The Securities and Exchange Commission (SEC) has published an update on the progress of Regulation A, commonly referenced as Reg A+.

When the JOBS Act of 2012 was signed into law, Regulation A received an update that took a securities exemption from just about zero utilization to billions of dollars in offerings. While the update clearly improved the rules, many industry participants see an opportunity to enhance the exemption further.

Today, the Commission proposed several improvements to Reg A+, perhaps most importantly is to boost the funding cap to $75 million

The staff report from Corporate Finance has compiled some interesting information and statistics. Reg A+ is currently separated by Tier 1 and Tier 2 rules. On a high level, Tier 1 issuers must adhere to state blue sky review and issuers may raise up to $20 million. Under Tier 2, issuers may raise up to $50 million but are preempted from state review and must provide a fairly detailed offering circular to be reviewed, and qualified, by the SEC staff. Tier 2 offerings must also provide more detailed information than Tier 1.

The report reviewed offering as of December 2019 so it is fairly up to date.

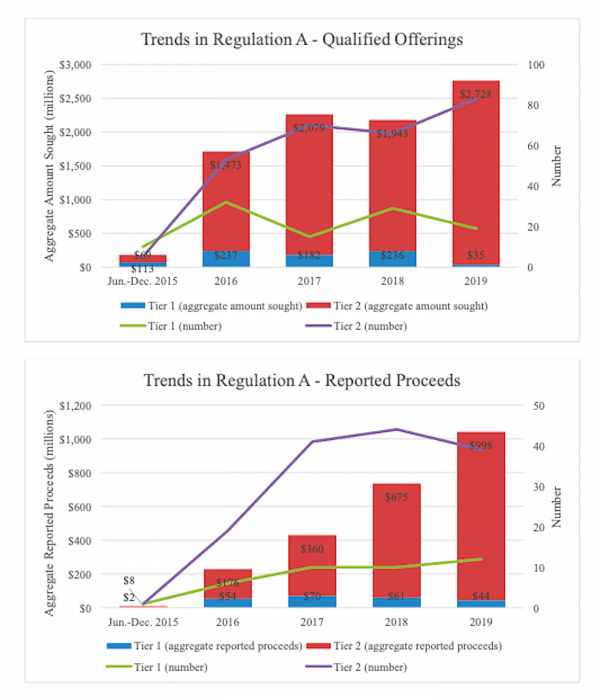

The SEC reports that Reg A+ has enabled 183 issuers to raise about $2.446 billion or an average of $13.4 million. This amount can be further segregated as Tier 1 issuers raised $230 million and Tier 2 raised the bulk at $2.216 billion.

Overall, $9.095 billion in funding has been sought across 382 qualified offerings (average of $23.8 million). This includes $759 million sought across 105 qualified Tier 1 offerings and $8.336 billion sought across 277 qualified Tier 2 offerings (excluding withdrawn offerings). About a hundred filings have not been qualified or have been withdrawn.

2019 generated the most productive year for Reg A+ as more issuers used the exemption plus the aggregate amount sought and reported raised all increased. This was due to Tier 2 issuers as the aggregate amount sought and aggregate amount raised under Tier 1 declined to its lowest level since 2015. In fact, issuers sought-just $35 million under Tier 1 in 2019. In 2018, that amount was pegged at $236 million – a dramatic decline.

2019 generated the most productive year for Reg A+ as more issuers used the exemption plus the aggregate amount sought and reported raised all increased. This was due to Tier 2 issuers as the aggregate amount sought and aggregate amount raised under Tier 1 declined to its lowest level since 2015. In fact, issuers sought-just $35 million under Tier 1 in 2019. In 2018, that amount was pegged at $236 million – a dramatic decline.

While the funding cap is higher under Tier 2, the SEC believes the fact that state review is preempted under Tier 2 helps to make the Tier more popular. It is quite difficult to endure multiple reviews by various regulators instead of just one – each with a disperse set of rules.

Most of the issuers are smaller companies, as one may expect. And while a Reg A+ issuer may soon trade an issued security, most do not. Once again this lack of liquidity may be due to overlapping state rules that impede this liquidity.

The finance sector, including real estate, accounts for 79% of all proceeds. Real estate issuers account for 69% of all reported proceeds thus it would seem the real estate sector may be the biggest beneficiary of the reconstituted rule.

The SEC addresses the frequency of enforcement actions while noting that the sample size is small and the latency of fraud can make it more difficult to tabulate. To quote the report:

“During the considered period, there have been relatively few instances of legal proceedings involving issuers or intermediaries relying on Regulation A, some of which remain ongoing as of this writing. We have identified nine enforcement actions and administrative proceedings undertaken by the Commission involving issuers or intermediaries involving or and one group of actions by a state securities regulator against an relying on Regulation A, issuer and its intermediaries.”

The SEC adds that NASDAQ has upped its listing standards for Reg A+ issuers due to a perceived lack of quality.

As well, under Reg A+ there is no requirement to utilize an intermediary and this may be “correlated with risk to investors.”

That being said, the report states it is not clear if additional protections are needed at this time.

As many regulated investment crowdfunding platforms utilize the Reg A+ exemption the report will be read with interest. Some digital asset issuers have considered Reg A+ a viable exemption but as of yet, this has not panned out.

Perhaps a more helpful discourse would be why Reg D is the most popular security exemption in contrast to all others.

The report is embedded below.