Many of you are still reeling from the impact of the worldwide collapse of the financial markets in 2008. And most of us have rightfully observed that following one of the greatest debacles in financial history, no one has gone to jail – no one has been prosecuted.

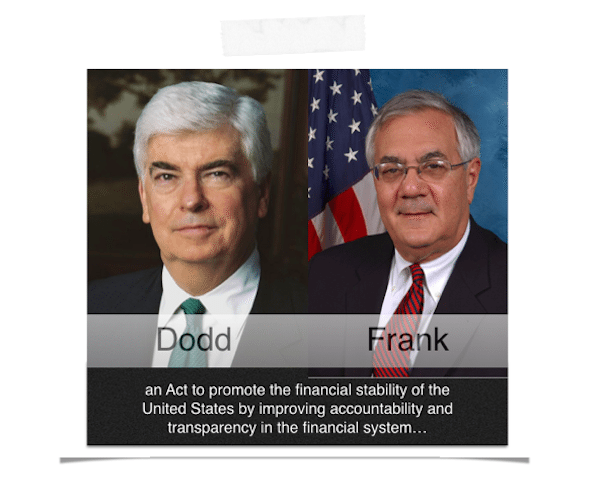

Meanwhile, rather than look back at the carnage, Congress looked forward – and put together one of the largest and most complex pieces of legislation ever in a Democrat-controlled Congress – The Dodd Frank Act of 2010 . Its purpose: to protect financial markets and the ordinary investor. And one of the gems that emerged from the Act – the Investor Advisory Committee – charged with being the watchful eye for the ordinary investor.

Meanwhile, rather than look back at the carnage, Congress looked forward – and put together one of the largest and most complex pieces of legislation ever in a Democrat-controlled Congress – The Dodd Frank Act of 2010 . Its purpose: to protect financial markets and the ordinary investor. And one of the gems that emerged from the Act – the Investor Advisory Committee – charged with being the watchful eye for the ordinary investor.

Following the mandates of Dodd-Frank, the Investor Advisory Committee met at the D.C. headquarters of the SEC on July 10, 2014, ostensibly to revisit the definition of “accredited investor” under U.S. securities laws, and with a view towards presenting its recommendations to the SEC. So in light of the recent meeting of the Investor Advisory Committee, this seemed like an opportune time to take stock of exactly how the ordinary investor fares today – four years after the passage into law of Dodd-Frank.

Let’s examine some facts.

The Great Recession of 2008 marked one of the largest implosions of household wealth in U.S. history. The large majority of Americans had their investment capital parked in either IRA’s or “managed accounts ” – in hindsight, a sucker’s bet, where Blue Chip investment managers pull in billions of dollars of investment capital, largely from ordinary investors, and rake off the top an annual fee of 1.5 – 2%, win, lose or draw. And most of this money was invested in publicly traded securities, shielded from those private placements deemed “too risky” for the ordinary investor. History recalls that the financial markets were caught by surprise, and billions of dollars vanished, almost overnight, from the accounts of ordinary Americans.

So how is Dodd-Frank solving this problem? Of recent moment, Dodd-Frank mandated that the SEC reconsider the definition of “accredited investor” by July 2014. Hence, the meeting of the Investor Advisory Committee. For individuals, up until now this has meant those persons earning more than $200,000 per year ($300,000 if married), or those with a personal net worth over $1 million, excluding principal residence. Seems that these benchmarks have stood almost unscathed since they were adopted by the SEC in 1982. The only modification to these 1982 benchmarks came in 2010, courtesy of Dodd-Frank, when Congress decided to exclude from the calculation the value of an individual’s principal residence. Seems that most in Congress were caught unaware with the realization that most Americans saw the value of their homes plummet – and in some cases – wiped out. Or perhaps, Congress was simply hedging its bet, in case one had any equity left in their home.

So how is Dodd-Frank solving this problem? Of recent moment, Dodd-Frank mandated that the SEC reconsider the definition of “accredited investor” by July 2014. Hence, the meeting of the Investor Advisory Committee. For individuals, up until now this has meant those persons earning more than $200,000 per year ($300,000 if married), or those with a personal net worth over $1 million, excluding principal residence. Seems that these benchmarks have stood almost unscathed since they were adopted by the SEC in 1982. The only modification to these 1982 benchmarks came in 2010, courtesy of Dodd-Frank, when Congress decided to exclude from the calculation the value of an individual’s principal residence. Seems that most in Congress were caught unaware with the realization that most Americans saw the value of their homes plummet – and in some cases – wiped out. Or perhaps, Congress was simply hedging its bet, in case one had any equity left in their home.

So how exactly does tightening up the definition of “accredited investor” help the ordinary investor? Well, for those legally anointed as “accredited investors,” they are legally privileged to invest in private placements, investments long labeled by consumer protection groups and state securities administrators as “too risky for the ordinary investor.” And SEC Regulation D, Rule 506, makes this group an attractive source of capital for companies: issuers can raise unlimited amounts of capital from accredited investors, without the need for SEC registration, and without the need to provide any specific type of investor disclosure. Sweet.

So how exactly does tightening up the definition of “accredited investor” help the ordinary investor? Well, for those legally anointed as “accredited investors,” they are legally privileged to invest in private placements, investments long labeled by consumer protection groups and state securities administrators as “too risky for the ordinary investor.” And SEC Regulation D, Rule 506, makes this group an attractive source of capital for companies: issuers can raise unlimited amounts of capital from accredited investors, without the need for SEC registration, and without the need to provide any specific type of investor disclosure. Sweet.

No wonder, therefore, that billions of dollars are raised every year from accredited investors under Rule 506.

On the surface, tightening up the definition of “accredited investor” may have seemed like a good idea back in 2010 – at least to the organizations/lobbyists who populated the halls of Congress while Dodd-Frank was winding its way through Congress: The Consumer Federation of America, the AFL-CIO and the North American Securities Administrators Association (NASAA). After all, who better to protect ordinary investors from risky private placements. Better to limit ordinary investors to safer investments, such as managed accounts administered by the Captains of Wall Street.

On the surface, tightening up the definition of “accredited investor” may have seemed like a good idea back in 2010 – at least to the organizations/lobbyists who populated the halls of Congress while Dodd-Frank was winding its way through Congress: The Consumer Federation of America, the AFL-CIO and the North American Securities Administrators Association (NASAA). After all, who better to protect ordinary investors from risky private placements. Better to limit ordinary investors to safer investments, such as managed accounts administered by the Captains of Wall Street.

But even those who are mathematically challenged will easily conclude that raising the bar to be an accredited investor would most assuredly shrink the available pool of capital for businesses, public and private alike. And the biggest loser of all – small businesses – a group with the least number of choices for raising capital.

So who are the winners by raising the bar for defining accredited investors?

Seems like a good deal for FINRA regulated Wall Street funds that make a living off of managed accounts for ordinary Americans. And according to NASAA, this would be a good deal for the ordinary investor and small business. It is not surprising that FINRA and NASAA would be on the same side of the issue of shrinking the available pool of accredited investors. After all, NASAA derives a good deal of its funding from broker-dealer exams administered by – you guessed it – FINRA.

Seems like a good deal for FINRA regulated Wall Street funds that make a living off of managed accounts for ordinary Americans. And according to NASAA, this would be a good deal for the ordinary investor and small business. It is not surprising that FINRA and NASAA would be on the same side of the issue of shrinking the available pool of accredited investors. After all, NASAA derives a good deal of its funding from broker-dealer exams administered by – you guessed it – FINRA.

And well, in theory at least, “ordinary investors” are the real winners – protected from risky private placements – according to NASAA, historically a haven for fraudsters.

So exactly where does this leave the ordinary investor, other than with the safety of accounts managed by seasoned Wall Street professionals or, the more risky self-managed account.

Crowdfunding you say? Not so, says the AFL-CIO, the Consumer Federation of America, and NASAA – and not so fast, says the SEC.

Frankly, all of this leaves my head spinning, as should yours.

What to do about this?

What to do about this?

Seems that at the July 10 Investment Advisory Committee meeting, Damon Silvers, an AFL-CIO representative, shared my frustration, albeit for very different reasons. At one point in the meeting he threw up his hands in frustration and stated, “perhaps we should just disband the committee and let markets decide … and the building here [the SEC] should disband.”

My suggestion to Mr. Silvers: perhaps, instead of shutting down the SEC Headquarters, a more diplomatic approach would simply be to throw up a picket line around 100 “F” Street.

Time to Take a Page from the Most Regulated Financial Market in the World

Personally, feeling both nauseous and dizzy from the debate, I am taking my cue from President Obama, and following his lead after he learned that a U.S. Ambassador was dead – and a U.S. Consulate in flames – weeks before coming up for re-election. I am taking the weekend off and heading to Las Vegas – with the hope that in my absence better minds than mine can make some sense of this. And maybe I’ll even learn something in the process. After all, Nevada gaming is the most regulated financial market in the world – where alcohol flows freely and ordinary Americans can gamble away all of their hard earned money – 24/7. And where the myriad of carefully crafted and enforced gaming regulations leave off, the laws of mathematics will ensure the ultimate outcome – for the ordinary American.

Personally, feeling both nauseous and dizzy from the debate, I am taking my cue from President Obama, and following his lead after he learned that a U.S. Ambassador was dead – and a U.S. Consulate in flames – weeks before coming up for re-election. I am taking the weekend off and heading to Las Vegas – with the hope that in my absence better minds than mine can make some sense of this. And maybe I’ll even learn something in the process. After all, Nevada gaming is the most regulated financial market in the world – where alcohol flows freely and ordinary Americans can gamble away all of their hard earned money – 24/7. And where the myriad of carefully crafted and enforced gaming regulations leave off, the laws of mathematics will ensure the ultimate outcome – for the ordinary American.

_______________________

Samuel S. Guzik, a recognized authority on the JOBS Act including Regulation D private placements, investment crowdfunding and Regulation A+, writes a regular column, The Crowdfunding Counselor, for Crowdfund Insider. A consultant on matters relating to the JOBS Act, he recently led a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy. He is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience. He is admitted to practice before the SEC and in New York and California. Guzik has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.

Samuel S. Guzik, a recognized authority on the JOBS Act including Regulation D private placements, investment crowdfunding and Regulation A+, writes a regular column, The Crowdfunding Counselor, for Crowdfund Insider. A consultant on matters relating to the JOBS Act, he recently led a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy. He is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience. He is admitted to practice before the SEC and in New York and California. Guzik has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.