Recently, the European Securities and Markets Authority (ESMA) held its first ever conference in Paris. The event underlined the growing importance of ESMA, the European Supervisory Authority for capital markets. Along with the European Commission and the Parliament, ESMA is one of the pillars of Europe’s Capital Markets Union (CMU), the ongoing effort to create of a single market for capital in the European Union (EU). ESMA is now officially the watchdog to watch for fintechs in wealth management, asset management, and financial investment services in the European Union (EU).

The ESMA conference highlighted the impending coming into force of the second Markets in Financial Instruments Directive (MiFID II) as a game changer and a major milestone towards the achieving the CMU.

Among many speakers, Steven Maijoor, Chair of ESMA, Valdis Dombrovskis, Vice-President of the European Commission, and Roberto Gualtieri, Chair of the Committee on Economic and Monetary Affairs (ECON) of the European Parliament discussed the CMU Action Plan. As the event went on, these discussions revealed how major a setback the Brexit is for the CMU.

If you’re not familiar with the workings of the EU, prepare for the alphabet soup of EU regulation acronyms.

ESMA, Supervisory Convergence and Product Intervention

As speakers stressed, EU regulation is not an end goal. The ultimate goal of the Capital Markets Union is to foster the development of equity markets in the EU ‒ making the financial system less reliant on debt, hence more stable. Currently only 24% of company funding in the EU is equity funding, against 38% in China and 48% in the US.

By removing regulatory barriers to cross-border investments, the CMU will help ease the EU’s 23 million SMEs’ access to capital, so that they can create jobs for the 20 million unemployed.

“Can we have a single rule book for the CMU without a single supervisor?”

This was the rhetorical question asked by Olivier Guersent, Director General of the Directorate-General for Financial Stability, Financial Services and Capital Markets Union of the European Commission, also known as DG FISMA. The answer, of course, was no.

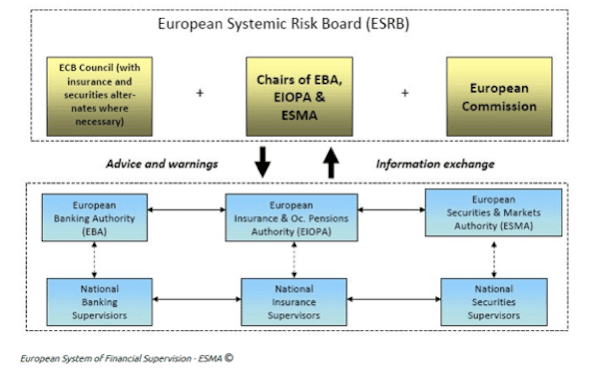

Beyond defining a single rulebook, the EU must make sure that these rules are consistently implemented and applied in the 28 Member States ‒ soon to be 27 after the UK leaves. This challenge is called, quite euphemistically, “supervisory convergence.” Concretely, supervisory convergence means that European Supervisory Authorities (ESAs) must have more power, including more enforcement power. ESMA is one of the three ESAs in EU financial services. The other two are the European Banking Authority (EBA) for banking and the European Insurance and Occupational Pensions Authority (EIOPA) for insurance.

Supervisory convergence is a huge challenge. Indeed, national regulators of EU Member States, called in this context “national competent authorities” or NCAs, operate in very diverse local political, economic and cultural environments and, hence, tend to easily diverge from each other when they transpose EU directives into national law. For this reason, MiFID will be implemented directly through a European regulation, the Markets in Financial Instruments Regulation (MiFIR). In addition, MiFIR will give ESMA a product intervention power, i.e. the ability to intervene directly and, for example, ban a product if it poses a threat for investors or for the integrity of capital or commodity markets.

The Imminent Coming into Force of MiFID II

“I don’t want to spread panic, but in 80 days MIFID is there.”

This is how Elisabeth Roegele, Executive Director, Securities Supervision, at the German Federal Financial Supervisory Authority (BaFin) introduced a panel discussion on MiFID II and MiFIR.

The breadth and depth of MiFID II is quite unprecedented. Large firms, including large exchanges, are on track, but smaller ones are not. Yet, the date of MiFID II’s entry into force, 3 January 2018, will not be pushed back again, as it was already delayed by a year.

Here are the main MiFID changes (non-binding summary):

- Customer protection: Enhanced requirement in terms of suitability testing and appropriateness of product, product information, product performance reporting, and pricing transparency.

- Products: Increased product governance. Investment product manufacturers must submit their products for review and publish product performance data. They are responsible for the distribution of their products to appropriate target markets.

- Unbundling of advice: Inducements, commissions and rebates for independent advisors are banned.

- Market infrastructure: Broader scope of supervision to include equity and non-equity trading. Increased transparency requirements for all trading facilities, including Regulated Markets, Multilateral Trading Facilities (MTFs), Organized Trading Facilities (OTF) and Systematic internalizers (SI) and high-frequency trading.

- Best Execution: Firms must take “all sufficient steps” to ensure that transactions are executed in the best interest of customers.

- Data reporting: The requirements for transaction data reporting increase considerably.

Along with removing trade barriers, MiFID is also intended to bring back to capital markets the retail investors who have deserted them after the financial crisis. EU representatives, including Member of the European Parliament, Pervenche Berès firmly believe that MiFID’s strengthened customer protection rules will help achieve this goal. Some critics pointed out, however, that transparency might make products too complex and will not make up for the lack of equity culture among EU private investors.

The final word on MiFID probably goes to Markus Ferber, German Member of the European Parliament (MEP), who said:

“MIFID II was never meant to make financial institutions happy, but to make the financial system safer.”

EU Regulatory Achievements and Forthcoming Agenda

During the discussions, speakers highlighted several achievements of CMU-related regulations:

- The Alternative Investment Fund Managers Directive (AIFMD) has defined a EU framework and a EU passport for alternative investment firms.

- The packaged retail and insurance-based investment products (PRIIPs) has enhanced product information through the definition of the Key Information Document (KID).

- The new Prospectus Regulation, following the proportionality principle, has defined simpler rules for smaller capital raisings and raised the threshold of prospectus exemption from €100K to €1 million.

- The Simple, Transparent and Standardized Securitization (STS) policy has defined a new regulatory framework for adequately supervised securitization.

Among the main items remaining on the agenda were mentioned:

- The constitution of new EU-wide databases such as Financial Instruments Reference Data System (FIRDS) and Access to Trade Repositories Project (TRACE) that enable trading monitoring and analytics.

- The revised European Market Infrastructure Regulation (EMIR) designed to further enhance the transparency of derivatives markets and further reduce systemic risk.

- Equivalence negotiations with non-EU countries.

- An EU-integrated market for personal pension products (PPPs).

- Fintech and financial innovation support.

Brexit and the Cliffhanger Worst Case Scenario

When the Action Plan for the CMU was designed, nobody had an inkling that the UK, which represents about 2/3 of the union’s equity trading, would leave the EU.

The sorest point of the Brexit discussion at the ESMA event was the issue of Central Counterparties (CCPs) and of the possible (but certainly not easy) relocation of the clearing of financial products denominated in euros into the EU zone. Currently, the London Clearing House (LCH) clears 98% of all swaps in euros.

A major concern cited by EU officials was that the Brexit could trigger a “regulatory race to the bottom”, i.e. competition on regulatory and supervisory standards with the UK and among the EU 27. In response, Xavier Rolet, CEO of the London Stock Exchange Group, countered that:

“Competition is essential within the EU and between the UK and the rest of the world.”

Industry representatives bemoaned the current uncertainty about the terms of the Brexit. The cliffhanger scenario, in which the industry would be taken by surprise after a drawn-out negotiation process, was generally considered a worst-case scenario.

Sylvie Matherat, Chief Regulatory Officer Deutsche Bank, warned that the industry would not be able to wait much longer to take action for its clients:

“If we had a hard Brexit, at least it would be organized.”

In the end, despite a few soothing words about the persistence of shared interest and culture between the UK and the rest of the EU, the event showed the Brexit as a major impediment to the CMU, with no positive, but only loss-mitigating outlooks.

Therese Torris, PhD, is a Senior Contributing Editor to Crowdfund Insider. She is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique.

Therese Torris, PhD, is a Senior Contributing Editor to Crowdfund Insider. She is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique.