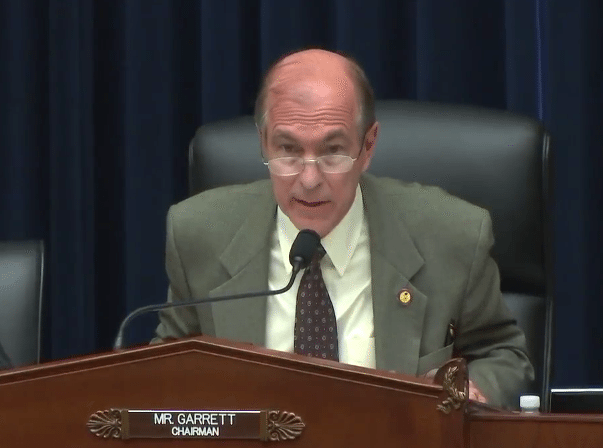

The Subcommittee on Capital Markets and Government Sponsored Enterprises, part of the House Financial Services Committee, reviewed several proposed acts of legislation crafted to help smaller business and grow the economy today (April 14). Chaired by Congressman Scott Garrett, the hearing was labeled “The JOBS Act at Four: Examining Its Impact and Proposals to Further Enhance Capital Formation”. The gathering included new legislation sponsored by Patrick McHenry entitled the “Fix Crowdfunding Act“, designed to improve upon existing Title III retail crowdfunding rules and enhance investor protection.

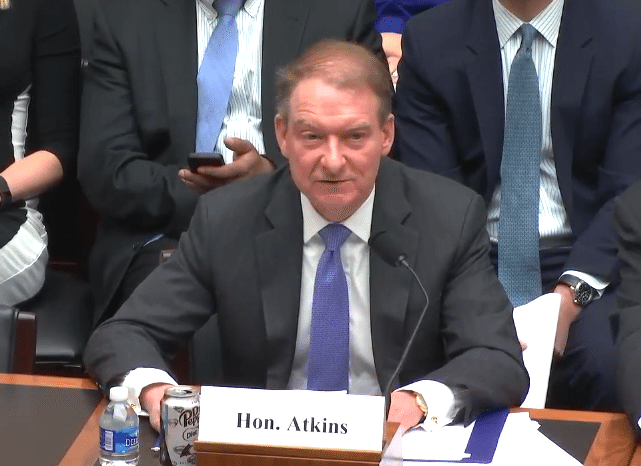

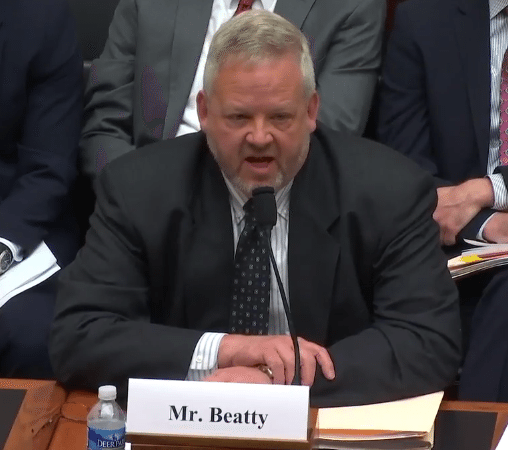

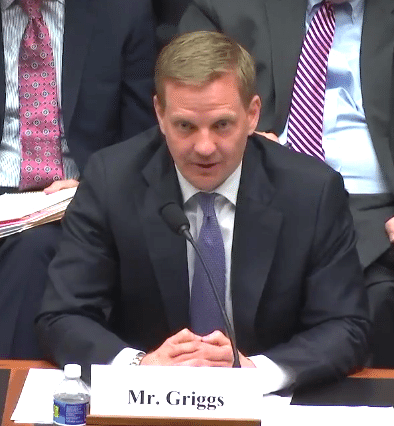

The hearing saw prepared remarks delivered by five witnesses including Kevin Laws of AngelList, Raymond Keating of the Small Business & Entrepreneurship Council, Nelson Griggs of NASDAQ, William Beatty of the Division of Securities of the State of Washington, and Paul Atkins a former SEC Commissioner.

The hearing saw prepared remarks delivered by five witnesses including Kevin Laws of AngelList, Raymond Keating of the Small Business & Entrepreneurship Council, Nelson Griggs of NASDAQ, William Beatty of the Division of Securities of the State of Washington, and Paul Atkins a former SEC Commissioner.

Congressman Garrett opened the proceedings by commenting on the JOBS Act legislation pointing to the fact that updated rules have improved capital formation for smaller companies. He stated the law empowered entrepreneurs and improved the economy for all, not by spending taxpayer money but by streamlining processes that were designed for 1934 instead of 2016.

Congressman Garrett stated;

- The JOBS Act has led to a resurgence in the IPO market, with some 85% of IPO’s since April 2012 coming from emerging growth companies

- Companies have raised some $50 billion under the new Reg D provision that allows business to solicit an offering to the general public

- While the newly modernized “Reg A+” is only a year old, business are already beginning to issue securities under this exemption

- Recent reports indicate that the SEC has already received up to 30 applications for portals under the new crowdfunding rules, which are set to go live next month

But Garrett cautioned there is more to be accomplished.

“…The point of this hearing is not to pat ourselves on the back and say “job well done For starters, because the Senate tried its best back in 2012 to neuter the crowdfunding title and the SEC has taken some liberties with other rulemakings, the JOBS Act needs some “fixing”, stated Garrett.

Atkins, who is currently CEO of Patomak Global Partners, acknowledged the fact that small businesses accounted for 63% of the net new jobs created in the U.S.

Atkins, who is currently CEO of Patomak Global Partners, acknowledged the fact that small businesses accounted for 63% of the net new jobs created in the U.S.

“…if we are serious about spurring strong and lasting economic growth, creating more jobs outside of Washington, D.C., and breaking down our two-tiered economy, we do not need higher taxes or more government spending – instead, the data suggest that we need more entrepreneurs and more small businesses, and we need to continue to create a sensible regulatory environment in which these firms and individuals can succeed,” said Atkins.

He called the Obama Administration “the most prolific regulatory force in U.S. history.”

He called the Obama Administration “the most prolific regulatory force in U.S. history.”

Beatty, who is presently Chair of North American Securities Administrators Association (NASAA) Committee on Small Business Capital Formation, pointed to his role as a state regulator as the “cop on the beat”. He expressed NASAA’s concerns about the proposed legislation. He pointed to rule 506 and the potential for fraud;

“Title II of the JOBS Act repealed a long-standing prohibition on general solicitation and advertising of securities under Rule 506. State securities regulators remain deeply concerned about the negative impact these changes will have on investors in our states. In 2014, the most recent year for which data is available, Regulation D Rule 506 offerings were the second most frequently reported fraudulent product or scheme involved in enforcement actions by state securities regulators.”

Griggs, Executive Vice President of Nasdaq, shared his perspective that “even with the JOBS Act in place, there are issues that remain, and there are dark clouds still affecting the private company view of the public markets.” Highlighting the role that NASDAQ plays in both private and public capital formation, Griggs stated;

Griggs, Executive Vice President of Nasdaq, shared his perspective that “even with the JOBS Act in place, there are issues that remain, and there are dark clouds still affecting the private company view of the public markets.” Highlighting the role that NASDAQ plays in both private and public capital formation, Griggs stated;

“Four years have now passed and the evidence is clear that the JOBS Act has successfully helped hundreds of companies access capital and go public while also generating new dynamism in the private company sector. Our records indicate that 785 companies have gone public as Emerging Growth Companies (EGCs) under the JOBS Act raising over $103 billion in capital to expand, hire employees and compete on the global stage.”

Raymond Keating, Chief Economist for the SBE Council, said many entrepreneurs still struggle to access the funding they need to grow and create jobs. Keating expressed his concern regarding the excessive regulation and associated costs that has harmed access to capital.

Raymond Keating, Chief Economist for the SBE Council, said many entrepreneurs still struggle to access the funding they need to grow and create jobs. Keating expressed his concern regarding the excessive regulation and associated costs that has harmed access to capital.

“To sum up, long after the financial crisis hit in late 2008 and the Great Recession came to an official end in mid-2009, the value and number of traditional small business loans are still down markedly, and angel investment is still down compared to 2008. Based on these numbers, the struggle for entrepreneurs to gain access to the financial resources needed to start up, thrive or just survive continues to be difficult,” testified Keating. “The bottom line is that small businesses need more options or avenues to expand access to financial capital. The securities market would seem to be an option, but the regulatory and legal costs long had been prohibitive.”

Kevin Laws, COO of AngelList, focused on his ground level experience. Since launching their platform in 2013, AngelList has raised capital online of approximately $250 million for about 1000 companies. Having raised money via the internet using “accredited crowdfunding”, legalized under Title II of the JOBS Act, AngelList has captured hard earned wisdom as to what works online – and what does not.

Kevin Laws, COO of AngelList, focused on his ground level experience. Since launching their platform in 2013, AngelList has raised capital online of approximately $250 million for about 1000 companies. Having raised money via the internet using “accredited crowdfunding”, legalized under Title II of the JOBS Act, AngelList has captured hard earned wisdom as to what works online – and what does not.

“…we have settled on techniques that protect investors interests while still encouraging capital formation for good companies. Unfortunately, some of those techniques to protect investors would not be legal under the final [Title III] crowdfunding rules. HR 2855, the “Fix Crowdfunding Act,” would go a long way towards improving the underlaying crowdfunding measure adopted four years ago.”

As one may expect, much of the discussion hovered around as to how to best protect investors.

As one may expect, much of the discussion hovered around as to how to best protect investors.

Asked by Congressman McHenry if Title III, as it stands now, would be useful, Laws explained that it was dangerous as written now. Title III may be used by companies that cannot raise under Title II of the JOBS Act. He called it a potential marketplace for major problems. Laws believes that the Fix Crowdfunding Act goes a long way in protecting investors and improving on existing rules. On AngelList today, they use a syndicate model where a lead investor plays an important role in raising capital for an early stage company thus mitigating risk. The ability to use a similar vehicle would be allowed if the Fix Crowdfunding Act becomes law.

While concerns of possible fraud remain, Atkins pointed to the fact that under Title II, 506(c), there has really not been much fraud at all. This is something that was echoed by the SEC in a presentation earlier this year.

While concerns of possible fraud remain, Atkins pointed to the fact that under Title II, 506(c), there has really not been much fraud at all. This is something that was echoed by the SEC in a presentation earlier this year.

Congressman Hines questioned the ability of retail investors to make any money in these crowdfunding offers*. Congressman Neugebauer defended the little guy stating they have been blocked from the opportunity to invest in early stage companies in the past.

While much was discussed the discourse was a prelude to an eventual vote on the aforementioned bills. In closing, Congressman Garrett summed it up as not being a question of “no regulation but appropriate regulation.”

The four bills under discussion:

- H.R. 4850, the “Micro Offering Safe Harbor Act”

- H.R. 4852, the “Private Placement Improvement Act of 2016″

- H.R. 4854, the “Supporting America’s Innovators Act of 2016″

- H.R. 4855, the ‘Fix Crowdfunding Act”

The hearing committee video is below.

*David S. Rose, Managing Principal of Rose Tech Ventures, on Angel Investing.

“The average annual return from investing in publicly traded companies is roughly 5%. The average annual return from an active, professionally managed, disciplined, long-term, angel investment portfolio is roughly 25%.”