When Congress passed the JOBS Act lifting the ban on general solicitation in offerings under Rule 506 of Regulation D, it turned these so-called “private” offerings into potentially very public ones. Since Reg D offerings involving general solicitation can only be sold to “accredited” investors, it also amplified the already central role that the accredited investor definition plays in determining the conditions under which issuers can sell shares to members of the public without providing the full disclosure that has been the hallmark of our securities markets. This dramatic change in policy has led some — particularly JOBS Act skeptics, but even some JOBS Act supporters — to conclude that the definition is in need of an overhaul.

In order to assess the adequacy of the existing definition, it is important to understand the regulatory purpose it is intended to serve. Regulation D relies on an exemption from the Securities Act of 1933 for transactions “not involving any public offerings.” The Supreme Court has interpreted that to mean any offering to individuals who are “able to fend for themselves” without the protections afforded by the ’33 Act. And the Court and the Securities and Exchange Commission between them have described the ability to fend for oneself as involving one or all of the following characteristics: 1) access to information about the issuer that makes the ’33 Act’s mandated disclosures unnecessary; 2) the financial sophistication to weigh the risks and merits of the offering; and 3) the ability to bear the economic risks of the offering, including risks associated with the illiquidity of private offerings and the risk of loss.

In order to assess the adequacy of the existing definition, it is important to understand the regulatory purpose it is intended to serve. Regulation D relies on an exemption from the Securities Act of 1933 for transactions “not involving any public offerings.” The Supreme Court has interpreted that to mean any offering to individuals who are “able to fend for themselves” without the protections afforded by the ’33 Act. And the Court and the Securities and Exchange Commission between them have described the ability to fend for oneself as involving one or all of the following characteristics: 1) access to information about the issuer that makes the ’33 Act’s mandated disclosures unnecessary; 2) the financial sophistication to weigh the risks and merits of the offering; and 3) the ability to bear the economic risks of the offering, including risks associated with the illiquidity of private offerings and the risk of loss.

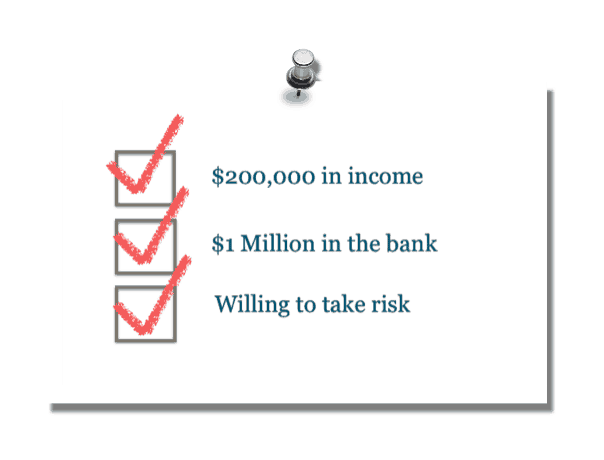

The first question then is whether the current accredited investor definition satisfies any of these three standards. In our view, it does not. The definition relies on financial thresholds — $200,000 in income ($300,000 per household) and $1 million in net worth minus the value of the primary residence — which say nothing about whether an individual is financially sophisticated or has special access to information. These financial thresholds may not even provide a sufficient cushion against risk. Individuals who qualify as accredited based on an illiquid asset, such as a family farm or closely held family business, for example, may be ill prepared to weather the liquidity risks of these offerings. Similarly, individuals who qualify based on a retirement nest egg they are depending on to provide a steady and reliable stream of income over many years may be unable to absorb potential losses without significant harm to their financial well-being.

The first question then is whether the current accredited investor definition satisfies any of these three standards. In our view, it does not. The definition relies on financial thresholds — $200,000 in income ($300,000 per household) and $1 million in net worth minus the value of the primary residence — which say nothing about whether an individual is financially sophisticated or has special access to information. These financial thresholds may not even provide a sufficient cushion against risk. Individuals who qualify as accredited based on an illiquid asset, such as a family farm or closely held family business, for example, may be ill prepared to weather the liquidity risks of these offerings. Similarly, individuals who qualify based on a retirement nest egg they are depending on to provide a steady and reliable stream of income over many years may be unable to absorb potential losses without significant harm to their financial well-being.

It is equally true that some individuals whose income and net worth fall below the financial thresholds may be able to gain access to information about an offering — by investing through an angel group that conducts extensive due diligence before investing, for example — and may have the business expertise necessary to assess the risks and potential benefits of a particular offering. If that individual keeps investments to a small portion of their overall portfolio, he or she may also be fully capable of withstanding potential losses. Yet this individual would be prevented from investing under the current definition.

It is equally true that some individuals whose income and net worth fall below the financial thresholds may be able to gain access to information about an offering — by investing through an angel group that conducts extensive due diligence before investing, for example — and may have the business expertise necessary to assess the risks and potential benefits of a particular offering. If that individual keeps investments to a small portion of their overall portfolio, he or she may also be fully capable of withstanding potential losses. Yet this individual would be prevented from investing under the current definition.

In short, the greatest strength of the current definition, that it is relatively simple to implement, is also its greatest weakness: it adopts a simplistic approach to a complex issue. There are a variety of approaches that one could take that would better meet the standard established by the Supreme Court for relying on the private offering exemption.

Many observers seem to instinctively agree, for example, that there ought to be a way for truly financially sophisticated individuals to qualify as accredited investors regardless of their income or net worth. But what is the appropriate test of financial sophistication? Is it a credential, such as the CFA designation or a series 7 license? Is it a certain record of investment or business experience? Or is it an actual test of relevant financial knowledge? Should there be a means to qualify as “sophisticated” based on reliance on a recommendation from an expert? If so, what protections are needed to ensure that the advice is unbiased and truly designed with the interests of the investor in mind?

Many observers seem to instinctively agree, for example, that there ought to be a way for truly financially sophisticated individuals to qualify as accredited investors regardless of their income or net worth. But what is the appropriate test of financial sophistication? Is it a credential, such as the CFA designation or a series 7 license? Is it a certain record of investment or business experience? Or is it an actual test of relevant financial knowledge? Should there be a means to qualify as “sophisticated” based on reliance on a recommendation from an expert? If so, what protections are needed to ensure that the advice is unbiased and truly designed with the interests of the investor in mind?

We are frankly skeptical that a good definition could ever be developed based exclusively on hard and fast financial thresholds. If the SEC chooses to continue to rely on financial thresholds, however, there are certainly changes that could be made to better ensure that these thresholds fulfill their intended regulatory function of identifying a class of individuals with the ability to fend for themselves without the protections afforded by the ’33 Act. For example, just as the value of the primary residence has been removed from the net worth calculation, other non-liquid assets could also be subtracted. This would better protect investors in Reg D offerings from the illiquidity of such investments. Certain retirement assets, such as those held in tax-advantaged retirement accounts, could also be backed out of the calculation, decreasing the harmful impact of significant investment losses.

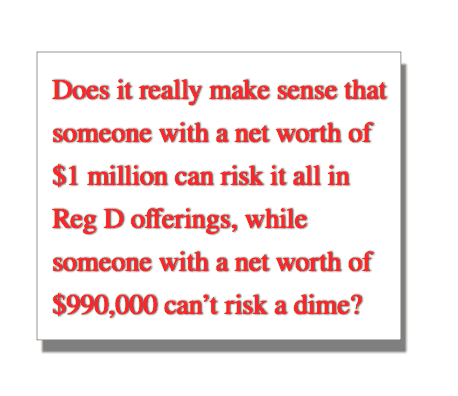

These approaches to setting financial thresholds lack the simplicity of the current definition. They also retain its all or nothing approach, another key weakness of the current definition. Does it really make sense that someone with a net worth of $1 million can risk it all in Reg D offerings, while someone with a net worth of $990,000 can’t risk a dime? If financial thresholds are going to be the basis of the definition, doesn’t it make more sense to base them on a percentage of income and net worth, as Congress did for crowdfunding and as the Commission has proposed for offerings under Regulation A? Under such an approach, a sliding scale could be adopted, with an upper limit above which an individual would be deemed to be sufficiently wealthy that no limits are necessary or appropriate. Perhaps that upper limit could be based on the current thresholds as adjusted for inflation since they were set in 1982. But difficult policy choices would remain. First and foremost, if this approach were adopted, how would we monitor for compliance with the limits in a highly dispersed market with no

These approaches to setting financial thresholds lack the simplicity of the current definition. They also retain its all or nothing approach, another key weakness of the current definition. Does it really make sense that someone with a net worth of $1 million can risk it all in Reg D offerings, while someone with a net worth of $990,000 can’t risk a dime? If financial thresholds are going to be the basis of the definition, doesn’t it make more sense to base them on a percentage of income and net worth, as Congress did for crowdfunding and as the Commission has proposed for offerings under Regulation A? Under such an approach, a sliding scale could be adopted, with an upper limit above which an individual would be deemed to be sufficiently wealthy that no limits are necessary or appropriate. Perhaps that upper limit could be based on the current thresholds as adjusted for inflation since they were set in 1982. But difficult policy choices would remain. First and foremost, if this approach were adopted, how would we monitor for compliance with the limits in a highly dispersed market with no  central party or securities professional through which all investments are conducted?

central party or securities professional through which all investments are conducted?

These are complicated questions, and there are no perfect answers. But the issue deserves more careful consideration than it has been given by those who argue simply to maintain the status quo because it works for them. Given the fundamental shortcomings in the existing definition, and the heightened importance attached to that definition in the wake of the JOBS Act, it ought to be possible to arrive at an approach that better protects vulnerable investors without unnecessarily constraining capital formation.

Barbara Roper is director of investor protection for the Consumer Federation of America. A leading spokesperson on investor protection issues, Roper is a member of the SEC Investor Advisory Committee. She chairs the IAC subcommittee that addresses issues that directly affect individual investors, including issues related to JOBS Act implementation.

Barbara Roper is director of investor protection for the Consumer Federation of America. A leading spokesperson on investor protection issues, Roper is a member of the SEC Investor Advisory Committee. She chairs the IAC subcommittee that addresses issues that directly affect individual investors, including issues related to JOBS Act implementation.