lending clubLending Club (NYSE:LC) has filed an 8-K regarding an investor update from the company’s Chief Investment Officer Siddhartha Jajodia.

lending clubLending Club (NYSE:LC) has filed an 8-K regarding an investor update from the company’s Chief Investment Officer Siddhartha Jajodia.

The letter includes an update on expected delinquency rates across the existing loan portfolio following changes made several times in 2016, and implemented additional changes on January 11, 2017 to tighten the thresholds on borrower leverage on unique combinations of risk factors, According to the document, Lending Club has “seen signs of stabilization in delinquency rates across the existing loan portfolio.”

The document also provided some perspective on Q1 of 2017 stating:

Economic Backdrop. There are signs indicating that the American economy remains strong (the Federal Reserve recently raised interest rates in December 2016, unemployment remains low at 4.7%, the economy added approximately 156,000 jobs in December 2016, and housing prices remain strong).1 On the other hand, some consumers have appeared to be taking on more debt overall (such as student loans, auto loans, credit cards, etc.). As we noted throughout 2016, we observed this trend on the Lending Club platform in populations characterized by high indebtedness and an increased propensity to accumulate debt. We will continue to monitor trends and take action accordingly. Note that overall economic indicators are not necessarily indicative of the behavior of any particular borrower on the Lending Club platform

Economic Backdrop. There are signs indicating that the American economy remains strong (the Federal Reserve recently raised interest rates in December 2016, unemployment remains low at 4.7%, the economy added approximately 156,000 jobs in December 2016, and housing prices remain strong).1 On the other hand, some consumers have appeared to be taking on more debt overall (such as student loans, auto loans, credit cards, etc.). As we noted throughout 2016, we observed this trend on the Lending Club platform in populations characterized by high indebtedness and an increased propensity to accumulate debt. We will continue to monitor trends and take action accordingly. Note that overall economic indicators are not necessarily indicative of the behavior of any particular borrower on the Lending Club platform- Borrower Performance. Throughout 2016 and into 2017 we have continued to observe the same trends on the Lending Club platform: indicators suggest a strong U.S. economy, but some borrowers are not offering appropriate levels of risk- adjusted return. As part of our continuous risk management process we have identified additional ways to optimize models around specific combinations of risk indicators while maintaining solid investor yields. Effective January 11, 2017, changes were implemented to tighten credit criteria based on unique combinations of risk factors such as number of recent installments loans, revolving utilization, and higher risk scores on our proprietary scorecard. Borrowers who meet these specific combinations of risk factors model lower risk-adjusted returns than their otherwise similar peers. This group represents a small portion of the total borrower population but a notable portion of higher risk borrowers. In addition to implementing these changes to credit policy, we continue to regularly invest in our multifaceted collections capabilities to further mitigate risk. Recent efforts include adding new recovery strategies, adding a new agency partner and expanding our internal collections team capacity.

- Interest Rates. The Federal Reserve raised its target rate by 25 bps in December 2016. Based on proactive interest rate increases made in 2016 for loans facilitated on our platform (with a weighted-average increase of approximately 118 basis points), we believe our marketplace already reflects the higher interest rate environment; therefore, interest rates are not changing at this time. Lending Club will continue to take a deliberate, prudent approach to risk management and will adapt as needed.

- Other Factors. Investor returns are also impacted by other factors, such as prepayment rates, the size and diversity of a portfolio, the exposure to any single loan, borrower or group of loans or borrowers, as well as other externalities and macroeconomic conditions. Recently, market rates for sales of charged-off loans to third party purchasers have decreased, which has impacted investor returns.

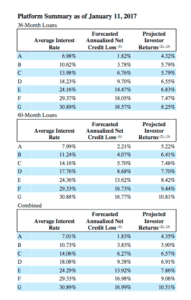

Lending Club also provided a graph of forecasted investor returns and net credit loss.

Lending Club will announce Q4 2016 results after the market closes on February 14th.

The 8-K is embedded below.

[scribd id=336935884 key=key-vjw1X8pn2iAP7lEGWAe0 mode=scroll]