I have been immersed in the equity crowdfunding industry since late 2015 and have tried to collect as many different perspectives on the industry from as many experts as possible. And while it is hard to predict the ultimate fate of an industry that had not been in existence until May 16, 2016, I found there to be no lack of opinions. As anyone would expect, a consensus among those who are experts in the crowdfunding industry was hard to come by. When I would ask experts their predictions on how equity crowdfunding for the masses would turn out, responses spanned the spectrum from ‘dead in the water’ to the most optimistic of ‘it will start out slow but catch on over time’. The latter opinion was shared by the co-author of the JOBS act and current Crowdfund Capital Advisors founder Woodie Neiss. According to Neiss;

“if you look back over history, change happens slowly and when it comes to financial markets adoption of new technology depends on market use and credibility. Both of those are built over time.”

Part of the problem with the initial legislation of Title III was that it would be too restrictive from a cost and regulatory perspective for early-stage companies to raise capital. Add to that the $1M per 12-month period limit placed on funding rounds and pessimists thought it just wasn’t going to be the right environment for many founders. However, we are continuing to see signs of life in the industry even though we have yet to see five full months of data. Regulatory restrictions are turning out to be not as onerous as expected and costs to get a funding round up on a platform are lower than many had estimated. And Woodie Neiss believes things are only going to get better from this perspective. According to Neiss;

“There is already a fix that passed the US House of Representatives. This may ease the cost of putting one of these offerings together which includes accountants and lawyers to social media experts and videographers.”

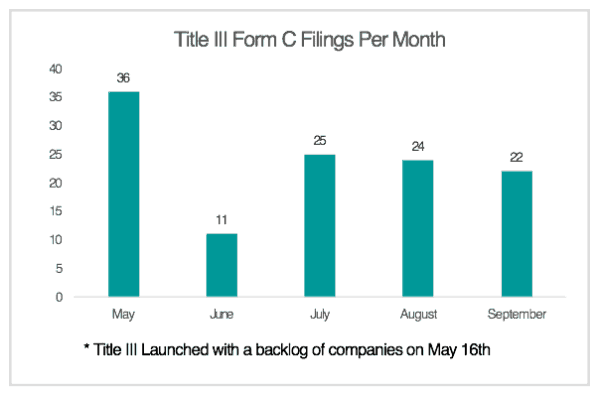

Even from the most optimistic of opinions that I heard prior to the launch of Title III crowdfunding, things are actually looking very good. Here is a look at monthly Form C filings made by companies to the SEC in the first few months:

There is no doubt that we still have a long way to go. But an industry starting from a base of zero on May 16th and now averaging over 20 new companies raising per month should be viewed as a win for equity crowdfunding, especially given that awareness of this type of capital raising has yet to catch on with mainstream Americans and founders alike. Trends are encouraging and over time we will see this industry (both Title II and Title III) become the go-to funding channel for early stage companies and investing channel for accredited and non-accredited investors. Time is all this industry needs, but we should all be encouraged with progress so far exceeding the highest of initial expectations.

Investors Beware: Not all Funding Structures are Created Equal

I recently read an article on Crowdfund Insider written by Joe Green and John Coyle titled Is the SAFE Not So Safe for Investment Crowdfunding? which directly touches on one of the few issues that have arisen in the first months on Regulation Crowdfunding in the U.S. At Stratifund, we have analyzed all of the Regulation CF deals that have gone live since May and have kept especially close eye on the companies who have tried to raise capital using these so called SAFEs. Aside from the far misleading acronym that an unsophisticated investor might take literally, certain terms of the SAFEs are also not advantageous to investors under Regulation CF. Mr. Green and Mr. Coyle did a nice job of laying out the issues investors might face with these financing structures, so I am not going to repeat what has already been said.

I recently read an article on Crowdfund Insider written by Joe Green and John Coyle titled Is the SAFE Not So Safe for Investment Crowdfunding? which directly touches on one of the few issues that have arisen in the first months on Regulation Crowdfunding in the U.S. At Stratifund, we have analyzed all of the Regulation CF deals that have gone live since May and have kept especially close eye on the companies who have tried to raise capital using these so called SAFEs. Aside from the far misleading acronym that an unsophisticated investor might take literally, certain terms of the SAFEs are also not advantageous to investors under Regulation CF. Mr. Green and Mr. Coyle did a nice job of laying out the issues investors might face with these financing structures, so I am not going to repeat what has already been said.

What I do want to touch on is that SAFEs are not the only type of structure an investor needs to look out for. Just like with SAFEs, there is a time and place for most funding types, but at my company have found that many founders are choosing funding structures that are not advantageous to them, their companies, or the potential investors of the round, however much the founder perceives this to be the opposite.

Case in point, we analyzed and wrote a report on a company last week that had a great business model, and its founder was a first time entrepreneur who identified a need for a brewery in his hometown. He clearly had passion for his business but it also appeared as though he had not been given the proper advice on what funding type was best for his current position. Despite needing capital to build out his brewery, make his beer, buy brewing equipment, market his product, and then wait to get to a breakeven level of production in order to start making money, he chose a short-term funding revenue share structure which would start taking 10% of all of his revenues upon sale of his first beer. The issue with this is that breweries are small margin business and it takes a lot of capital and time to get to break even. What this owner needed was to give up some equity and to take on long term investors who will be patient with the growth process. Most likely this was an unsophisticated founder who thought “If I keep more equity in my business, then it’s a positive for me” when it couldn’t be further from the truth. Sure the founder still owns all of his business, but now he will be squeezed on growth capital. The very thing he needs to grow his business (cash) is now being paid out to investors who don’t care about his profitability and only want their promised return, which was 50% in this case.

Case in point, we analyzed and wrote a report on a company last week that had a great business model, and its founder was a first time entrepreneur who identified a need for a brewery in his hometown. He clearly had passion for his business but it also appeared as though he had not been given the proper advice on what funding type was best for his current position. Despite needing capital to build out his brewery, make his beer, buy brewing equipment, market his product, and then wait to get to a breakeven level of production in order to start making money, he chose a short-term funding revenue share structure which would start taking 10% of all of his revenues upon sale of his first beer. The issue with this is that breweries are small margin business and it takes a lot of capital and time to get to break even. What this owner needed was to give up some equity and to take on long term investors who will be patient with the growth process. Most likely this was an unsophisticated founder who thought “If I keep more equity in my business, then it’s a positive for me” when it couldn’t be further from the truth. Sure the founder still owns all of his business, but now he will be squeezed on growth capital. The very thing he needs to grow his business (cash) is now being paid out to investors who don’t care about his profitability and only want their promised return, which was 50% in this case.

Obviously, there is no malice nor wrongdoing with what the founder decided to do, but it should be noted for all investors looking to invest in startup companies that all fundraising structures are not equal for all situations. If the above-mentioned founder pursued an idea in a lower capital intensive industry or had a steady stream of revenue with much of his capital expenditures behind him, then a revenue share might make sense. Unfortunately, he decided on a structure that from his vantage point appears to be most advantageous to him but we believe will ultimately limit the growth of his business.

There are many risks of investing in early stage companies, and a savvy investor needs to be aware that risks come in all shapes and sizes.

Marc Snover is CEO & Co-Founder of Stratifund an independent, unbiased, centralized source of information about equity crowdfunding deals. Marc has extensive background in business valuation and due diligence research in investment banking, corporate development and as a research analyst covering both the buy side and sell side of M&A transactions. Marc has led numerous teams through all stages of M&A, debt/equity financings and other deal structures. He also has experience in financial securities regulation as a broker/dealer auditor for FINRA. Marc holds a Economics and Finance degree from Southern Methodist University and an MBA from the University of Notre Dame, Mendoza College of Business.

Marc Snover is CEO & Co-Founder of Stratifund an independent, unbiased, centralized source of information about equity crowdfunding deals. Marc has extensive background in business valuation and due diligence research in investment banking, corporate development and as a research analyst covering both the buy side and sell side of M&A transactions. Marc has led numerous teams through all stages of M&A, debt/equity financings and other deal structures. He also has experience in financial securities regulation as a broker/dealer auditor for FINRA. Marc holds a Economics and Finance degree from Southern Methodist University and an MBA from the University of Notre Dame, Mendoza College of Business.