process – the ability of a company to “test the waters” for interest in their offering before a startup or small business sunk significant dollars into the cost of conducting the crowdfunded offering.

What I had labeled on January 9 as six flawed proposed rules which threatened to be “industry killers” if enacted, Neiss and Best later similarly cautioned: “crowdfunding may be dead on arrival” without their four proposed fixes.

Not to leave any stone unturned, the six deadly sins were also presented by me, in greater detail, to the SEC in a comment letter which I submitted on February 11, and supplemented by a second comment letter on February 20.

The Path Forward

One can only speculate as to why the SEC chose, in proposed rule after proposed rule, to either not exercise the discretion which Congress entrusted to it – or to exercise its discretion in a way which would ensure the certain demise of the investment crowdfunding market. Given the track record of the SEC thus far in implementing Title III, it would be imprudent to rely on mere speculation as to the outcome of final rulemaking– unless one is indifferent to the fate of retail investment crowdfunding and the potential it holds for small business and the economy.

One can only speculate as to why the SEC chose, in proposed rule after proposed rule, to either not exercise the discretion which Congress entrusted to it – or to exercise its discretion in a way which would ensure the certain demise of the investment crowdfunding market. Given the track record of the SEC thus far in implementing Title III, it would be imprudent to rely on mere speculation as to the outcome of final rulemaking– unless one is indifferent to the fate of retail investment crowdfunding and the potential it holds for small business and the economy.

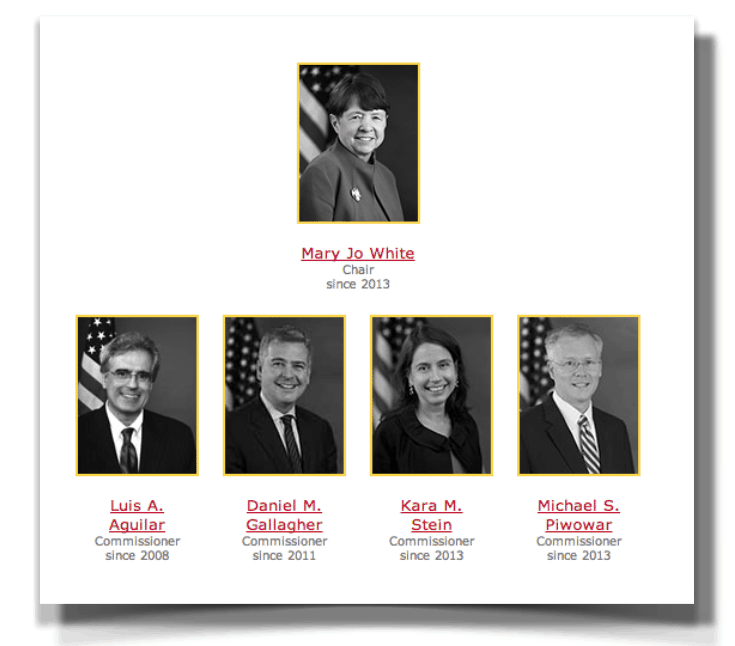

Unless Congress wants to roll the dice one more time, and rely on the SEC to fix the unworkable mess squarely in its lap – in final rules – at some indeterminate time – perhaps Congress ought to consider revisiting Title III, with the benefit of hindsight, and fine tune the Title III rules – lest the “enthusiasm” which SEC Chair White recently noted from the public for Title III in a recent public statement, turn the crowd into an angry mob of voters in the fall of 2014.

Alternatively, Congress could take a “wait and see” attitude, and allow the rulemaking process to continue to conclusion at some indeterminate time.

The Fly in the JOBS Act Ointment – Implementation Left by Congress to the SEC

Though there is certainly plenty of blame to go around for the quagmire that Title III has become, the reality is that this mess was not only avoidable by Congress – it was foreseeable.

Though there is certainly plenty of blame to go around for the quagmire that Title III has become, the reality is that this mess was not only avoidable by Congress – it was foreseeable.

Case in point – Wisconsin – which in November 2013 enacted its own local crowdfunding statute – to invigorate its local businesses and its local economy. It is no coincidence that the Wisconsin crowdfunding legislation, drafted by Wisconsin residents, some of whom in an earlier life made their living inside the Washington Beltway, left nothing to the discretion of its state securities administrator by way of rulemaking. Rather, the Wisconsin crowdfunding statute is self-implementing.

Unless Congress wants to continue to roll the dice, after the SEC has already shown most of its cards in the Title III rulemaking, the path forward is clear: It is time for Congress to revisit what it started in April 2012 – and to allow Title III to become a working market – through a much needed, and long overdue, JOBS Act 2.0.

And if it is indeed necessary for Congress to go back to the drawing board to make Title III a reality, it ought to add a couple of other points to the “six deadly sins,” now that it has the benefit of hindsight.

Eliminate the Requirement of Independently Reviewed Financial Statements.

This is a statutory requirement which never made any sense for a startup seeking to raise up to $500,000. Basic financial statements, certified by the company’s management, ought to work just fine. The cost of an independent review will quickly outweigh the potential benefit of a successful crowdfunded offering of under $500,000. Apparently, the only ones currently with a different view are the outside accountants who hope to benefit from a new source of revenue.

Allow Regulation A to Function as a Vehicle for “CrowdfundingPlus” – For Raises Under $5 million under Title IV of the JOBS Act.

Title IV of the JOBS Act was intended to revitalize an historic relic, Regulation A, which in theory would allow companies to raise up to $5 million in a “mini-IPO” through a short form SEC registration review process. Among its advantages:

- No need for expensive audited financial statements – less expensive “reviewed” financial statements would suffice.

- An offering that could be conducted with or without an Internet “portal”, with or without licensed broker-dealers – with unlimited use of social media and general solicitation.

- The ability to “test the waters” by soliciting interest in the offering before a company sunk thousands of dollars into offering costs – including high priced accountants and securities attorneys.

- Freely tradeable securities the moment they were sold to investors.

- No burdensome annual disclosure.

In sum, Title IV could have been, and still could be, the perfect vehicle for “CrowdfundingPlus”, raises up to $5 million under Regulation A. The only fly in the ointment – time consuming and expensive duplicate registration at the state level – so called “blue sky merit review” – which allows a state to block an offering if it determines that it is necessary to protect retail investors.

In sum, Title IV could have been, and still could be, the perfect vehicle for “CrowdfundingPlus”, raises up to $5 million under Regulation A. The only fly in the ointment – time consuming and expensive duplicate registration at the state level – so called “blue sky merit review” – which allows a state to block an offering if it determines that it is necessary to protect retail investors.

Instead, in 2012 Congress chose to make lemons out of lemonade. It handed Wall Street an early, oversized Christmas present – raising the limits for Regulation A to $50 million – but doing nothing to solve the underlying problem with the original Regulation A – a problem known to all – by pre-empting state blue sky regulation for offerings under $5 million. Apparently, in the final legislative process, small business was thrown under the bus in the interest of political expediency – bowing to pressure from well organized state securities regulators – apparently more interested in preserving jobs (theirs) – effectively with absolute veto power over federal regulators in the Regulation A registration process- than in creating new jobs.

Though the Commission has recently indicated its willingness, through rulemaking, to consider exempting Regulation A offerings under $5 million from state blue sky review, by soliciting comments on this issue in proposed Title IV rules issued in December 2013, it has yet to actually propose a rule to this effect – as it has already done for raises over $5 million up to $50 million. And if history is to be any guide, absent Congressional intervention, it is more than likely that this SEC “request for comment” to exempt offerings under $5 million from state blue sky review will wind up as a bargaining chip left on the table to assuage the entrenched interests of state securities administrators – which is precisely what happened to Title IV in the JOBS Act legislative process.

Though the Commission has recently indicated its willingness, through rulemaking, to consider exempting Regulation A offerings under $5 million from state blue sky review, by soliciting comments on this issue in proposed Title IV rules issued in December 2013, it has yet to actually propose a rule to this effect – as it has already done for raises over $5 million up to $50 million. And if history is to be any guide, absent Congressional intervention, it is more than likely that this SEC “request for comment” to exempt offerings under $5 million from state blue sky review will wind up as a bargaining chip left on the table to assuage the entrenched interests of state securities administrators – which is precisely what happened to Title IV in the JOBS Act legislative process.

It is not too late for Congress to act – by exempting Regulation A raises under $5 million (designated by the SEC as so-called “Tier I” offerings) – and eliminating the caps on the number of investors who can participate in an offering without triggering the cumbersome ongoing reporting requirements required of large public companies. Ongoing annual disclosure, for these Tier 1 raises, coupled with periodic reporting of specified material events, would certainly provide needed transparency to investors, but without burdening small businesses with expenses from filing more frequent detailed reports it can ill afford.

The result – Tier 1 of Regulation A, with some tweaking by Congress to mimic provisions already in Title III (state blue sky pre-emption and no limits on the number of investors) presents the perfect vehicle for larger dollar crowdfunded offerings – where any cost or complexity, such as the disclosure burden embedded in Title III, would be more than outweighed by the amount of the dollars being raised. And investors would be amply protected by a “light” SEC review process and size-appropriate ongoing disclosure following a successful raise.

However, whether “CrowdfundingPlus” will happen without an act of Congress is unlikely, given the SEC’s track record with Title III rulemaking and the proposed Title IV rules, is at best, left to speculation.

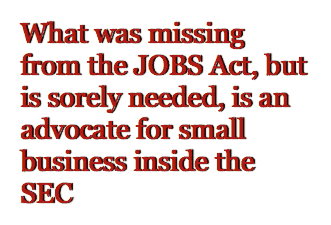

The Missing Title of the JOBS Act – “Small Business Advocate”

If history is to be any guide, what was missing from the JOBS Act, but is sorely needed, is an advocate for small business inside the SEC, with broad statutory powers and a direct reporting relationship to Congress – what I call a Small Business Advocate (SBA).

If history is to be any guide, what was missing from the JOBS Act, but is sorely needed, is an advocate for small business inside the SEC, with broad statutory powers and a direct reporting relationship to Congress – what I call a Small Business Advocate (SBA).

The JOBS Act of 2012 is not the first legislative initiative to jumpstart the engine of job creation – small business. Back in 1980, as was the case with the JOBS Act, under a Democratic administration with broad bi-partisan support, Congress enacted historic, sweeping legislation intended to both reduce the regulatory burdens on small business in the capital formation process, and to open new paths for capital formation for small business. Part of this legislation provided for initiatives to encourage cooperation between the SEC and state securities regulators, and to facilitate input from small business in the SEC rulemaking process – the latter through an annual forum, or roundtable – bringing together leaders from small business and government – to provide recommendations and initiatives to assist the SEC in new rulemaking to ease the burden of capital formation on small business.

More than 30 years later – the policies and objectives behind this bi-partisan legislation remain valid – however, small business has been left with nothing but empty promises and empty pockets. The so-called SEC Government-Small Business Forum, under the auspices of the SEC Office of Small Business of Policy, has proven to be a dismal failure. The SEC website is replete with year after year of consensus recommendations – which have gone almost entirely unheeded.

Included in these recommendations have been consensus conclusions that Regulation A $5 million offerings need to be exempt from state blue sky regulation. Most recently, in November 2012, the Number One consensus recommendation – that the SEC provide an optional, simplified question and answer disclosure format for Title III crowdfunded offerings – has been ignored entirely – and likely will continue to be when the final rules take effect.

And the November 2013 SEC Small Business Forum was even less promising. Unlike the 2012 Forum, where four SEC Commissioners were present, in 2013 only one of the five SEC commissioners even bothered to show up.

And the November 2013 SEC Small Business Forum was even less promising. Unlike the 2012 Forum, where four SEC Commissioners were present, in 2013 only one of the five SEC commissioners even bothered to show up.

And need I recall how the Commission thumbed its nose at Congress, delaying rulemaking under both Title II and III of the JOBS Act, well beyond the mandatory rulemaking deadlines set by Congress.

Though there is no single magic bullet which will more effectively advance the interests of small business at the SEC, clearly more is needed. What is essential is that Congress create a new office at the SEC, Small Business Advocate, whose sole function would be to advocate the interests of small business at the SEC in all areas where significant policy interests of small business are at stake.

This new office ought to include, by necessity:

- A Small Business Advocate, both experienced in the representation of small business, with expertise in securities regulation – and lacking any prior tenure as an SEC officer or employee.

- Direct reporting to both the SEC Chair and to Congress, with reporting responsibilities to Congress no less frequently than annually – with both a retrospective and prospective review and plan.

- Access to all documents and personnel in the Commission which impact small business.

- Participation in all policymaking and rulemaking initiatives affecting small business, including ad hoc membership on all committees addressing issues impacting small business.

- Statutory authority to enforce, through judicial proceedings, provisions of the Regulatory Flexibility Act of 1980, as amended, intended to require the SEC to consider rulemaking alternatives which are not burdensome on small business – so long as such proceedings do not interfere with the effectiveness of any rule before there is a final judicial ruling on whether the SEC has violated the terms of the Regulatory Flexibility Act.

The concept of a federal agency having a specifically designated advocate to protect certain interests is not a foreign one. There is an office of taxpayer advocate in the Internal Revenue Service. And most recently, through Congressional legislation, the Office of Investor Advocate was created at the SEC. Surely, if after 80 years of protecting investors an Investor Advocate is appropriate, then after more than 33 years of inaction following well intentioned federal legislation, a Small Business Advocate to protect the interests of small business is long overdue.

The concept of a federal agency having a specifically designated advocate to protect certain interests is not a foreign one. There is an office of taxpayer advocate in the Internal Revenue Service. And most recently, through Congressional legislation, the Office of Investor Advocate was created at the SEC. Surely, if after 80 years of protecting investors an Investor Advocate is appropriate, then after more than 33 years of inaction following well intentioned federal legislation, a Small Business Advocate to protect the interests of small business is long overdue.

Some might argue that such a position would be redundant with the SEC Office of Small Business Policy. Apart from the lessons which decades of history have taught us, one need only look at who has populated the leadership position in this office – individuals with little or no experience representing the interests of small business – many of whom have as their primary qualification their longevity of prior service at the SEC.

And if this were not problematic enough for small business, one ought to look at one of the core functions of the Office of Small Business Policy – to serve as a liaison between the SEC and state securities administrators. How’s that working out for small business?

And if this were not problematic enough for small business, one ought to look at one of the core functions of the Office of Small Business Policy – to serve as a liaison between the SEC and state securities administrators. How’s that working out for small business?

The bottom line – Congress needs to come together one more time – to finish what it started – in the interest of advancing the objectives of the JOBS Act, – job creation for small business through enhanced tools for capital formation.

______________________________________

Samuel S. Guzik, a recognized authority on the JOBS Act including Regulation D private placements, investment crowdfunding and Regulation A+, writes a regular column, The Crowdfunding Counselor, for Crowdfund Insider. A consultant on matters relating to the JOBS Act, he recently led a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy. He is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience. He is admitted to practice before the SEC and in New York and California. Guzik has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.

Samuel S. Guzik, a recognized authority on the JOBS Act including Regulation D private placements, investment crowdfunding and Regulation A+, writes a regular column, The Crowdfunding Counselor, for Crowdfund Insider. A consultant on matters relating to the JOBS Act, he recently led a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy. He is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience. He is admitted to practice before the SEC and in New York and California. Guzik has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.