There’s a Fintech revolution happening in Minnesota. Since passing its own version of intrastate crowdfunding legislation in 2015 and quietly opening its doors in 2016 the state has taken the regional lead in raising more money for more businesses under its “MNvest” exemption as well as the older Small Corporate Offering Registration (SCOR) exemption than all the states in the region combined.

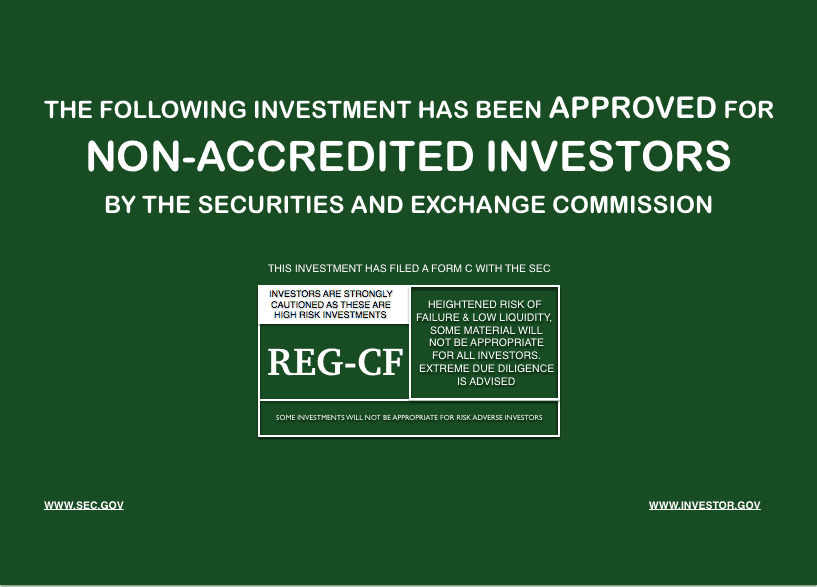

Intrastate based investment crowdfunding today is superior to the interstate Regulation Crowdfunding aka REG-CF option representing lower friction, a lower cost of capital and access to larger investment amounts from everyday people. Unless some changes are made to REG-CF, and soon, it will likely be relegated to history as a failed experiment and those using it will face significant headwinds in raising subsequent rounds of capital.

The Democratization of Capital

The laws surrounding investments in the United States were written largely in an era of wooden ships and telegraphs. Very few homes had telephones and the predominant form of communication was radio and newspaper. We still affectionately refer to that tomb of restrictions as “The Acts of 1933 and 1934.” They were written under the rubric of inequitable information asymmetry.

The laws surrounding investments in the United States were written largely in an era of wooden ships and telegraphs. Very few homes had telephones and the predominant form of communication was radio and newspaper. We still affectionately refer to that tomb of restrictions as “The Acts of 1933 and 1934.” They were written under the rubric of inequitable information asymmetry.

If you want to know what “information asymmetry” actually FEELS like, have your car break down in rural Nebraska sometime with a dead cell phone, hitch-hike to the nearest roadside motel with no wifi, check-in using cash only while asking to use a landline to call a tow truck to get your car to a garage that will accept personal checks all while having a desperate need to place a winning bid on tickets to an Imagine Dragons concert before the weekend is out. Welcome to buying stock on the open market in the 1930’s.

“The Act” was in large part a reaction to the rampant and reckless speculation during the run-up to the stock market crash of 1929.

The actual causes, of course, are largely lost to time, however, a little digging reveals that the bulk of the losses were due to bankers using depositors funds to speculate, and largely without their knowledge or permission. It was NOT, as some would have you believe, just like the heady “dot com” days where individual investors were accessing discount brokers online and shorting stuff they had no business shorting.

The effect of “The Act” was to put a chill on the opportunity for the vast majority of Americans for over 80 years and has resulted in the creation of a wealth chasm separating us into “Accredited” investors (the top 3%) and everyone else.

You read that right – just 3% of the population as defined by their income or net worth has been permitted to make investments in startups or income-producing real estate deals as they see fit while the rest of us have been treated like second class citizens simply because the government has outsourced its discernment of financial fitness to a person’s wealth.

The case of virtual reality headset company “Oculus Rift” could not be more relevant, having hosted a wildly successful Kickstarter campaign in 2012 raising over $2.4M* and all those early “backers” (over 9,500 in all) now have an obsolete brick on their shelves instead of the right to pay off a student loan, buy a car or put a down payment on a house. The “investors” who came in after them got more than a 20X return on their investment a few years later after Oculus Rift sold to Facebook for 2.3B in cash*. That’s inequitable a/f.

With the passing of the JOBS Act of 2012 a batch of changes were approved to remove friction from the process of issuing securities as well as a bipartisan mandate to allow for a form for everyday investors to participate through “crowdfunding” in Title III of the bill. Of course, as we now know having a bill passed and actually getting to utilize it doesn’t take “an act of Congress”; it takes the legacy bureaucratic infrastructure years to digest, synthesize, and interpret the intention and codify it in rules that they think make sense for everyone.

Tired of waiting for the SEC to make Regulation Crowdfunding effective, over 30 states passed various forms of intrastate crowdfunding laws based in part on the model legislation approved in the JOBS Act signed into law. The first Funding Portals started to appear in 2014 but were largely focused on accredited investors only with the first truly open portals showing up in late 2016.

Let’s (Mis)Treat Everyone Equally

REG-CF has the highest “cost of capital” of all the exemptions. Let’s look at why.

Under REG-CF all investors are treated the same, subject to an income and net-worth means test that sets caps on what an adult investor can invest per rolling twelve month period. The numbers are adjusted for inflation periodically and currently set the floor at $2,200 and a cap at $107,000 subject to either a 5% of the lesser income/net-worth test for amounts up to $107,000 or 10% for income/net worth amounts over $107,000. Thankfully the math is managed by the portals under a “self-reported” model that is supposed to capture any investments made outside of a given portal in the past 12 months.

This means that an accredited investor under REG-CF, who would normally be eligible to invest as much as they wanted, are prevented from investing more than $107,000. It is exactly why we’re seeing dual offerings where a company will concurrently run a REG-CF and a REG-D offering with a self-selection option to send accredited investors into the REG-D offering. In other words, just as the internet is designed to “route around censorship” the capital markets are also just as efficient at “routing around bad regulations.”

REG-CF allows for issuers to use self-reported financials for raises up to $107,000 and then requires either audited or reviewed financials (depending on how long the issuer has been in business) for amounts over $107,000. These fees add to the cost of capital in amounts as low as $3,500 for a quick CPA review on up to $20,000 or more for full-blown audits. Add to this the cost for legal preparation, portal fees, and possibly bank escrow fees and it makes REG-CF untenable. Nobody is going to spend $50K for the chance raise $150K.

Contrast this with intrastate exemptions like MNvest where an issuer can raise up to $1 million with self-reported financials and up to $2 million if they have been reviewed or audited and you begin to understand why REG-CF is like the village idiot that no one wants to claim. Getting access to investors in all 50 states for low amounts of capital is about the only compelling reason to use it.

Contrast this with intrastate exemptions like MNvest where an issuer can raise up to $1 million with self-reported financials and up to $2 million if they have been reviewed or audited and you begin to understand why REG-CF is like the village idiot that no one wants to claim. Getting access to investors in all 50 states for low amounts of capital is about the only compelling reason to use it.

The positive note I will relay about the cost of capital is that it has been keeping the petty fraud at bay.

There are just so many other ways to defraud grandma of her retirement than using investment crowdfunding.

I recently read Les Henderson’s “Crimes of Persuasion” and Irwin Steins “Investment Schemes, Scams & Strategies” – there is nothing new under the sun when it comes to fraud and investment crowdfunding is not how it is being perpetrated.

In my humble opinion, the regulators are focused on the wrong things. My friends at FINRA should spend more time looking at the FORM-C filings and less time shaking me down for the last three months of bank statements or asking me to defend why we think SAFEs are “suitable” investment securities.

First, a non-broker-dealer portal operator is not allowed to express any kind of preference or endorsement for any offering on its website. Secondly, you can bet a portals time dealing with compliance factors into an issuers cost of capital.

To be clear, we have seen some pretty egregious operating agreements for offerings of common stock that outright prevented investors from getting out of their investments! So focusing on the type of security sold is not protecting investors in my opinion.

The Simple Agreement for Future Equity (SAFEs) accounts for over one-third of all offerings and is basically a zero percent interest convertible note that like most convertible notes offers no voting rights nor any liquidation preferences. What will matters more in long term is access to a secondary market. More on that in a bit.

The Three Waves of Money

It’s time to dispel some myths surrounding investment crowdfunding for potential issuers and regulators. Despite the intimations and sometimes claims of online funding sources, simply “posting and praying” that random strangers are going to rain money down on you to make you stupid rich is never going to happen.

Look at the boneyard of sites like Kickstarter and even social begging on GoFundMe to get some perspective. Investment Crowdfunding is DIFFERENT because you’re selling a great INVESTMENT instead of a great PRODUCT or appealing to the heartstrings of donors. There is only room for one kid to sell a viral potato salad recipe once.

The stats from three years of runtime with REG-CF nearly mirror the success rates of rewards and donation-based crowdfunding. Low dollar amounts and lots of investors.

The last report we saw suggested that the “average” successful REG-CF deal raised about $250K from about 350 investors at about $800 per investment with an overall success rate of about 45%. Pretty dismal. It’s no wonder angel investors and venture capitalists are so down on crowdfunding with cap tables of that size and the inability to do the raises in Special Purpose Entities (or Vehicles).

The reality of fundraising, regardless if you’re selling Girl Scout Cookies or seed capital for your startup is this:

“All fundraising is the SLOW conversion of your SOCIAL capital into FINANCIAL capital.”

The First Money that comes in is almost always betting on the founders first and then on their idea second. They are investing because they like and trust the team. They may be investing out of a sense of obligation for prior reciprocal support. But ultimately it is confidence in the team that brings the first money. Incidentally, people who know you tend to live by you, which is why intrastate investment crowdfunding often makes more sense.

The Second Money that arrives is betting on the idea. These are the “friends of friends.” They may or may not know the team personally but they know someone who does and through that social credibility comes the second wave. These investors have a more critical eye on the soundness of the idea. They will be the ones that ask the most critical questions because they are in this for the Return on Investment (ROI) primarily and sometimes Fear of Missing Out.

The Third Money, if it ever shows up, is betting with the crowd. These are investors that do not know the founders, may not know anyone who does and may only have a vague understanding of the business model or how they are going to make money on the investment. They are relying on the “wisdom of the crowds” and are definitely investing for affiliation and upside.

There is nothing sadder than seeing a busker on the sidewalk with an empty guitar case. The more savvy musicians know they need to “salt that tip jar” to get others to contribute. It is a form of normative behavior at play. People look to the crowd to see how to behave. If no one has contributed the inertia to be the first is high. So it also goes with donation, reward, and investment crowdfunding! Success breeds success and success has many fathers. Failure is always an orphan.

Let’s Settle the SCOR

The Small Corporate Offering Registration or “SCOR” offering (Rule 504 of Reg D) is experiencing somewhat of a renaissance in part to some automation software we created to help with the preparation of the NASAA U-7 form. For example, MNvest laws provide for a 10-day notice to file with an auto default approval while the SCOR has no such service level agreement. That stated, the last SCOR filed in Minnesota was approved in under a week!

The SCOR in a lot of ways is the grandfather of modern investment crowdfunding having been available in over 30 states now since the early 2000’s.

In fact, prior to the passing of the MNvest law the most successful offering in the state was for, unsurprisingly, a brewery that raised over $800K by putting inserts into their six packs and going door to door selling stock to their neighbors.

Belatedly, we learned only recently that the company did not use the funds as advertised to invest in a canning line. Instead, the company paid off former debts and then closed their doors. A kind of fraud that David Carpentier from Assurely says their “Crowd Protector” insurance product is designed to protect against.

Along with the updates to Rule 147 in 147a that rationalized the inter-state advertising rules was an update to SCOR that raised the ceiling from $1M to $5M.

One of the most compelling features in addition to the $5M limit of the SCOR offering is that there is, practically speaking, no limit on how much non-accredited investors can invest (subject to “suitability”) as well as the ability to file it in multiple states!

Contrast this with intrastate exemptions in Minnesota and Wisconsin that have a $10K limit per individual per investment per year, and Colorado where its $5K per investor/investment per year or Iowa where it’s $5K per family/investment per year with no restriction on accredited investors, and it makes REG-CF seem pathetically anemic.

The SCOR option is ideal for real estate projects too. Real estate has accounted for the bulk of the money raised in Minnesota due to its $5M cap and the ability for non-accredited investors to invest as much as is “suitable” for them.

We were the first intrastate and REG-CF funding portal to connect to Eric Satz’s AltoIRA.com platform and have already witnessed MUCH larger investment funds flowing through Self Directed IRAs into income producing and capital appreciating assets like commercial real estate.

Liquidity is Everything

For investment crowdfunding to really take off it requires the development of a secondary market.

For investment crowdfunding to really take off it requires the development of a secondary market.

Investors absolutely have the right to liquidity even if that means taking a haircut on their investments.

Life happens and while that investment in your town’s brewery meant solidarity with your neighbors and a meeting place for a free beer, whether it is a job change that takes you out of state, a storm that damages the roof, the kid needing braces or you need to give your liver a break, investors need a way to get out.

Michigan initially lead the way, at least legislatively, with the 2014 passage of a “Michigan Investment Marketplace” (MIM) act.

To date, no markets have developed and it is our opinion that the Michigan Licensing And Regulatory Affairs (LARA) appears to have ZERO interest in seeing one develop.

We can confirm that Silicon Prairie Portal & Exchange has made application to LARA to register as a MIM per the rules in the statute and they have responded with a four-page, single-spaced documentation request for additional information based in part on their “Notice of Proposed Rule Making” that essentially makes the legislation still-born. In their request, they asked for evidence of compliance with SEC rules that can be satisfied with a “no action letter” from the SEC — GOOD LUCK WITH THAT! They also asked for archaic “user manuals” … when is the last time you got a user manual with any software? Did your smartphone come with one? Is there a user manual for any website you use?

Once again Minnesota will likely lead the way as we were approached by the original sponsor of the MNvest law, Senator Eric Pratt, to develop legislation to bring about a secondary market here.

We are taking our proposed “MNtrade” no-action letter that we worked with our Department of Commerce last summer and grafting the best parts of the Michigan law without the LARA nonsense.

We are cautiously optimistic that we will have something drafted and ready to be introduced this session and look forward to a robust public debate on the matter.

The End of the Nanny State

It is time to put an end to the “nanny state.”

The rules in place do not protect people from themselves. The use of wealth as a measure of a person’s financial competence is idiotic and needs to be replaced with a more sensible and frankly less offensive means of segregating people.

Not to put too fine a point on it, the government will not intervene if you:

- Take out $150K in student loans (in fact they will cheerfully help you go into debt and become a wage slave)

- Pay agents to find and purchase collectible vehicles

- Spend tens of thousands of dollars on air travel, hotels, meals and “product” to try and grow a business — one that might be a blatant pyramid scheme

- Decide I want to eat $5,000 in cake every month

- Cash my check at a payday lending outlet and go to the casino

- Take out a home equity loan for $50,000 to finance a wedding for a marriage that won’t last 50 years

But if you want to make an investment in a local brewery, community solar garden, income producing commercial building, long term care facility, or the next Google that you deem worth the risk, the government arrogantly pretends to know better than you and what you want to do with your own money.

Meanwhile, the regulators are busy hassling people like us to demand our $100 investor (a recent divorcee) to cough up 3 months worth of bank statements so that they can check a box on god knows what form.

This despite the fact that there is an entire branch of the actual government known as FinCEN whose sole job is to monitor for Anti-Money Laundering (AML) for amounts that would actually rise to the level of money laundering. Not a $100 investment from a high school friend trying to put her life back together.

All the while, the Bernie Madoffs, and countless other “boiler room” operations, that get a free pass to bilk retirees out of what little assets they have been able to build is frankly asinine. For hundreds of examples where the regulators were asleep at the wheel check out Les Hendersons “Crimes of Persuasion: How Con Artists Will Steal Your Savings and Inheritance Through Telemarketing Fraud, Investment Schemes and Consumer Scams”

Let’s get Certified

A new definition, or possible certification, is required to permit investors with the means to take calculated investment risks they deem acceptable. In Wisconsin, they have adopted rules that create a new class called a “certified investor” defined as:

A new definition, or possible certification, is required to permit investors with the means to take calculated investment risks they deem acceptable. In Wisconsin, they have adopted rules that create a new class called a “certified investor” defined as:

“someone who has an individual net worth (or joint net worth with the individual’s spouse) of at least $750,000, or had an individual income in excess of $100,000 in each of the two most recent years (joint income with spouse in excess of $150,000)”

Contrast this with the federal definition of an “accredited investor”

- Has an individual income over $200,000 a year for past two years and expects same; or

- Has a joint income with a spouse of over $300,000 a year for past two years and expect same; or

- Has a net worth of over $1,000,000 that excludes equity in a primary residence

You can see that the Wisconsin definition is MUCH more rational and inclusive.

When combined with the use of tax-advantaged Self Directed IRAs the definition would DRAMATICALLY expand the available capital pool, creating a new generation of “micro-angel investors” in the process.

We believe that this will raise the average investment per offering from the current average of $800 to well over $1,000 as people begin to tap into retirement funds that have been trading sideways for years and are likely to experience significant loss in the upcoming market correction.

We’re proposing legislation in Minnesota this session to amend the MNvest rules to adopt the same “certified investor” definition and will begin advocating for the same in the other states where we operate intrastate portals.

Regulation Crowdfunding Version 2.0

Baked into the REG-CF rules is a five-year cycle of adjusting the limits for inflation. This is just about the only thing REG-CF has going for it at the moment.

The good news is that there is ALSO purportedly a mechanism in place to revisit the overall rules periodically as well.

We’ve already seen guidance come out from industry participants who think the limit should be raised to $20M as well as some surprising supporters such as the Office of the Comptroller of the Currency (OCC) that has suggested the maximum raise allowed be increased to $5M.

Here are my recommendations having lived and breathed both intrastate and interstate crowdfunding portal operations to fix REG-CF:

- Raise the REG-CF ceiling to $5M to be in line with SCOR

- Remove the ridiculous restriction on accredited investors — issuers are going to bypass it anyway by running concurrent REG-D offerings

- Set the threshold for reviewed/audited financials at raises ABOVE $1M

- Simplify the non-accredited investor amounts per campaign per year (similar to intrastate rules such as the $10K limits in MN and WI) — the current REG-CF annual limits are nearly impossible to enforce as there is no clearinghouse for the portals to share investor data and the regulators have next to zero bandwidth to monitor them anyway.

- Adopt the Wisconsin “Certified Investor” language to allow more people to participate at levels they are comfortable with investing based on their own due diligence and risk appetite

- Allow for containerization of the crowd in Special Purpose Entities so that companies do not become radioactive to subsequent rounds of capital raises

The cost of capital using REG-CF is among the highest of all the capital raising options an entrepreneur has available. To fix it, and level the playing field, might take an act of Congress.

I hope not as I believe the SEC has the power to revise their interpretation of the intent of the JOBS ACT of 2012. Otherwise, I fully expect there will be more funding portals voluntarily withdrawing their registrations as they find it nearly impossible to run a sustainable business model servicing REG-CF deals alone.

For our part, my platform is “doubling down” on investment crowdfunding by exploring the steps to become a registered Broker-Dealer, first in Minnesota and then working with the SEC staff on a low-volume exempt Alternative Trading System (ATS) as we just don’t think there will be a lot of trades in these small offerings.

Because “Liquidity is Everything” and investors absolutely have a right to it.